This website uses cookies as well as similar tools and technologies to understand visitors’ experiences. By continuing to use this website, you consent to Columbia University’s usage of cookies and similar technologies, in accordance with the Columbia University Website Cookie Notice.

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

It’s hard to overstate how consequential President Trump’s “Liberation Day” tariffs have been for American economic policy. While the administration has paused the steep reciprocal tariffs it announced...

Please join the Women in Energy initiative at the Center on Global Energy Policy at Columbia SIPA for a student roundtable lunch and discussion with Sunaina Ocalan, who will discuss...

Event

• Center on Global Energy Policy

1255 Amsterdam Ave

New York, NY 10027

About Us

We are the premier hub and policy institution for global energy thought leadership. Energy impacts every element of our lives, and our trusted fact-based research informs the decisions that affect all of us.

The Rockefeller Foundation and the Center on Global Energy Policy at Columbia University SIPA jointly organized a workshop from December 3rd to 6th, 2024, in Bellagio, Italy, on how to finance responsible critical mineral supply chains. The event brought together leading experts in critical minerals, including miners, refiners, battery manufacturers, traders, investors, consultants, and representatives from financial and multilateral institutions, under the Chatham House Rule. This roundtable report summarizes the key takeaways from the dialogue that took place.

The discussion at the workshop touched on many topics but focused primarily on three themes: finance, trade, and offtake. These themes encompass the main challenges faced in developing responsibly mined, diversified mineral supply chains: capital expenses (CapEx), operating expenses (OpEx), and revenue planning. Together, CapEx and OpEx are the principal drivers of competitive mining, processing, and clean energy–component manufacturing activity. The participants stated that any credible effort by developed countries to build responsible mineral supply chains will invariably need to address positioning in both areas. At the same time, policy must create strong offtake mechanisms to de-risk investments in mining further and thereby ensure the operational continuity of critical mineral projects.

Accordingly, the participants in the workshop developed an initial framework covering three high-level recommendations for developed market policymakers should they seek to reduce capital and operational barriers to creating responsible critical mineral supply chains. These recommendations are as follows:

Finance: Governments in advanced economies can offer concessional debt, target the use of grants, and strengthen structures that provide equity to critical mineral projects. These financing mechanisms can be paired with policies that promote industry-led efforts to expand and incentivize the use of thematic bonds, vertical integration, and industrial hubs. This two-pronged approach should significantly reduce capital expenses for responsible producers of critical minerals.

Trade: Developed market governments can explore creating a trade infrastructure―including reliable supply chains―to support the diversification and responsible production of critical minerals. This infrastructure requires clear standards, collaboration among mineral-importing countries and between mineral importers and producers, a focus on specific parts of the supply chain, and strong compliance. It can also include penalties for irresponsible operators. Differentiated prices can, in turn, level the playing field for all operators, in contrast to the current situation in which responsible operators often incur higher operating (and capital) costs while receiving the same price as operators that do not adhere to basic standards. A functional trade system can incentivize responsible production and capture the environmental, social, and national security externalities of critical mineral supply chains.

Offtake: Governments in developed countries can devise active offtake policies, potential price stabilization mechanisms, and political risk guarantees to help secure critical mineral supply chains. As the participants pointed out, offtake agreements provide revenue certainty but remain difficult to secure, particularly for smaller producers. Floor price mechanisms and strategic reserves could counter market volatility and predatory pricing but are costly to implement. Expanded political risk guarantees, on the other hand, could help de-risk investments immediately, while stronger diplomatic engagement could help ensure that companies can compete fairly against state-backed rivals operating under different regulatory and ethical standards, specifically with respect to corruption.

The rest of this workshop summary details the discussion that took place around each of the three themes.

Finance

As the participants in the workshop recognized, critical mineral supply chains in developed countries—especially those that are done responsibly—face various challenges in capital markets. Innovative technologies often do not receive sufficient early-stage grants to support their development or mid-stage financing to scale to commercial production. Many greenfield mines and processing facilities lack the cheap, patient capital needed within a long-term, capital-intensive industry. Larger companies often do not have sufficient incentives to process byproducts that are essential to national security because they tend to have volatile prices and are risky and too small to matter on their balance sheets.

