Israel-Iran Energy War Disrupts Global LNG Supply for Years

Qatars LNG Facility Damage Forces 3-5 Year Repair, Contract Cancellations Attacks on Ras Laffan disrupt global supply, triggering force majeure on con

Current Access Level “I” – ID Only: CUID holders, alumni, and approved guests only

Get the latest as our experts share their insights on global energy policy.

On February 28, the US and Israel launched new attacks on Iran targeting primarily the country's leadership, security forces, and missile program.

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

As the conflict in the Middle East enters its 20th day, events on the ground have shifted into a critical new phase marked by direct strikes on core...

Find out more about our upcoming and past events.

This roundtable is open only to currently enrolled Columbia University students. To register, you must sign in with your UNI. The Center on Global Energy Policy (CGEP) at...

Insights from the Center on Global Energy Policy

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. Rare cases of sponsored projects are clearly indicated.

For a full list of financial supporters of the Center on Global Energy Policy at Columbia University SIPA, please visit our website at Our Partners. See below a list of members that are currently in CGEP’s Visionary Circle. This list is updated periodically.

While the EU has significantly reduced pipeline gas imports from Russia, from 132 billion cubic meters (bcm) in 2021 (BP 2022) to 62 bcm in 2022 (Energy Institute 2023), its dependence on Russian gas remains considerable. In 2022, pipeline and liquefied natural gas (LNG) from Russia amounted to 80 bcm, representing 23 percent of the EU’s energy consumption (Energy Institute 2023). The EU is proposing to phase out the remaning Russian gas supplies by accelerating the deployment of (variable) renewable energy supply. In this article, the author outlines a key challenge facing the EU during this transition period by focusing on the problem of high demand variability and related price risk—and proposes policy options to deal with this challenge.

