The oil market ‘is lying to us’ oil execs say

Oil prices held above $100 a barrel on Thursday as peace talks between the US and Iran collapsed before a second round could take place.

Get the latest as our experts share their insights on global energy policy.

Europe is entering the 2026 gas injection season with its lowest level of gas in storage since 2018.

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

The global order that shaped the past several decades is giving way to a more fragmented and uncertain world. Long-standing alliances are under strain, economic integration is giving...

Insights from the Center on Global Energy Policy

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. Rare cases of sponsored projects are clearly indicated.

For a full list of financial supporters of the Center on Global Energy Policy at Columbia University SIPA, please visit our website at Our Partners. See below a list of members that are currently in CGEP’s Visionary Circle. This list is updated periodically.

November’s election for president of the United States will have crucial implications for the nation’s and world’s energy and climate policies. From meeting the needs of the energy transition, to managing conflicts between trade policies and climate goals, to engaging in the global competition for critical minerals, decisions the next president makes will reverberate around the world.

At the Center on Global Energy Policy, scholars are thinking about how the priorities of Kamala Harris and Donald Trump could shape policies, markets, and geopolitics. This special blog post offers brief thoughts on what might change in key energy and climate areas after the next US president takes office.

Climate change is real and worsening, and the urgency to combat climate change is increasingly evident. Efforts to accelerate the pace of transition to a low-carbon energy system are yielding remarkable results. For example, this year, global spending on clean energy is on track to reach almost double the amount going to fossil fuels. Despite this progress, oil use, natural gas use, and coal use are all still rising globally, and annual global greenhouse gas emissions will reach their highest level ever in 2024.

Acknowledging this reality, a key priority moving forward is to sharply accelerate the deployment of low-carbon energy globally.

The Inflation Reduction Act (IRA) was a historic step toward this goal, representing the world’s largest-ever investment in clean energy. Given Vice President Kamala Harris’s recent comments on energy and climate, she would likely continue to support effective implementation of the Inflation Reduction Act to accelerate clean energy deployment in the US. This includes finalizing outstanding regulatory guidance to allow companies to access federal incentives, providing the market with certainty that long-term tax incentives for clean energy deployment will remain in place, and making it easier to build energy infrastructure at scale by working with Congress to enact meaningful permitting reform, building on the current proposal by Senators John Barrasso and Joe Manchin.

The future of the IRA would seem to be at greater risk should President Donald Trump return to office next year. Trump has vowed to “rescind all unspent funds under the misnamed Inflation Reduction Act,” and in August said he would consider ending the $7,500 consumer tax credit for EV purchases. The EV tax credit, along with support for renewable energy, may be the most vulnerable parts of the IRA, given Trump’s past statements and also potential need to find revenue to pay for a tax cut extension. At the same time, Trump would likely be unable to repeal the IRA without congressional support although could tighten interpretation of Treasury Department guidance to make tax credits hard to access. Moreover, the job growth and investment resulting from the IRA in domestic manufacturing of clean energy technologies like solar and electric vehicle batteries has been overwhelmingly beneficial to Republican-leaning states, leading a group of Republican House members recently to write a letter encouraging the Speaker not to repeal the IRA.

While successful implementation of the IRA (along with regulatory actions) is necessary to get the US closer to its emission reduction target, it is important to note that the US represents less than 5% of future greenhouse gas emissions through the end of the century. Currently, emissions are growing fastest in emerging and developing economies, which comprise two-thirds of global greenhouse gas emissions.

A key priority for the next administration should thus be to build on the success of the IRA with an even more ambitious policy agenda to accelerate clean energy deployment in the rest of the world. While the odds of a Harris administration prioritizing such an effort might seem higher than a Trump White House, I have written recently about why doing so is important not only for climate change but also for advancing America’s security, geostrategic, and economic competitiveness interests—objectives both political parties should agree on. As for actions the next administration could take to achieve this goal, I recently wrote a memo for a roundtable discussion in Washington DC in response to a request to articulate specific steps a potential Harris administration could take to address the climate crisis and support the clean energy transition around the world.

