This website uses cookies as well as similar tools and technologies to understand visitors’ experiences. By continuing to use this website, you consent to Columbia University’s usage of cookies and similar technologies, in accordance with the Columbia University Website Cookie Notice.

David Turk, who serves as a distinguished visiting fellow at the Center on Global Energy Policy at Columbia University SIPA, will testify at a full committee hearing of...

Announcement• April 8, 2025

Energy Explained

Get the latest as our experts share their insights on global energy policy.

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

In energy policy circles, the word “resilience” often refers to future-proof systems or infrastructure designed for the transition away from fossil fuels. But resilience means something different to...

Please join the Women in Energy initiative at the Center on Global Energy Policy at Columbia SIPA for a student roundtable lunch and discussion with Kadri Simson, who most recently...

Event

• Center on Global Energy Policy

1255 Amsterdam Ave

New York, NY 10027

About Us

We are the premier hub and policy institution for global energy thought leadership. Energy impacts every element of our lives, and our trusted fact-based research informs the decisions that affect all of us.

What seems a simple commercial commitment, however, involves a web of complexities. Many EU utilities are not keen to buy (US) LNG on a long-term basis on the back of expected declining EU LNG demand in the long term. Also, European companies with US LNG contracts can redirect volumes outside Europe, especially international companies looking for profits. Finally, if the EU were to double its US LNG imports in line with the US doubling its LNG exports by 2030, that would dramatically increase the region’s dependency on one supplier, which the EU is not likely eager to do.

EU Imports of US LNG in 2025

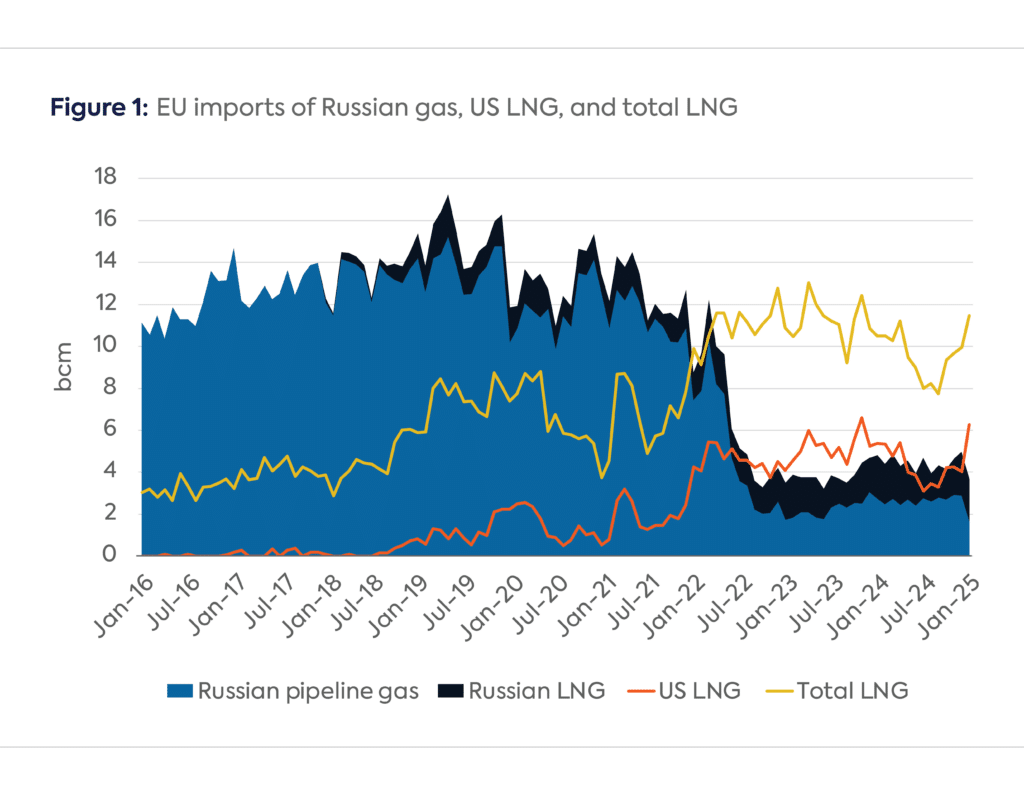

In 2024, EU imports of US LNG dropped to 51 billion cubic meters (bcm), from 62 bcm in 2023. Lower EU LNG imports was due to a mix of high storage levels in 2024, strong pipeline imports and flat EU gas demand, as well as a diversion of US LNG to more lucrative Asian LNG markets. Still, the two regions are deeply interconnected: the US supplied 45 percent of EU LNG imports in 2024 (114 bcm), while the EU purchased 43 percent of US LNG exports (119 bcm).