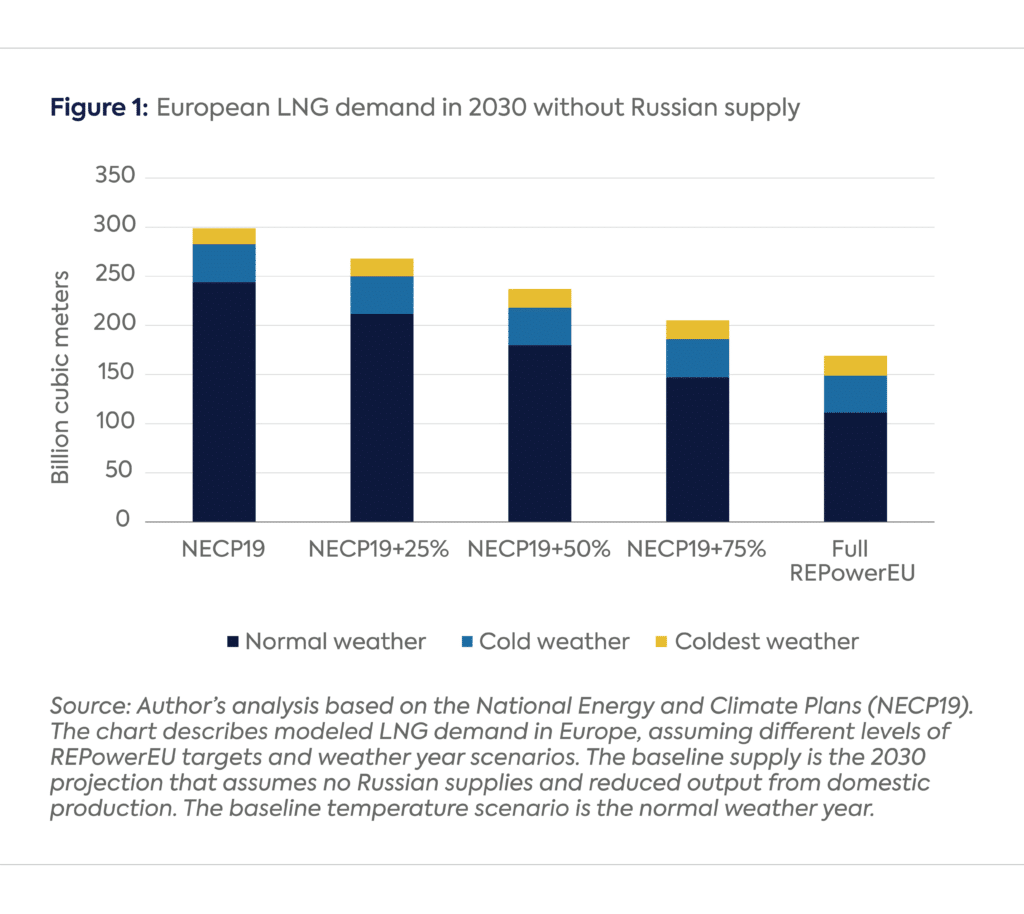

Simple modeling of European (including Ukraine and Moldova) LNG demand shows that if the EU meets the REPowerEU targets, total LNG demand is expected to reach 111 bcm in 2030. This model considers renewable policy targets, the potential reduction of domestic production, and a complete phase-out of the remaining Russian gas in Europe (Ah-Voun et al. 2023).

However, in the coldest year, LNG demand could increase to 169 bcm, or 47 percent of European demand. To put this in the context of the global LNG market, which is expected to go from 184 bcm in 2022[1] to 263 bcm in 2030,[2] Europe would consume 42 percent of all spot LNG trade in a normal weather year and as much as 64 percent, or two-thirds of the expected spot market, in the coldest weather year. The inter-annual demand variability is equivalent to almost one-quarter[3] of the entire spot LNG market in 2030 (Figure 1), potentially causing global gas price spikes. Moreover, these annual demand variations are not remote scenarios, as cold weather years occur twice in 10 years (Ah-Voun et al. 2023).

Targets less ambitious than those set by REPowerEU will likely increase prices even more. For example, reaching only 75 percent of the REPowerEU targets means that Europe would need to import at least 147 bcm of LNG (56 percent of the global spot LNG market), but in the coldest weather year the import requirement could reach 205 bcm (78 percent of the global spot LNG market).

The EU’s reliance on the spot LNG market will increase during its transition from Russian gas toward renewables, potentially increasing its exposure to price risk and impacting its energy security. In theory, recent long-term contracting activities by European buyers[4] could mitigate spot price risks, but the volume of these deals is marginal compared to the expected LNG demand. Here are three complementary policy options for European decision makers to consider to mitigate the impact of the EU’s increasing reliance on the spot LNG market.

1. Baseline demand reduction targets

Under a 2022 mandate,[5] EU member states (MS) agreed to reduce their gas demand by 15 percent compared to their average consumption in the past five years (April 1, 2017, to March 31, 2022) with their own measures. Should the European Commission and MS wish to extend this gas savings mandate, it would be helpful to consider a more comprehensive definition of the baseline demand against which to measure the savings, including:

2. Revision to the gas storage regulation

The 2022 EU gas storage regulation[7] mandates that, until December 2025, EU MS fill their storage facilities to at least 90 percent of their storage capacity by November 1 of each year.[8] But with the EU phasing out natural gas under REPowerEU, the existing storage target—equivalent to 90 bcm—is a potential overestimation of the need for natural gas in the long run. The author estimates that the coldest weather year may result in 46 bcm of extra gas demand, about half of the storage target. And in a normal weather year, total gas demand is expected to be just under two-thirds of the 2021 demand.

Overprotecting consumers with high storage levels may have been necessary during the 2022 crisis. However, an inefficient gas storage policy might impede the EU’s sustainability and energy affordability objectives. It triggers expensive gas infrastructure investments, leading to stranded assets as Europe strives to be carbon neutral by 2050. Indeed, almost half of the energy deals involving the EU and its MS since 2022 had long-term implications for infrastructure (Dennison et al. 2022).

If the storage regulation extends beyond 2025 to deal with market uncertainty posed by the inter-annual variability of gas demand, geopolitical events, and technological risks, the filling targets could be indexed to the baseline winter demand rather than total gas storage capacity. It may also be possible to develop a market-based approach with minimal distortions to the existing operations of the wholesale gas markets in Europe. For example, storage system operators could run auctions of a premium on the prevalent seasonal price spreads, encouraging suppliers and shippers to inject the gas required to meet the desired storage targets. In these auctions, bidders would specify a seasonal price spread premium for every quantity of gas they would be willing to inject at that premium.