US foreign policy toward the Middle East will be a challenge for either a Harris or Trump administration in early 2025.

The next American administration will have opportunities to accelerate the deployment of capital for clean energy infrastructure across emerging markets and inside the Middle East, including in partnership with the region’s sovereign investment vehicles. This will have long-term political and economic impacts in the countries receiving these financial interventions and on bilateral relations of the US and its Gulf partners. However, the financing of clean energy, whether in wind or solar plants or critical mineral supply chains, is not a source of good governance or democratic influence on its own, especially if the capital supporting it is state-owned. Gulf economic statecraft uses financial support to achieve political goals, so one can expect the strengthening of bilateral authoritarian relationships in places where these states and their investment vehicles engage. Clean energy infrastructure alone does not necessarily support political competition, transparency, or responsiveness to citizens.

In tandem, the United States will face choices about its own energy sector, including the ability of foreign state investors to engage, own, and operate new infrastructure in blue and green hydrogen as well as traditional oil and gas production and pipeline facilities and refineries inside the United States. In domestic oil production, some minor variance in support from either a Harris or Trump administration could be seen, but both are likely to commit to symbols of energy independence encouraging oil and gas production, which could have some impact on how Middle East oil and gas producers view the United States as a competitor. (It is unlikely, though, that either candidate would be able to spur production as a policy imperative given how domestic private firms choose to expand operations and return profits to shareholders.)

In Middle East and North Africa regional gas production, US attention will likely be drawn to two different but related brewing crises. In Egypt, the decline in gas production and export capacity will have increasingly painful impacts on its fiscal balance and require further US, multilateral, and Gulf support. The maritime agreement between Israel and Lebanon in October 2022 that established boundaries on oil and gas production for each country and that has benefitted Israel’s gas production (little has been found or produced offshore in Lebanon) may be threatened by Hezbollah. Conversely, the maritime agreement might be threatened by nationalist politics inside of Israel.

How OPEC+ can maintain cohesion in the face of increasing supply from the Americas will create opportunities and challenges, especially for Saudi Arabia if the kingdom seeks closer defense and nuclear cooperation with the United States. A parallel effort by Saudi Arabia to retake market share (reminiscent of 2014 and 2020) could ensue and even come with a US administration’s blessing despite the negative impact to US producers, as their higher costs of production would hurt their balance sheets. Saudi Arabia and the UAE would likely see market dominance achievable in the longer term, as some of their OPEC+ partners are sidelined by more severe fiscal stress and a lack of investment and technology access. A weakening Iran, Iraq, and Libya—Russia and Venezuela, too—could play to US national security interests as well.

Most importantly, either Harris or Trump will face the dilemma of confronting Iran. By January, the region could look very different, given an expected Israeli retaliatory attack on Iran. Further escalation cycles that do not achieve deterrence but rather draw the United States and other powers into the conflict is a worrying pattern to expect between now and January 2025. Either candidate could enter office with a direct war between Israel and Iran well underway. But even as things stand now, the oil market’s risk assessment and subsequent price sensitivity are sure to increase, as the market has been relatively sanguine since October 7, 2023.

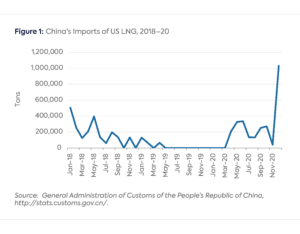

On paper, US liquefied natural gas (LNG) exports to China are set to increase dramatically during the next administration due to the large volume of supplies contracted by Chinese buyers in recent years. Since 2021, Chinese buyers have signed mostly long-term contracts to purchase 27.4 million tons per annum (MTPA) of US LNG.[1] This is more than seven times the volume of LNG the US exported to China in 2023 (3.6 MTPA), which at the time amounted to 4 percent of US LNG exports and China’s LNG imports. The announced start dates for most of these contracts are between 2025 and 2028.[2] But political uncertainties posed by the US presidential election and commercial factors could prevent all of this LNG from flowing to China.