The participants stressed that there is no one-size-fits-all approach to capital provision for critical minerals. Different companies and supply chain areas face unique market challenges. Governments must constantly communicate with industry to keep abreast of the unique capital needs of companies and production processes. Policymakers and companies can then work together to find customized solutions for projects that are committed to socially and environmentally responsible standards. Despite the participants’ emphasis on a bespoke approach, they drew several takeaways that apply broadly.

Government loans are vital for many mining companies, given the capital-intensive nature of mining projects. As the participants observed, mining projects have large capital needs: it can often cost more than $1 billion to construct a greenfield mine. Processing is similarly, albeit slightly less, capital-intensive. Although large mining companies can fund new projects with cash, most other producers must turn to debt. These latter companies require significant loans even as they initially face limited cash flow and uncertain profitability. This economic context makes it difficult for aspiring producers to access debt, let alone at a competitive interest rate to make a capital-intensive project financially viable. The participants observed that whereas small and mid-sized companies in the critical minerals industry are generally facing a shortage of debt financing, Chinese companies are thriving due to the state support they receive, including cheap loans.

The participants noted that governments in advanced economies are attempting to address this gap by offering low-interest loans. The US has led the way on this front through the Department of Energy’s Loan Programs Office, which disbursed $2.8 billion in active loans and an additional $3.5 billion in conditional commitments to critical mineral projects as of the end of 2024 under its Advanced Technology Vehicles Manufacturing program.[1] Some participants felt that such loans are helpful and must continue. As they pointed out, government loans can focus on projects that struggle to access debt to cover their capital expenses and can prioritize projects for which public finance crowds in, rather than crowds out, private capital.

Public grants should be approached with caution. The participants noted that these grants can be useful for early-stage innovation but are difficult to scale due to fiscal limitations on government and public sector budgets. With debt and equity, the government can recover or even increase its capital through debt repayments and dividend payouts, respectively. By contrast, public grants are direct public expenditures. As the participants mentioned, the public is also more likely to view them as the government “picking winners.” Finally, public grants do not crowd in capital as effectively as debt or equity since they do not involve a continued government stake in the project. Due to these factors, the participants felt that grants could be used to support early-stage innovation, but other financial tools would be more effective for projects in later stages.

Government equity is one such mechanism that, while still nascent, could be a powerful facilitator of investments in responsible mining. The participants noted that equity investments provide governments with a direct ownership stake in projects. This can help de-risk a project, provide policymakers with a say in key decisions, and offer potentially greater financial upside (although with more risk) than loans. Government equity can also improve a project’s economics by not overburdening it with debt, depending on the level of dilution. This is most relevant for smaller mining companies without significant cash on their balance sheets. Large companies may appreciate the de-risking that government equity can provide but may not need the cash nor want to dilute their ownership. Overall, the participants recognized that equity is not a silver bullet but can be a useful tool for governments in complementing debt.

As the participants observed, in the US, the Development Finance Corporation (DFC) has taken the lead on critical minerals equity investments. But the DFC lacks sufficient processes to scale its equity investments. The DFC scores equity investments as a total loss, similar to grant funding.[2] This fails to recognize the potential for profits and thus limits scalability. Ideally, the DFC would score equity investments based on the expected risk-adjusted return and have stronger processes to disburse equity and receive dividends. The participants felt that Congress and the DFC should urgently revise the DFC’s equity investment criteria accordingly. By implementing structured co-investment models, governments can crowd in private capital rather than displace it.

The participants noted that globally, the public use of equity is not a new idea. State-owned funds such as the Government Pension Fund of Norway and Temasek of Singapore have long used equity as a strategic investment tool. Saudi Arabia’s Public Investment Fund, the Qatar Investment Authority, and the Canada Pension Plan Investment Board have gone even further by directly investing equity into critical mineral projects. In all these cases, state-owned funds benefit from being run like private enterprises but are still subject to government oversight. This allows for the kind of countercyclical funding that is necessary to improve mineral supply resilience. Other countries, including Canada, France, Germany, and Italy, have all established public critical mineral investment funds with equity stakes.[3] These efforts are promising but still nascent.

As the participants observed, government equity investments also face questions around decision-making. Should governments decide directly which projects to invest in? Or should they acquire equity stakes in private funds, which then make the investment decisions? A state-run fund may be the best design in the long term, but building an institutional structure and expertise will take time. In the interim, governments can explore partnering with private funds to make equity investments. This blended public-private model has the potential added benefit of isolating the government from possible public backlash due to any investment failures or based on government involvement in mining. That said, it still requires stringent due diligence by the government and continuous evaluation of the private funds’ decisions and performance.

