Big banks predict catastrophic warming, with profit potential

Morgan Stanley, JPMorgan and an international banking group have quietly concluded that climate change will likely exceed the Paris Agreement's 2 degree

Current Access Level “I” – ID Only: CUID holders, alumni, and approved guests only

Get the latest as our experts share their insights on global energy policy.

Earlier this month, China convened its “two sessions”—the annual concurrent meetings of the National People’s Congress (NPC), China’s legislature, and the Chinese People’s Political Consultative Congress, a political...

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

Across America, energy policy is often driven by short-term politics over long-term planning. Despite record-breaking U.S. oil production in recent years, partisan battles continue over fossil fuels and...

Find out more about our upcoming and past events.

The Columbia Global Energy Summit 2024 is an annual event dedicated to thought-provoking discussions around the critical energy and climate challenges facing the global community.

Insights from the Center on Global Energy Policy

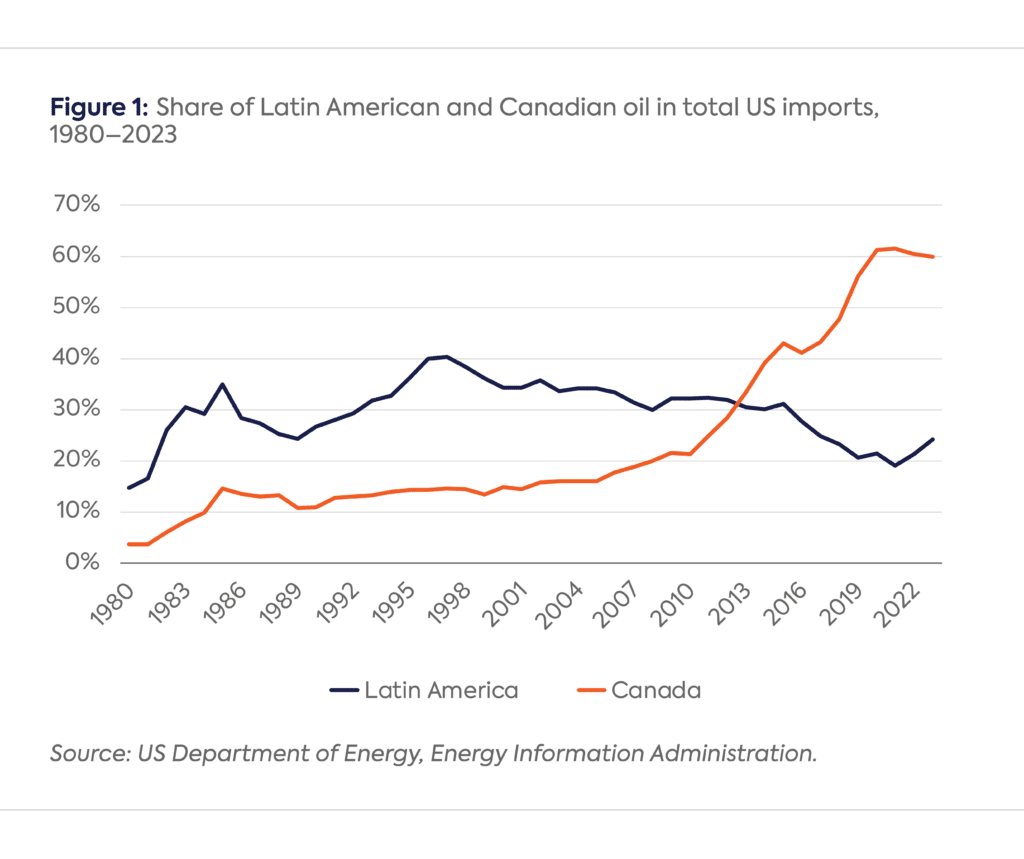

Many Latin American countries have had a long and close energy trade relationship with the United States. However, some of the Trump administration’s executive orders (EOs) have the potential to negatively impact this decades-long energy integration in the Americas. The most consequential EOs for Latin America’s energy policy and energy trade are likely the 25% tariff on US imports from Mexico and the 10% tariff on Canada’s energy imports to the US, both paused until March 4. The lower 10% tariff on US energy imports from Canada is a recognition of that country’s strategic role in the US energy market, while the 25% tariff on Mexican oil reflects how asymmetrical energy trade has become with Mexico. In fact, the US is now a net exporter of energy to Mexico and to Latin America overall, despite the region being, in theory, energy abundant.

This piece answers four of the most pressing questions about the potential effects of Trump’s EOs on Latin America’s energy trade. It looks at the tariff differentiation between Mexican and Canadian US energy imports and its implications for Mexico and the rest of Latin America within the context of the US also becoming a large oil and gas exporter to Latin America. It also explores how Trump’s EO about energy dominance amid increasing demand for electricity, and its implications, could inform Latin American energy policy.

The Trump administration’s lower tariff on Canada’s energy imports is a recognition of the strategic role of Canada’s energy sector and its integration into the US economy. While the oil trade is at the core of this strategic relationship, Canada’s energy exports encompass a broad spectrum of energy sources, including natural gas, electricity, petroleum products, and uranium as well as adjacent sectors like critical minerals. This makes it difficult for the US to impose tariffs on Canadian energy exports without negatively impacting US consumers and businesses. It also showcases that Canada is an energy powerhouse not only a net oil exporter, although oil plays the largest strategic and economic role today.

Canada’s oil and gas exports to the US totaled about $170 billion in 2024. Canada supplies 60% of total US oil imports, which translated into an average of 4.6 million barrels per day (b/d) in 2024, with crude oil representing the bulk of it.