Vice President Kamala Harris’s position on LNG exports is uncertain. In January 2024, the Biden administration, of which she is a part, paused its review of applications for licenses to export LNG to countries without free trade agreements with the United States, such as China, in order to update the economic and environmental studies that inform its decisions. Several projects affected by the pause are slated to supply Chinese buyers. While former President Donald Trump has said that, if reelected, he would lift the pause on day one, Harris has not explicitly addressed the issue. That said, comments she has made highlighting record levels of US natural gas production under President Joe Biden suggest she might also favor more LNG exports, perhaps with new licensing requirements.

As for Trump, his “more than 60 percent” proposed tariff on all Chinese imports, if implemented, could disrupt US–China LNG trade entirely, if Beijing were to respond in a way that mirrors its response to the tariffs Trump imposed on Chinese imports in 2018–19. That earlier response involved placing its own tariffs on US imports, including LNG, which caused Chinese imports of US LNG to fall to zero in May 2019, where they remained until after the two countries inked the US–China Phase 1 Trade Deal in January 2020 committing China to buying more US energy (see Figure 1).

Beyond the election, the growing role of Chinese companies as global LNG traders means that Chinese buyers of US LNG might not ship that LNG to China. Chinese LNG importers value US LNG because of its lack of destination restrictions, which allows them to send cargoes to wherever they command the highest price. Indeed, after Russia’s invasion of Ukraine, Chinese firms profited from reselling US LNG to Europe. Moreover, some US LNG supplies contracted by Chinese buyers are with projects that have not made final investment decisions.[3] Consequently, there is a risk that some of these projects might not move forward in light of projections that the global LNG market will shift to oversupply before the end of the decade.

[1] S&P Global Commodity Insights.

[2] Ibid.

[3] Ibid.

In the last two decades, energy and climate have been a foundation of the growing US-India relationship, on par with defense and security. Traditionally, cooperation has centered on meeting India’s growing energy needs through technical and development assistance and commercial ties in the energy sector. However, both countries have recently focused on sharper strategic terms, such as clean energy manufacturing and emerging technologies, in addition to India’s traditional development needs.[i] The US election will impact cooperation in two areas: clean industrial policy and fossil fuels. As seen in multiple US administrations, energy relations with India will be “all-of-the above,” but new ambition and attention at the highest political levels will depend on whether Kamala Harris or Donald Trump is in the White House.

Under a Harris administration, both countries will likely continue to grow cooperation in clean energy manufacturing and supply chain diversification. China’s dominance in clean energy manufacturing is a geopolitical and geo-economic concern for the United States and India. A recent joint statement committing to expand manufacturing in cooling, solar, electric vehicle, and wind technologies provides a starting point for a new Harris administration. Several other sectors saw enhanced US-India partnerships during the Biden administration: critical technology, semiconductors, and critical minerals. Each country’s respective industrial policies in these sectors provides domestic impetus to collaborate as well, but it is uncertain how domestic competitiveness will square with international cooperation.

Under a Trump administration, the bilateral relationship will likely ignore climate change and focus on fossil fuels. Fossil fuel trade between the United States and India reached an annual $15 billion in 2023, rising on average 13% annually between 2013 and 2023, including large increases during the Trump administration (2017–2021). This trade is largely market-driven, with increases in both supply from the United States and demand from India. Nonetheless, the prior Trump administration signed a number of agreements to increase exports of US oil and gas to India. Moreover, the threat of US sanctions on Iranian oil in 2019 prompted India to look for alternative imports. Beyond fossil fuels, it is uncertain whether the Trump administration will continue cooperation in clean energy industrial policy. While Trump has remained skeptical of technologies such as electric vehicles, the shared strategic threat from China may make some continued cooperation at lower levels of government possible.

Energy will remain a pillar of US-India cooperation regardless of who wins the White House in November. There are myriad technical assistance and development projects at the bureaucratic level that have weathered changes through US elections before. However, changes between Democratic and Republican administrations over the last two decades have impacted the high-level tone and tenor of discussions that spur consistent government-to-government cooperation.[ii] And exactly how both countries address the dominance of China in the energy transition will remain an open question next year.

