Current Access Level “I” – ID Only: CUID holders, alumni, and approved guests only

Campus open to active affiliate Columbia University ID (CUID) holders and approved guests only.

Columbia students, faculty, and staff can use the guest registration portal to register up to two same-day guests. Alumni can use the portal to register for campus same-day access as well. Learn more below.

This website uses cookies as well as similar tools and technologies to understand visitors’ experiences. By continuing to use this website, you consent to Columbia University’s usage of cookies and similar technologies, in accordance with the Columbia University Website Cookie Notice.

President Donald Trump said one reason that the U.S. will “run” Venezuela and “indefinitely” control its oil sales is because "years ago" Venezuela "took our oil away from us" and "stole our assets." That’s an oversimplification of what happened when Venezuela assumed greater control of its energy sector.

The US intervention in Venezuela may jeopardize both the flow of discounted Venezuelan oil to China's teapot refineries and the role of Chinese oil companies in Venezuela’s upstream business.

Great power competition—particularly between the United States and China—is intensifying. This rivalry is reshaping everything from technology supply chains and energy security to the future of artificial intelligence. ...

The Center on Global Energy Policy at Columbia University SIPA's Women in Energy initiative and Accenture invite you to join us for an evening of conversation and networking...

Event

• Accenture – One Manhattan West

395 9th Ave, New York

About Us

We are the premier hub and policy institution for global energy thought leadership. Energy impacts every element of our lives, and our trusted fact-based research informs the decisions that affect all of us.

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. Rare cases of sponsored projects are clearly indicated.

For a full list of financial supporters of the Center on Global Energy Policy at Columbia University SIPA, please visit our website at Our Partners. See below a list of members that are currently in CGEP’s Visionary Circle. This list is updated periodically.

Gas production in the United States will need to grow in meeting both domestic demand and additional exports of liquified natural gas (LNG) and pipeline gas. Sounds simple, but it is not. US gas producers want higher US gas prices to maximize their returns at the wellhead; US and Mexican LNG producers want lower US gas prices to maximize their netbacks, or gross profits per barrel, overseas. As US gas exports become a larger and larger share of US gas demand, these divergent needs will make for strange bedfellows and add further risk of price volatility in the global gas market.

Market-based pricing has been acceptable in the US for 30 years, since the Federal Energy Regulatory Commission’s (FERC) Order No. 636 opened domestic gas markets.[1] What’s new is that future price volatility will be driven more and more by events overseas and with it, the inevitable political backlash and issues of energy security. After years of a flexible market being the primary driver of price, the recent loss of Russian gas to Europe has created a massive supply vacuum and pushed supply security to the forefront. What constitutes an acceptable level of price risk is changing.

The Flexibility of the US System Is Both its Greatest Strength and Weakness

Rising LNG and pipeline exports are positive for US gas producers, which should be taken as a signal to increase output. But the risk of US gas production not keeping pace is real, particularly if oil and natural gas liquids (NGL) prices are weak and if permitting issues create midstream chokepoints for incremental gas supply. Lack of US gas production growth would also present a challenge among US end users of gas in all major sectors, where low prices have been a primary engine of economic growth, industrial competitiveness, and coal plant retirements.

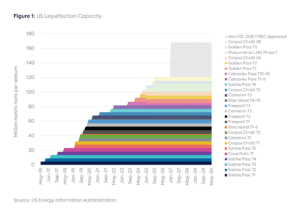

Unlike many other countries exporting LNG, the relationship between US gas production and LNG capacity growth is not integrated; a surge in new LNG export capacity – like the one that will occur between 2025 and 2030 (Figure 1) – does not guarantee a concurrent increase in US gas production to feed it. The recent focus on greater capital discipline and shareholder primacy in US shale only augments this concern.[2] If global gas prices remain high relative to US prices, US LNG exports will become a baseload form of gas demand in the US and create a greater competitive risk to US domestic buyers.[3]

Concurrently, US domestic buyers will want more certainty that any further buildout in additional US and Mexican LNG capacity – using US gas supply – will not raise domestic prices above the netback equivalent of what Europe and Asia are now paying. Conversely, the temporarily loss of access to US LNG supply also comes at a greater cost to Europe and Asia. Similar issues have arisen in Australia, Trinidad, and Egypt. In each case, domestic use was prioritized. Australia has attempted to solve this potential problem by establishing an Australian domestic gas security mechanism (ADGSM) in July 2017 as a policy to manage exports in case of a domestic shortfall.[4] Much to the chagrin of Australian gas producers[5], a price cap of $12 per gigajoule ($12.60 per million British thermal units) was placed on sales to Australian customers of uncontracted wholesale gas in December and will remain in place until the end of the year.