Canada’s position as the leading oil supplier to the US has been a phenomenon of the last 20 years. Latin America was the top oil provider to the US in the 1990s and 2000s, with its share of total US imports reaching up to about 40%, until Canada displaced the region in the 2010s (see Figure 1). The increase in Canada’s oil production from Alberta’s oil sands, which tripled between 2008 and 2024, partly explains this outcome. However, declining oil exports from heavy oil producers in Latin America, notably Venezuela and Mexico due to nationalistic policies, particularly in Venezuela, played a significant part.

The US is now the world’s largest oil producer, exporting 11 million b/d of oil and petroleum products. Yet the US still imports about 6.5 million b/d of crude oil, 60% of which is heavy oil from Latin America and Canada. This apparent mismatch is partly a legacy of investments made in the US refining system (particularly in the Midwest and Gulf Coast) when the US was the largest global oil importer, to process heavy crude from Canada, Venezuela, and Mexico.

While Canada supplies about 25% of the US refining system’s oil, it provides almost 70% of the oil processed by Midwest refineries and is transported via pipelines. The lack of alternatives to Canadian oil in this region makes Canada’s energy exports particularly important for the US. In contrast, Mexico’s oil travels seaborne to the Gulf Coast, which has, in theory, the flexibility to substitute Mexican imports with a cheaper alternative—including from Canada, given the proposed tariff differential. Mexico accounts for almost 40% of the Gulf Coast’s oil imports and 5% of total US refining throughput. Despite more logistical challenges, Canadian oil into the Gulf Coast has surged in the last decade, increasing by 300%, filling the hole left by declining Latin American oil production, notably from Venezuela. Canadian oil currently represents 30% of the Gulf Coast’s imported crude oil, and this without the Keystone pipeline.

Tariffs on Mexico’s and Canada’s energy trade, if implemented, raise the risk that other oil producers in the region end up facing similar tariffs. It is possible that higher tariffs on imported crude might also increase the competitiveness of US domestic oil vis-a-vis imported crude, which fits into the Trump administration’s goal of less dependence on foreign energy.

Latin America is a net oil exporter, producing 8% of the world’s production. The region has also been a primary contributor to global oil supply growth in past years, led primarily by Brazil, Guyana, and, to a lesser extent, Argentina. Oil exports are a significant source of fiscal and foreign exchange revenues for Latin America, with export revenues representing more than $160 billion in 2023.

However, with energy systems in transition, being a net oil exporter does not necessarily mean being a net energy exporter. In fact, Latin America has been a net energy importer in dollar terms since 2020, mainly due to its import of petroleum products and natural gas. This energy trade deficit is particularly acute with the US. The US exported an average 2.6 million b/d of oil and about 7 billion cubic feet per day (bcf/d) of natural gas to Latin America in 2024, with pipeline exports to Mexico as the primary portion. Nine countries in Latin America were importing liquefied natural gas (LNG) from the US in 2024: Argentina, Brazil, Chile, Colombia, Dominican Republic, El Salvador, Jamaica, Mexico, and Panama. US energy exports to the region, worth $100 billion in 2023, have increased by 25% since 2019.

While Mexico might not be able to underscore the strategic use of its energy exports as convincingly as Canada during potential tariff discussions with the US, its relevance as a market for US energy exports might ironically become a more effective leverage. Latin America represents 40% of total US gasoline exports and more than 35% of its natural gas exports today. Mexico is by far the largest single market for US refining products (at almost 20% in 2024) and the largest single market for US natural gas exports (at more than 30% last year). The second and third most important destinations for US refining products are China and Canada, at a distant 9% and 7%, respectively, with Canada the second most important market for US natural gas exports, at a distant 13%.

The Trump administration’s position on climate policy and renewables is creating significant uncertainty about the pace of the energy transition. However, energy systems are changing not only because of policy and regulatory action toward low-carbon energy but also because of extreme weather events, competition from cleaner energy technologies, and strong growth in electricity demand.

Abundant hydroelectricity in Latin America has translated into one of the lowest-carbon grids globally. However, drought conditions linked to weather events like El Niño in 2023 and 2024 severely impacted hydroelectricity in northern Brazil, Chile, Colombia, Ecuador, Panama, Peru, and Venezuela, leading to blackouts in some countries and/or a surge in natural gas imports in others. This is a reminder of the region’s reliability risks.

For the region to capitalize on its abundant energy sources, reliability, affordability, and sustainability need to go hand in hand. Improving resilience and tackling bottlenecks across Latin America’s energy value chain are critical to attracting energy-intensive industries and developing a more robust energy trade. This is becoming even more relevant given the uncertainty of whether Trump’s agenda for energy dominance will include Latin America.

The author would like to thank Robert Johnston, Diego Mesa, and Diego Rivera Rivota for their valuable comments and Christina Nelson for her superb editorial work.

In an escalation of trade tensions, Donald Trump threatened to double tariffs on Canadian steel and aluminum to 50 percent this week. This increase would have been in...

Shortly after Donald Trump was elected president of the United States, European Commission President Ursula von der Leyen suggested the European Union could import more US liquefied natural gas...

As Indian Prime Minister Narendra Modi makes his first visit to Washington in the second Trump administration, energy will likely take a front seat in United States-India relations. Due to...

On February 4, the Trump administration imposed an additional 10 percent tariff on all Chinese imports into the United States. China’s Ministry of Commerce responded by announcing new tariffs on US imports,...

A former deputy treasury secretary and a presidential economic adviser on the need to draw a sharper line between open economies and the rest | By Invitation

How the US can reclaim its independence from Chinaâs pharmaceuticals.