Higher EU imports of US LNG are likely to materialize in 2025 for two market-driven reasons, which have nothing to do with policies or politics:

US LNG exports are bound to increase, as two new liquefaction plants start in 2025 (Plaquemines and Corpus Christi Stage 3). The EIA expects US LNG exports to increase by 17 percent in 2025.

The EU will need to import more LNG to compensate for the halt on January 1, 2025, of Russian gas transit through Ukraine (which was around 15 bcm in 2024), and to refill EU storage facilities, whose levels were 20 bcm lower year-on-year as of mid-February 2025.

However, flexible US LNG will effectively land in EU countries only if EU spot prices are high enough to divert it from Asian markets, which has been the case in early 2025 so far (Figure 1) due to very high European gas prices. Retaliatory Chinese tariffs on US LNG could also lead Chinese companies to redirect contracted cargoes to Europe.

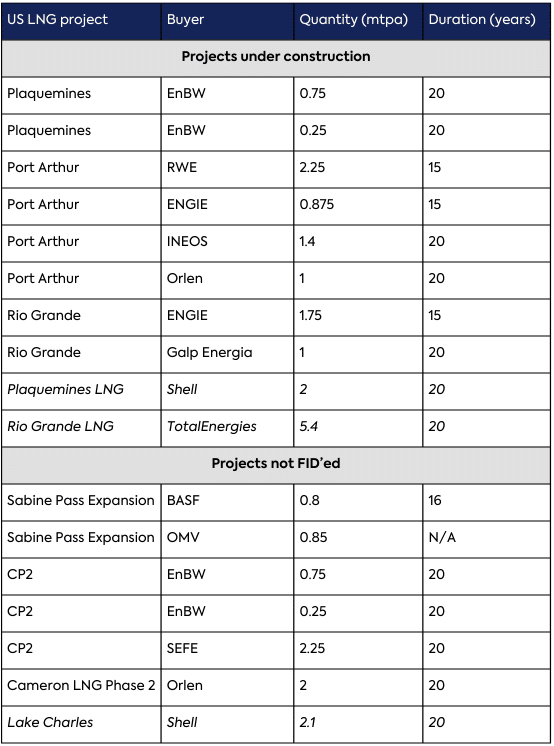

In January 2025, President Trump reversed one of the most debated decisions of the Biden administration: the pause on approvals of new US LNG exports to non-free-trade-agreement countries. Liquefaction plants are large, capital-intensive projects and need long-term contracts to secure financing and take final investment decision (FID).

A relatively low number of EU buyers signed long-term contracts with US LNG exporters after Russia invaded Ukraine in 2022, even though EU countries faced a 115 bcm/y drop in Russian pipeline gas between 2021 and 2023. Around 23 bcm/y of contracts were signed with US LNG projects now under construction: 55 percent with European utilities and the rest with European-based international oil companies (IOCs). Another 12 bcm/y were signed with projects still expecting to take FID, such as Calcasieu Pass 2, Sabine Pass Expansion, Lake Charles, and Cameron Phase 2. (See Table 1.)

Table 1: US LNG contracts with European companies, 2022–2023

Note: IOCs are in italics. Source: Companies’ announcements and GIIGNL.

Trump could potentially fulfil the role of “LNG Marketer in Chief” to nudge EU companies to sign more US LNG contracts. But in doing so, will he transact with EU governments—which are rarely shareholders of gas companies (with a few exceptions such as Engie and Uniper)—or with EU companies directly?

Finally, it is questionable whether European-based IOCs would qualify as “European,” as far as any negotiations around the trade deficit are concerned, given the global nature of their LNG business, but Trump may see them as European.

Implications for the Trade Deficit

A key reason for Trump’s ire against Europeans and desire to sell them more LNG is the US-EU trade deficit ($236 billion in 2024).