Tax credits could serve as another efficient source of resource allocation, but they need to be designed and structured properly. The participants observed that mining and processing projects vary greatly in their positioning on industry cost curves. If not designed properly, tax credits for critical mineral mining and processing may go to projects that are already profitable rather than new production that would be uneconomical without them. Public finance should always be targeted, increase efficiency, and avoid expenditure that has no obvious public value. The participants suggested that governments may benefit from undertaking more quantitative assessments of the impact of tax credits on incentivizing new critical mineral production. This could potentially open the door to new types of tax credits that are more efficiently directed towards otherwise uneconomical critical minerals production. A tax credit that incentivizes the development of by-product minerals, for example, could yield significant results. Many critical minerals are by-products of the extraction or processing of larger minerals such as nickel, copper, zinc, lead, platinum, or silver, but producing them requires investing in another production line that, while technically feasible, may incur prohibitive costs.

Some market-led developments are taking shape and could benefit from further government support. As the participants pointed out, these developments include the growth of thematic bonds, including green bonds, the proceeds of which are directed toward environmental and sustainability projects, and sustainability-linked bonds, the proceeds of which―unlike green bonds―are not locked in for specific projects; instead, the issuing company is expected to meet pre-specified key performance indicators covering environmental and/or social metrics. Less than $15 billion worth of thematic bonds has been issued so far by mining companies focused on critical minerals, which is only around 0.3 percent of the total thematic bond market, indicating tremendous room for growth.[4] Mining companies issuing green bonds or other thematic bonds face high compliance costs while typically realizing no cost savings from the issuance due to a lack of a premium relative to conventional bonds. Since bonds must be issued in a certain minimum amount to reach benchmark size, they are typically issued by large companies that can readily access capital rather than smaller companies that need financing. As a rule of thumb, the participants said that bond sizes need to be at least US$ 500 million to be attractive to investors. The participants highlighted that there is still untapped investor demand for thematic bonds. Once large companies set frameworks and precedents, it could become easier for smaller companies to issue such bonds, though they would still need to meet the minimum size to be attractive to investors. An alternative path for smaller companies is to access funding via green loans, for which size is not an issue, but the cost savings potential may be even lower. Governments could encourage companies to tap the thematic bonds market by either providing monetary incentives or de-risking them via guarantees.

Vertical integration is another market-led development that is revolutionizing financial markets in developed countries. Downstream original equipment manufacturers (OEMs), such as General Motors and Tesla, are increasingly interested in financing mining and processing projects.[5] This helps increase capital availability. The role of governments here may be more limited, but the participants observed that policymakers can use their convening power to continue fostering the kind of industry collaboration that facilitates capital allocation. This model has been key to China’s dominance in critical mineral value chains. In Indonesia, for example, nickel processing projects are largely financed by Chinese steelmakers.[6] Governments can also provide public data platforms and market analysis, targeted regulatory flexibility for large projects, and/or low-cost financing or credit guarantees for vertical integration partnerships.

Related to vertical integration, industrial hubs are another important variable in the competitiveness of processing projects. The participants outlined how industrial processing hubs are essential to lowering costs and risk. Unlike the location of mines, the location of processing facilities is not determined by geology. These facilities can be placed in any area with strong infrastructure, streamlined permitting, and economies of scale. Such industrial hubs can occur organically, but the participants highlighted that they are usually the product of industrial policy. Often delineated as special economic zones, they are a key feature of countries with dominance in mineral processing, such as Indonesia for nickel and China for a host of commodities. Industrial hubs reduce not only capital expenditure for processing projects but also operating expenditure, as discussed in greater detail in the next section.

Trade

Trade is an essential part of the critical mineral landscape. Despite countries’ efforts to reshore mineral production, most critical minerals exist within highly globalized markets. Mining, processing, manufacturing, and consumption are spread across the world. Mineral prices in different countries are generally quite similar or at least linked to similar benchmarks.

According to the participants, the globalized nature of critical mineral markets poses key challenges to policymakers. Governments can promote free markets at home and implement regulations to ensure that domestic production is environmentally and socially responsible. But policymakers have fewer tools to incentivize such behavior beyond their borders.