[i] https://www.whitehouse.gov/briefing-room/statements-releases/2024/09/21/fact-sheet-2024-quad-leaders-summit/; https://www.whitehouse.gov/briefing-room/statements-releases/2024/09/21/joint-fact-sheet-the-united-states-and-india-continue-to-expand-comprehensive-and-global-strategic-partnership/.

[ii] https://orfamerica.org/newresearch/polls-to-policy-energy-and-climate-cooperation-united-states-and-india-2024-elections; https://orfamerica.org/newresearch/us-india-energy-climate-cooperation.

The approaches of the two US presidential candidates on international climate finance are polar opposites. Kamala Harris, if elected, is widely expected to continue the Biden administration’s efforts to increase funding for climate change mitigation and adaptation. Donald Trump, based on his prior record in office, would likely roll back many of these funding programs.

Boosting international climate finance is important because of the large investment gap that currently exists: although investments in clean energy systems are expected to rise to $2 trillion in 2024, this is a far cry from the $5 trillion in annual investments needed to stay on a path to net-zero emissions. In percentage terms, the investment gap is even greater in emerging and developing economies.

To meet this challenge, President Joe Biden launched the first US International Climate Finance Plan in 2021. As part of the plan, US international public climate finance increased by almost three times, to $5.8 billion in 2022, rose further to $9.5 billion in 2023, and is expected to reach $11 billion in 2024. The US funding for adaptation to climate change increased to $2.3 billion in 2022 from very low levels previously, and is expected to be scaled up to $3 billion in 2024.

The current administration also pledged $3 billion to the United Nations’ Green Climate Fund (GCF) during the UN’s climate change conference, COP28, last year, while multilateral development banks added $10 billion in 2022, to take the total contribution toward climate finance to $60 billion. Climate investments by the US International Development Finance Corporation (DFC) also surged under Biden. In the first two years of his presidency, total commitments by the DFC reached almost $14 billion, versus $12 billion during Trump’s entire four-year term. Though these amounts are far from sufficient, at the very least Harris’s engagement with these international efforts would likely continue.

The playbook for a Trump presidency likely points in a different direction. Less than six months into his first term, in 2017, Trump announced a withdrawal of the United States from the Paris Climate Accord, accompanied by a rollback of climate policies such as the Clean Power Plan. If he were to win in November, there could be a repeat exit from the Paris Agreement, which has significant implications for climate finance. Since the agreement is not legally binding and is based on trust and leadership, the stance taken by the largest economy sets the tone for the rest of the world. Similarly, the efforts by DFC would likely be scaled back and contributions to GCF may potentially be retracted in a repeat showing, as Trump had held back part of the pledged amount by President Barack Obama.

To be clear, even in a Trump presidency, investments in clean energy are likely to continue rising because of market dynamics, especially with renewable energy sources becoming more cost-effective on the back of technological advances. Nevertheless, a US withdrawal from the Paris Agreement and the regulatory and policy uncertainty under Trump would likely slow the pace of investments―negating some of the benefits of a lower cost of capital on the back of falling interest rates―an outcome that the warming planet can ill afford.

Energy and climate policy, particularly around fracking for oil and gas, has been an important theme in the presidential campaign. Overall, while there are important policy differences between the two candidates that will shape the US oil and gas sector, production growth will continue to be primarily driven by market factors, regardless of who wins the election.

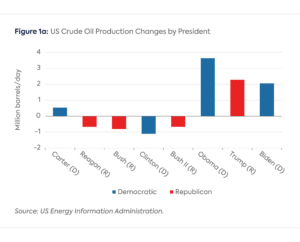

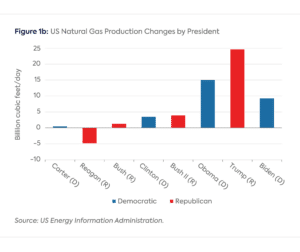

History has shown that technological breakthroughs in oil and gas production shape markets and policy more than the other way around. Over the past 50 years, the largest increase in US crude oil production occurred during a Democratic administration and the largest natural gas production increase occurred during a Republican administration (see Figures 1a and b).