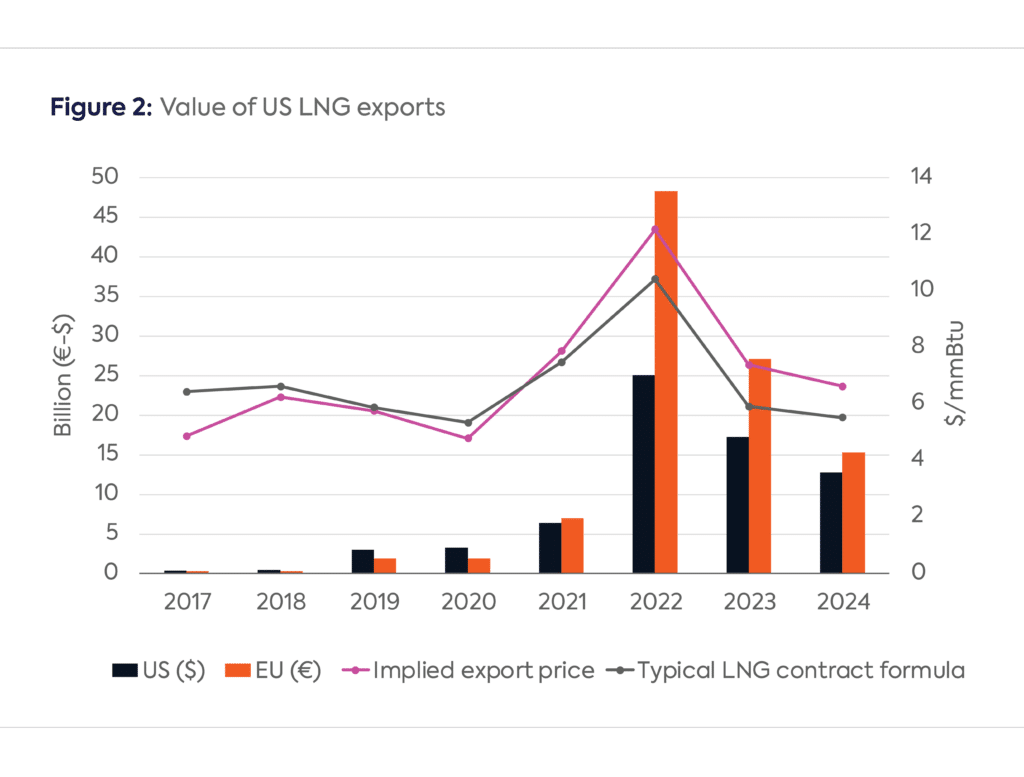

In 2024, US LNG exports to the EU were around $13 billion, according to the US Census Bureau (Figure 2), around 5.4 percent of the trade deficit. Trade data on US LNG exports observed by the US administration is influenced by both volume and price. US LNG exports price data is not straightforward: it could be the contract price (Henry Hub times a multiplier plus a liquefaction fee), or another price if the LNG is sold within a US company’s portfolio. Still, the implied annual LNG price is reasonably close to a reference contract price (115% Henry Hub + $3/mmBtu), despite a gap emerging over the past two years implying a higher sales price.

Additionally, US and EU bilateral trade data are massively different, even accounting for currency differences. Indeed, the EU import price of US LNG is different from the US LNG export price—it can be a European spot price or the contract price plus the prevailing transport fee. Given the current high European spot prices, EU trade data are much higher than what the US reports (Figure 2). EU numbers equate to almost 8 percent of the deficit, and EU policy makers could use these trade data in the upcoming negotiation.

Whatever Trump may think he is gaining in the short-term by pushing more US LNG exports to EU countries, it will hardly be a sustainable solution to bridging the US-EU trade deficit.

First, European LNG imports, including from the US, are likely to eventually dwindle as European gas demand decreases. While US LNG exports are bound to at least double by 2030, an increasing share of that is likely to go to the growing Asian market.

Second, EU countries value LNG because of the diversity in suppliers. Increasing imports and moving to an 80–90 percent share of US LNG in total LNG imports would undermine this benefit of diversification from a security of supply perspective.

Third, even if US LNG is contracted by a European company, it could end up elsewhere and not be counted in US-EU trade data. The beauty of US LNG is its destination flexibility. Offtakers can arbitrage between destinations depending on prices. European utilities are likely to deliver contracted LNG to their home market, but a European company like SEFE, with ambitions to build an international portfolio, could eventually send its contracted LNG to Asia. Meanwhile, aggregators such as Shell and TotalEnergies are beholden to their shareholders, not to ensuring Europe’s security of supply.

Finally, US-EU LNG trade also depends on the domestic US gas price. Trump’s pledge to decrease domestic energy (including gas) prices could be counter-productive to his desire to bridge the deficit. Meanwhile, higher domestic gas prices could help to reduce the deficit but hamper US gas consumers.

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

Earlier this month, China convened its “two sessions”—the annual concurrent meetings of the National People’s Congress (NPC), China’s legislature, and the Chinese People’s Political Consultative Congress, a political...

A former deputy treasury secretary and a presidential economic adviser on the need to draw a sharper line between open economies and the rest | By Invitation