3. LNG options contracts

Jointly (for example, by building on the joint purchasing platform[9] established in 2022) or separately, MS can also consider auctions for LNG options contracts (Losz et al. 2023), with the volume to be auctioned indexed to the baseline demand. This policy option could be an alternative or it could be supplementary to extending the storage regulation discussed above. The difference is that LNG options contracts are financial contracts with the risk of sellers defaulting on delivering LNG cargos when most needed (although non-delivery can be penalized at a cost above wholesale price). On the other hand, storage obligations require a physical injection of gas, and hence actual ownership, but at a much higher cost due to the cost of purchasing and storing the extra gas in storage facilities.

In conclusion, as Europe phases out Russian gas with more renewables, there will be greater demand variability and resulting impact on European spot gas prices. Long-term contracting, the traditional way for buyers to mitigate spot price risk, is incompatible with Europe’s climate objectives. The author has proposed some alternative policy options to mitigate this price risk.

CGEP’s Visionary Circle

Corporate Partnerships

Occidental Petroleum Corporation

Tellurian Inc

Foundations and Individual Donors

Anonymous

Anonymous

the bedari collective

Jay Bernstein

Breakthrough Energy LLC

Children’s Investment Fund Foundation (CIFF)

Arjun Murti

Ray Rothrock

Kimberly and Scott Sheffield

Ah-Voun, D., Chyong, C.K., and Li, C., Potential Implications of the Repowereu Plan on European Energy Security. SSRN Preprint. DOI: https://dx.doi.org/10.2139/ssrn.4569761

BP. (2022). Statistical Review of World Energy. https://www.bp.com/en/global/corporate/energy-economics/statistical-review-of-world-energy.html

Custer, T. (2022). 2022 Outlook: Global liquefied natural gas. Bloomberg Intelligence Industry. https://www.bloomberg.com/professional/blog/2022-outlook-global-liquefied-natural-gas/

Dennison, S., Kardaś, S., Piaskowska, G., & Zerka, P. (2022, November). EU Energy Deals Tracker. European Council on Foreign Relations. https://ecfr.eu/special/energy-deals-tracker/

Energy Institute. (2023). Statistical Review of World Energy. https://www.energyinst.org/statistical-review

GIIGNL. (2023). GIIGNL Annual Report. https://giignl.org/giignl-releases-2023-annual-report/

Losz, A., Chyong, C. K., & Joseph, I. (2023). Beyond Spot vs. Long Term: Europe’s LNG Contracting Options for an Uncertain Future.

Refinitiv. (2023). Refinitiv LNG Infrastructure Database.

[1] In 2022, spot and short-term LNG trade totaled 135 MT (GIIGNL 2023), assuming a conversion factor of 1.36 bcm/MT gives 183.6 bcm.

[2] The calculations of European LNG demand in the total spot LNG market assume that by 2030, there will be 874 bcm of total LNG export capacity (Refinitiv 2023), a utilization rate of 86% (Custer 2022) for LNG export, and a share of the spot market in overall LNG trade is 35% (GIIGNL 2023).

[3] i.e., 46 bcm of additional LNG demand in the coldest year is equivalent to 22% of the 2030 LNG spot market of 263 bcm.

[4] https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/lng/103123-qatar-energys-long-term-lng-contracts-with-european-buyers-likely-to-include-natural-gas-indexation

[5] The regulation sets an objective for MS to reduce their natural gas consumption by 15% between April 1, 2023, and March 31, 2024, compared to their average consumption in the period between April 1, 2017, and March 31, 2022.

[6] For example, considering peak electricity load days, expressed in terms of residual load to be met by gas-fired generation subject to N-1 contingency in the electricity security of supply assessment.

[7] https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32022R2301&qid=1669911511115

[8] Along with a series of intermediates targets in May, July, September, and February.

[9] https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32022R2576

Iran has among the world's largest natural gas resource bases, but its ability to supply regional and global markets is constrained by sanctions, underinvestment, and limited export infrastructure.

Iran appears to be a natural gas giant, due to its large proved gas reserves and significant gas production and consumption.

Venezuela holds 70% of Latin America's natural gas reserves, which it could export to Colombia and Trinidad to increase revenues.

Geopolitical uncertainty associated with Russian gas exports could swing the range of those exports by an estimated 150 bcm per year.

Amid global oil and gas disruptions, China stands prepared for the electrostate era.

Anne-Sophie Corbeau and leading experts explore how Europe's gas sector is being reshaped by geopolitical shocks.