Crude oil production thrived under President Barack Obama for two reasons: fracturing shale moved from a gas to an oil play, and the Obama administration eventually allowed crude oil exports to resume after a 40-year ban.

With exports of gas and liquefied natural gas (LNG) expected to account for more than 20% of US gas demand by the end of the next presidential term, the US is emerging as a swing supplier to the world. Whereas a Trump administration would likely place LNG at the center of its international energy and climate policy, a Harris administration would likely emphasize zero-emissions technologies and decarbonization pathways absent major supply shocks for oil and gas.

In terms of environmental policy, stricter fugitive methane emissions control on US upstream and midstream operations will have at least some bipartisan support—particularly if it helps strengthen EU gas commitment to US suppliers.

Beyond methane, there are stark differences between Democrats and Republicans, not least around the Environmental Protection Agency (EPA). A Trump administration would likely curtail the EPA’s regulatory authority over power plant emissions. A Harris administration would likely extend President Joe Biden’s efforts to use the EPA to impose net-zero emissions standards on new gas-fired power plants and explore similar standards for existing gas-fired power plants.[i]

Considering Vice President Kamala Harris’s disavowal of her past opposition to fracking, neither administration would be likely to seek stricter regulation of the practice. The future of oil and gas leasing on federally owned lands and waters remains in limbo following Biden’s pause on new leases that was subsequently overturned by the courts in August 2022. While politically symbolic, production on federally leased lands was only about 11–12 percent of total US oil and gas production in 2023 and unlikely to be determinative of US energy output under either administration.

Finally, the election outcome will affect the demand side of oil and gas, particularly in the medium to long term. Harris would likely double down on the Biden administration’s sector-level decarbonization goals, including through additional support for electric vehicle manufacturing and consumer subsidies as well as investment in supply chain and charging infrastructure, which could lower gasoline demand. Less clear is what Harris intends for a proposed phaseout of internal combustion engine vehicle new sales, a policy favored by the Biden administration but unpopular in battleground states, particularly Michigan.

By contrast, former President Donald Trump would likely limit federal support for and new investment in these areas, while eliminating mandates and strengthening Buy America provisions in existing programs. The fight over EPA regulation of electric power plants will also shape demand for natural gas in power generation.

[i] Democratic Party Platform 2024, https://democrats.org/wp-content/uploads/2024/08/FINAL-MASTER-PLATFORM.pdf, p. 34.

The multitude of critical geopolitical hotspots around the world might suggest Latin America is unlikely to be of high priority for either a Kamala Harris or Donald Trump administration—except around border security and immigration. However, the outcome of the US election will matter greatly for the region and for the energy and climate relationship between the US and Latin America, particularly related to the United States-Mexico-Canada Agreement (USMCA) up for review in 2026, China’s ties in Latin America around critical minerals and energy transition investments, and the potential for more sanctions on Venezuelan oil.

The US electoral results will be critical for Mexico, given potential actions that could be taken in response to the upcoming review of the USMCA. Rising Chinese investments and exports into Mexico are believed to be a loophole into the US market for Chinese companies. This has caught the attention of US policymakers, and actions to remediate this back door into the US market are likely to intensify under either a Harris or Trump administration. However, trade tensions could be significantly higher under a Trump administration given Trump’s recent call for a 100% tariff on cars manufactured in Mexico.

A productive US-Mexico relationship could be possible between a Harris administration and Mexico’s President Claudia Sheinbaum, the country’s first female president, sworn into office on October 1. However, recent reforms enacted by the former president Andrés Manuel López Obrador and additional legal changes currently making their way through the Mexican Congress will still be a challenge for the bilateral relationship, as they can potentially be seen as violating provisions in the USMCA.