The participants suggested that existing trade bodies, such as the World Trade Organization (WTO), have failed to address contentious issues related to critical minerals over the last few decades. They pointed to various examples of these failures. The Democratic Republic of the Congo (DRC), the world’s leading producer of cobalt, has a long history of precarious labor conditions.[7] Indonesia’s surging production in nickel mining and processing comes at a tremendous environmental cost.[8] Several participants stressed that China’s dominance of the processing of many critical minerals is closely tied to opaque state support as well as low environmental and labor standards.

As the participants observed, the lack of enforceable, synchronized global standards for critical minerals creates two major challenges. The first is an uneven playing field. Projects in certain countries may have an operating advantage due to lower labor standards and environmental compliance. This leads to the second challenge: countries with heavy state-backed financial support will increasingly dominate markets since projects in these countries have artificially low operating costs. For these reasons, critical mineral production is currently dominated by “irresponsible” producers. Facilitated by the policy landscape mentioned earlier, the DRC mines 76 percent of the world’s cobalt, Indonesia mines 59 percent of the world’s nickel, and China processes over 80 percent of the key minerals gallium, graphite, and rare earth elements.[9]

Developed market governments have a strategic interest in building more responsible and diversified critical mineral supply chains, for which trade is key. The participants observed that the trade toolkit of these countries, which are primarily critical mineral consumers, consists of three main tools: free trade agreements, tariffs, and restrictions on market access. The Participants discussed all three, and they ultimately agreed that a mix of them will be needed to construct a new trade infrastructure that rewards responsible mineral producers, penalizes irresponsible producers, and incentivizes responsible production. This, in turn, can diversify supply chains by creating more of a level playing field between countries.

The participants did not necessarily reach a consensus on the specificities of such a trade system, but they did identify several guiding principles. These principles include using performance standards, implementing strong verification mechanisms, balancing different trade tools, fostering collaboration between consuming countries, adopting a targeted approach to restricting the market access of worst offenders, and striving for political durability, each of which will be discussed in turn.

Performance standards must serve as the foundation for trade in critical minerals. The articipants pointed out that the mining industry currently has a variety of performance standards, each with its advantages and disadvantages. These standards include the International Finance Corporation (IFC) Performance Standards, the Initiative for Responsible Mining Assurance (IRMA) Standard, and the Global Industry Standard on Tailings Management (GISTM). Other important frameworks include the OECD Due Diligence Guidance for Responsible Minerals from Conflict-Affected and High-Risk Areas (technically a guidance but functions as a standard), the Extractives Industry Transparency Initiative (a voluntary framework), the International Council on Mining and Metals’ Mining Principles (voluntary principles), and the upcoming Consolidated Mining Standard, which combines four existing standards (The Copper Mark, Mining Association of Canada’s Towards Sustainable Mining, World Gold Council’s Responsible Gold Mining Principles, and the aforementioned ICMM Mining Principles).

Some participants argued that standards for trade should strive for simplicity. Simple standards are easier for companies to comply with and for governments to verify. For example, the OECD Due Diligence Guidance, which is a risk-based framework, has been widely adopted due to its relative simplicity. Adoption of the IRMA standard, meanwhile, has been slower due to its strict and comprehensive performance standards.

It might be more practical and feasible for any new trade system to penalize the least responsible producers rather than reward the most responsible producers. The participants highlighted how markets already offer slight premia to low-carbon products, and these premia will likely continue to grow. The market now needs policy support to lower the profits and reduce the competitiveness of the least responsible producers. A trade system may not require best-in-class performance standards; it can instead be based on simple, easily verifiable standards that are achievable for a meaningful portion of the market. These standards could reward data transparency and continuous improvement instead of using strict pass/no-pass thresholds.

Verification is an essential complement to any standard. The participants suggested thatas governments select a standard for trade rules, they must build internal capabilities to verify compliance. Governments can also use, or mandate, third-party audits. For smaller producers, it may make sense for host countries to carry out and collate reporting. It will likely take time for companies and governments to build the necessary infrastructure to monitor, measure, report, and verify social and environmental performances. However, this process will undoubtedly lead to more transparent markets. If paired with trade incentives, it will also lead to more responsible markets.