US LNG exports already account for 12 percent of US gas demand.[6] Add in pipeline exports to Mexico and this number grows to 20 percent.[7] By 2030, these figures could approach 30 percent without counting a slew of 80 million tonnes per year (MTPA) of announced Mexican LNG projects underpinned by US gas production.[8]

Meanwhile, US domestic gas demand will not be sitting still. Whether assuming historical average US demand growth rates of 2.3 percent[9] or lower growth rates of 0.5 percent through 2050 tied to more aggressive decarbonization and electrification goals,[10] the market will likely grow. If the commercially or policy driven retirement of the last 137 gigawatts of US coal capacity[11] emerges by 2035 or 2050, a combination of generation involving gas, renewables, and battery storage will need to replace it. Note that a higher oil and gas supply scenario by the EIA does show annualized demand losses of 0.6 percent through 2050, as does a low-cost renewable scenario leading to more aggressive decarbonization efforts.[12]

The Risks of a Non-integrated Value Chain

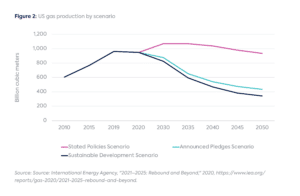

New LNG contracts do not necessarily greenlight new US gas production (Figure 2), although they do send market signals to do so. Capital discipline, midstream availability, acreage valuations, and other intangibles also influence US gas production. Most of all, gas production and prices are influenced by crude oil and NGL production to such an extent that gas is occasionally flared just to capture the rent from liquids output and is essentially treated as a waste product.[13] The increasing gas-to-oil ratio in US production is a positive for LNG producers and would de-risk gas supply, provided that the gas does not get stuck behind a pipe midstream,[14] an occurrence becoming more common as output grows.[15]

The pas de deux between US gas producers and US LNG exporters is already well-established. During 2020, a weaker international market led to the cancellation of 177 LNG cargoes[16] from the US due to negative netbacks and financial losses on exports. Russia also cut pipeline exports.[17] New global LNG supply was outpacing demand growth due to COVID-19 restrictions and forcing down the benchmark Japan Korea Marker (JKM) prices in Asia and Dutch Title Transfer Facility (TTF) prices in Europe. Despite weaker US gas prices as well, more money was still being made selling the US gas domestically than liquefying it and sending it abroad. The rise of US demand losses tied to COVID restrictions only accelerated this imbalance and triggered a major cut in US gas production from 91 billion cubic feet per day (Bcf/d) when Covid began to 82 Bcf/d at its nadir in June 2020.[18]

Today the opposite is true; the arbitrage opportunity overseas is massive, and tied to the loss of Russian gas pipeline exports to Europe, which created a gaping hole in the global supply/demand balance. In addition, the loss of 136 US cargoes tied to the temporary Freeport LNG closure in June 2022 also firmed global gas balances by pulling supply out of the market. Simultaneously, the loss of Freeport as a gas buyer in June has helped push down Henry Hub spot prices from $9 to $3, as US production has risen due to price signal coming from the gas itself as well as crude markets.

With US LNG exports surging, the question becomes whether it is wise to allow the market to operate as is or to create a mechanism to limit the influence of global gas markets on US prices. As the saying going, the cure for higher prices is higher prices, as demand weakens and the incentive to produce rises. Should policy emerge to minimize the risk in this interim period?

Foundations and Individual Donors Anonymous Anonymous the bedari collective Jay Bernstein Breakthrough Energy LLC Children’s Investment Fund Foundation (CIFF) Arjun Murti Ray Rothrock Kimberly and Scott Sheffield

[3] Study by US Gas consumers showing economic risk to export primacy. https://www.utilitydive.com/news/us-poised-to-become-leader-in-gas-exports-but-some-fear-price-impacts/448989/

[8] US pipeline exports to Mexico are also an issue. Current exports are 6 Bcf/d, while capacity to export at the border is 15 Bcf/d. Midstream constraints in Mexico keep this number from rising in the short term, although Mexico is chronically short of gas and does offer another potential market vulnerability. By global standard, inexpensive US gas, which prices only $0.50-$1/MMBtu over Henry Hub, is a major driver of Mexican industry.

[17] Alaska operated a stand-alone LNG project at Kenai from 1969 to 2017. The plant primarily serviced Japanese buyers but ran short of gas in southern Alaska. The North Slope of Alaska has sizable gas reserves and has been reinjecting gas for decades due to a lack of market or LNG facility. Multiple attempts to build a gas pipeline from the north to Kenai have failed.

From the east to west and north to south, in red states and blue states, attention to data centers is skyrocketing in state capitals across the United States.