How US-China trade tensions evolve under the next administration could also make it more difficult for countries in Latin America to maintain strong political and economic ties with both of these nations simultaneously. Chile, a top producer of critical minerals like copper and lithium, has received major lithium-related investments from Chinese companies in recent years, while also being courted by the US government seeking to enhance commercial ties around critical minerals under the Chile-US free trade agreement. The US has also increased efforts toward bilateral agreements on the energy transition, climate investments, and critical minerals with other countries in the region, including Argentina and Brazil. While a Harris administration would likely strengthen such agreements, it is not clear whether a Trump administration would follow through with these efforts.

Finally, the oil and gas sector may not be impacted by who gets elected to the White House. Latin America has become a key market for US fuels and natural gas exports: Mexico alone absorbs 30% of US natural gas exports and almost 60% of US gasoline exports.

Latin American countries are also likely to remain a large exporter of oil into the US (they currently represent about 23% of total US oil imports). An exception to this is oil exported from Venezuela, with the possibility of further oil sanctions against the country after the fraudulent election of Nicolás Maduro on July 28. This risk of sanctions exists regardless of who wins the US election in November.

US-European relations have never been simple, but they have nonetheless been close—including in energy and climate issues. Now, as the European Union enters President Ursula von der Leyen’s second term, and as Americans prepare to elect either Kamala Harris or Donald Trump as their next president, hard choices and perhaps serious tensions may lie ahead.

Energy and climate issues have been an important area of cooperation, debate, and sometimes diverging views between the trans-Atlantic partners. Decision makers in Brussels and EU member states have long prided themselves for providing leadership on climate change while criticizing what they felt was insufficient action by their American partners. On the American side, however, many criticized Europe’s longstanding reliance on Russian natural gas and oil. When energy supply chains were severely disrupted after Russia’s full-scale invasion of Ukraine, US-origin liquefied natural gas (LNG) was critical, and proponents for more US LNG exports say they are vital for Europe’s energy security.

Harris and Trump represent very different views of the world and very different approaches to energy and climate issues. The former president engages other countries in transactional terms, saying that doing otherwise is naïve and ineffective. In his campaign, he has proposed tariffs of 10–20% on all imports, including those from Europe, and a 60% tariff on imports from China. He disdains net-zero commitments such as the EU has adopted. And instead of continuing decarbonization efforts, he intends to abandon the Paris climate agreement again, encourage oil and gas production, and end President Joe Biden’s pause on LNG. Methane emissions would be a particularly sensitive topic, given that the EU has passed a methane regulation that will impact imports of fossil energy, notably LNG. Trump might also withdraw from the Global Methane Pledge, leading to limited progress in US methane emissions reduction—with potential negative consequences for future US LNG exports to the EU. Finally, some Republican members of Congress have criticized the Paris-based International Energy Agency for devoting too much attention to climate and have called for Trump to reconsider US participation.

In contrast, Vice President Harris appears set to follow Biden’s energy and climate policies, though she downplays these issues in her campaign. She appears likely to restart LNG export approvals, perhaps with certain restrictions, but unlike Trump she seems likely simultaneously to prioritize methane emissions reduction. Importantly for Europe, Harris supports implementation of the subsidies in the Inflation Reduction Act, which some European leaders say create unfair competition. She does not promise sweeping new import tariffs, but neither does she call for the loosening of existing clean energy tariffs, such as on Chinese solar panels. Harris may seek to extend Biden’s attempted de-linking from China in cleantech, including critical minerals, which Trump also favors. Whether Harris could secure deeper US-EU collaboration in this area through less bombast toward Europe and more nuance on China remains to be seen.

European nations would likely have varied views on these possible new American energy and climate priorities. Nationalistic leaders and/or opposition figures in Austria, Czechia, Hungary, Italy, Poland, and Slovakia may welcome the return of the former president as an EU critic. A somewhat different group might even hope for Trump to deliver peace in Ukraine in hopes of securing gas again from Russia. Current leaders in other EU states—France, Germany, the Nordics, and Spain, among others—might see Harris as a better partner on energy and climate, even if they do not embrace her views on the interplay of energy and climate.