Policymakers can use a mixture of free trade agreements, tariffs, and restrictions on market access to influence the competitiveness of critical mineral operations. As the participants pointed out, free trade agreements and tariffs need to be balanced carefully. In many developed countries, tariffs are too low for free trade agreements to influence trade flows, though the trade war initiated by the Trump administration in the US may change this going forward. Higher tariffs are likely required for critical minerals, but rather than applying them to countries as a whole, they can be applied to companies that do not meet certain performance standards, such as traceability.Alternatively, tariffs can be applied generally, with exemptions for producers that meet performance standards. Complete restrictions on market access can be levied against producers that have been established as “bad actors,” meaning those that have caused extreme social or environmental damage. A dedicated government entity can maintain the list of such actors based on a strict set of criteria to minimize subjectivity. These criteria should include forced labor and child labor provisions.

Trade tools can only be effective if they are implemented by a large portion of global consumers. As such, collaboration among countries is essential, and an effective trade architecture must be multilateral.The US, for example, only imports around 4 percent of the world’s processed cobalt and nickel (excluding imports in embedded products[10]). That share of consumption is too small to influence markets. As The participants discussed, governments of advanced economies can ally together to wield more power as a consuming bloc. At the very least, this will require agreeing on a common set of standards. Countries can use existing convening platforms, such as the Minerals Security Partnership, to build alliances.

Trade mechanisms should also be customized for commodities. The participants observed that each mineral has different operating cost curves, market challenges, and levels of market concentration. Tariffs for minerals with steep cost curves, for example, should generally be higher than tariffs for minerals with flatter cost curves. Similarly, different policies are required for different minerals, depending on their levels of market concentration. For monopolistic markets, price floors and other subsidies may be more practical than trade policies, given the lack of substitute producers.

The participants pointed out that the critical minerals trade is growing increasingly fractured and politicized. These trends will likely continue as critical minerals become increasingly important to national security and the global geopolitical landscape continues to fragment. The current trajectory of trade in critical minerals is marked by unpredictability, bilateralism, inefficiency, and risk. More importantly, trade policies are failing to make critical mineral production more responsible and geographically diversified.

The trade architecture outlined above would present a more orderly, efficient, and effective way for developed market governments to achieve their goals. However, as the participants observed, trade policy relies on cooperation between not only countries but also domestic political parties. Today’s critical mineral supply chains were formed over decades; they will also require decades to be reshaped. A successful trade system must have longevity for the industry to react. It must, therefore, be politically durable. While political compromise may take more time, such compromise is required for governments in developed countries to increase the probability of long-term success.

Offtake

Offtake agreements serve as a critical financial instrument by increasing revenue predictability for miners and processors. Unlike traditional financing structures, they help secure long-term commitments from buyers, thereby reducing investment risk and improving project bankability. The participants noted that securing offtake agreements remains challenging for smaller and mid-sized mining companies due to their customers’ uncertain demand, which is partly the result of concerns about geopolitical risks. In economies where such risks are heightened, projects also tend to face a substantially higher cost of capital that is exacerbated by underdeveloped domestic and regional capital markets. Several participants agreed that merely being located in Africa drives up the cost of capital, even if that is often not rational. As a result, developed market governments could consider offtake programs to de-risk offtake commitments for both producers and buyers. Public-private partnerships could serve as intermediaries to help structure multi-stakeholder agreements that distribute risk and increase the number of backers of a single project.

As the participants noted, a more structural approach to stabilizing critical mineral supply chains should also address the inherent volatility in these markets. Many critical mineral projects in developed countries are high on global cost curves and become uneconomical during downturns, making it more difficult for companies to invest in them countercyclically. Without interventions to stabilize prices, supply chains in these countries will continue to struggle against competitors that can then benefit from boom-and-bust cycles.

The participants identified several potential solutions to these issues.

Afloor pricing mechanism backed by governments could help prevent producers from being driven out of the market by cyclical price collapses or predatory pricing tactics. As the participants pointed out, floor pricing mechanisms would ensure that critical mineral producers do not fall below an economically viable threshold during market manipulations, with the difference between market price and floor price covered through strategic purchasing by a government or a market stabilization fund. These mechanisms could be triggered by clear benchmarks, such as cost curves, supply chain dependencies, and/or evidence of non-market behavior, including state-backed oversupply. While there are many pitfalls to consider, such systems could potentially help during periods of low or high prices due to market manipulation. The participants warned, however, that such a floor price system would neither prevent commodity cycles nor resolve the challenges associated with price volatility for most of the global industry.