While the US presidential candidates’ differing views on climate policy have been well covered, the election in November may also be a turning point for the federal strategy to support communities that depend on fossil fuel industries for high paying jobs and the funding of public services. The US coal industry is in decline, and all major countries have committed to transition away from fossil fuels, which presents acute risks to heavily fossil-fuel-reliant communities. An equitable energy transition requires mitigating these risks alongside the severe risks of climate change.

The federal government provides support to fossil fuel communities with a two-pillared strategy. First, recent federal laws include hundreds of millions of dollars in targeted funding, such as the Coal Communities Commitment of the Economic Development Administration and bonuses and carveouts for fossil fuel communities in the tax credits within the Inflation Reduction Act. Fossil fuel communities can also access other large pots of funding for priorities like infrastructure upgrades.

Small communities often struggle to access and effectively implement federally funded projects, so the second pillar of support involves efforts to work collaboratively with fossil fuel communities to overcome those barriers. The Interagency Working Group on Coal and Power Plant Communities and Economic Revitalization (IWG) was created in 2021 as a partnership between 12 federal agencies and coordinates government efforts to support the goals of coal-reliant communities. In six regions facing coal facility closures, “rapid response teams” are collaborating with local stakeholders to address the needs of the communities and help them access federal resources.

The effectiveness of federal actions to support fossil fuel communities remains to be seen. But given the centrality of the Biden administration to these efforts, it is important to consider how the strategy may evolve under administrations of either former President Donald Trump or Vice President Kamala Harris.

Most existing federal funding will likely remain available. Trump is calling for rescinding unspent funds from the Inflation Reduction Act, which includes measures that support fossil fuel communities and also measures that will accelerate the decline of fossil fuels. But efforts to rescind IRA funding may fail due to a lack of support among congressional Republicans whose districts are benefiting from the law.

On-the-ground efforts coordinated by the IWG may be in more jeopardy under a Trump administration, similar to how Trump did not continue President Barack Obama’s POWER+ Plan to support coal communities. When president, Trump also proposed eliminating the Appalachian Regional Commission and EPA’s Office of Sustainable Communities, a precursor to the IWG. Congress saved those programs through the budgeting process, but the IWG is not directly funded by Congress.

In contrast, an incoming Harris administration is likely to pursue a similar strategy as the Biden administration. The existing funding sources would be safe, and federal agencies would continue to help fossil fuel communities access funding and implement transition plans.

More uncertain is whether a Harris administration would prioritize additional efforts to support fossil fuel communities. Existing support has important limitations, including a focus on the transition away from coal rather than oil, natural gas, or carbon-intensive industries. Democratic senators are seeking broader support for workforce transition and economic development in fossil fuel communities, and they may need the support of the White House for these proposals. Harris’s policy plans mention support for rural communities, but not the unique risks facing fossil fuel communities as the country transitions to clean energy sources.

CGEP’s Visionary Circle

Corporate Partnerships

Occidental Petroleum Corporation

Tellurian Inc

Foundations and Individual Donors

Anonymous

Anonymous

the bedari collective

Jay Bernstein

Breakthrough Energy LLC

Children’s Investment Fund Foundation (CIFF)

Arjun Murti

Ray Rothrock

Kimberly and Scott Sheffield

On March 20, Governor Kathy Hochul proposed significant changes to New York’s Climate Leadership and Community Protection Act (CLCPA), the landmark climate law passed in 2019.

In January 2026, the UK government publicly released an intelligence report analyzing the security implications of global environmental destruction.

Securing critical minerals is a top priority of governments around the world.

The United States is at a rare inflection point for nuclear energy, with unprecedented momentum behind deployment and regulatory reform as nuclear becomes central to energy security, AI competitiveness, and state and corporate climate goals.

In March 2012, Israeli Prime Minister Benjamin Netanyahu arrived in Washington to press a US president on slowing Iran’s nuclear ambitions. Inside the White House, the dilemma was stark.

Within days of the initial U.S. and Israeli attack on Iran on February 28, 2026, the world was plunged into an energy crisis.

Energy has reemerged this year as a central force shaping our world—both a geopolitical weapon and an economic fault line.