The active use of strategic commodity reserves, where governments build stockpiles of critical minerals to be deployed during supply squeezes, price collapses, or geopolitical disruptions, could be actively managed (i.e., selling during high-price periods and buying during market downturns to maintain price stability). The participants suggested that a well-managed strategic reserve could reduce China’s ability to use its dominance in refining and midstream processing and its stockpiles as a geopolitical tool. To be effective, stockpiling systems would need to be well-designed and ideally coordinated amongst major mineral importers to reach scale. In the participants’ view, a good place to start would be to update the national defense stockpiles of North American and European countries.

Political guarantees could be expanded to immediately help de-risk projects. As the participants observed, firms in developed countries operating in mineral-rich but politically unstable countries face high exposure to risks such as conflict, nationalization, contract renegotiation, expropriation, and governance challenges. Unlike Chinese companies, which are often backed by sovereign guarantees and state-driven diplomacy, mining firms in advanced economies face the full financial burden of these risks. The participants suggested that expanding the use of political risk guarantees and insurance mechanisms could provide an alternative to the state-backed financing models that China deploys. The US Development Finance Corporation and allied export credit agencies could expand their insurance and guarantee programs to cover political risk in mining projects critical to allied supply chains. These guarantees could include coverage against expropriation, contract breaches, and disruptions due to geopolitical interference. A broader initiative, such as a Multilateral Mining Investment Risk Facility, could pool risks across multiple jurisdictions to lower financing costs for high-risk but strategically important projects. This would also allow certain risk-averse DFIs to contribute to a functioning solution without becoming too exposed themselves.

Developed market governments can be more active diplomatically to level the playing field beyond financial risk. The participants pointed out that mining companies in developed countries face regulatory disadvantages compared with their Chinese counterparts. The Foreign Corrupt Practices Act (FCPA), for example, imposes strict anti-bribery regulations on US companies but does not apply to Chinese firms, affording the latter a competitive advantage in resource deals in high-risk jurisdictions. Mining companies that refuse to engage in corruption often lose resource concessions to competitors that operate outside these constraints. This has led to significant losses for mining projects of American and other non-Chinese firms. To prevent this structural disadvantage from limiting supply chain development in advanced economies, governments can establish a direct line between mining companies and diplomatic authorities to trigger interventions when Western firms are being outcompeted through corrupt practices. A dedicated channel between miners and the US State Department, or institutions in allied countries, should allow firms to escalate cases where compliance with anti-corruption standards puts them at a disadvantagein foreign markets. Rather than pausing the FCPA, as the Trump administration has now done, miners believe that stronger communication could be an important solution so long as it enables rapid diplomatic responses coupled with effective enforcement, including trade restrictions and diplomatic consequences.

More broadly, the US and its allies can integrate anti-corruption standards into trade and investment frameworks for critical minerals. The participants felt that procurement policies could perhaps prioritize companies that adhere to transparency and anti-corruption commitments and ensure that firms not following FCPA regulations are systematically disadvantaged. They also suggested that policymakers could consider targeted trade measures that prohibit imports of minerals extracted through bribery or corruption, similar to existing bans on conflict minerals and those suggested above regarding forced and child labor. Absent such measures, mining companies in advanced economies will undoubtedly continue to operate at a structural disadvantage in critical mineral markets where corruption remains a primary mechanism for securing resource access.

Next Steps to Improve Financing of Responsible Critical Mineral Mining

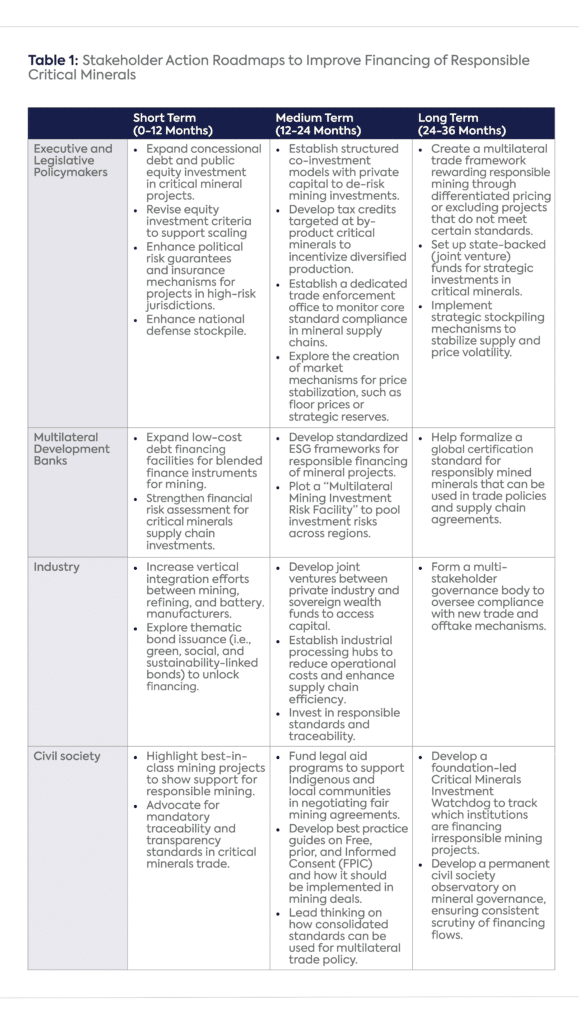

The workshop produced a set of recommendations for policymakers, MDBs, and industry to facilitate financing for responsible critical mineral mining. These are outlined in Table 1.

The workshop also produced a set of short-term, medium-term, and long-term recommendations for the critical mineral research community, including the Rockefeller Foundation and CGEP.

In the short term:

Develop targeted education programs for policymakers on financing mechanisms, trade policies, and offtake strategies for responsible mining.

Host closed-door policy briefings for key US, EU, and other government officials on critical minerals investment challenges.

Establish a high-level Task Force on Responsible Mining Finance that brings together the world’s largest investors, mining firms, and policymakers.

Develop a coalition of supply chain and financial experts to advise policymakers on investment in strategic minerals projects.

In the medium term:

Publish practical policy guides (e.g., “Critical Mineral Financing 101”) aimed at decision-makers in government and multilateral institutions.

Engage with investors to define a responsible financing taxonomy, including green bonds, concessional loans, and blended finance tools.

Host a global roundtable on “De-risking Investments in Responsible Critical Minerals” in partnership with sovereign wealth funds and DFIs.

Publish data-driven reports on the capital needs of responsible mining, including a breakdown of gaps in debt, equity, and concessional finance.

Develop case studies on innovative financing models (e.g., sovereign-backed equity funds and joint ventures) to inform policymakers and investors.

Convene a working group on price stabilization mechanisms, including strategic stockpiles and floor price guarantees.

In the long-term:

Help enshrine free, prior, and informed consent (FPIC) principles into legal frameworks governing mining projects.

Support the development of a dedicated trade enforcement mechanism to prevent the worst offenders of standards from accessing Western markets.

Establish an annual “Critical Minerals Finance Forum” similar to the UN’s Congress of the Parties (COP) meetings but focused on mineral financing.

Work with indigenous groups and civil society to design better benefit-sharing models in mining investments.

Establish a Critical Minerals Policy Fellowship to train future leaders in government, industry, and finance.

Create a global consortium of universities, think tanks, and industry leaders to institutionalize policy best practices in financing responsible minerals.

Dr. Tom Moerenhout is a research scholar at SIPA’s Center on Global Energy Policy and an Adjunct Associate Professor at Columbia University’s School of International and Public Affairs. He is also a Senior Advisor at the World Bank, and a Senior Associate at the International Institute for Sustainable Development. He also teaches at NYU Stern School of Business and is a Scholar in Practice at Columbia University’s Committee on Global Thought.

Tom’s research expertise and practical engagements focus on geopolitics, political economy, and international economic law. Tom’s main expertise lies in the role of trade, investment, and industrial policies of relevance to the energy transition, the sustainability dimension of economic globalization, and the economic development of resource rich countries. He has published extensively on sustainable development and energy policy reforms in developing and emerging economies, specifically on energy subsidies, critical minerals, and electric mobility.

For over 12 years, Tom has been responsible for conducting strategic research and market intelligence for governments and development practitioners. In recent years, he has provided in-country support to energy and development policy reforms in India, Nigeria, Lebanon, Egypt, the US, Iraq, Iraqi Kurdistan, Morocco, and Jordan. Tom has worked closely with various organizations such as the World Bank, OECD, OPEC, IRENA, UNEP, ADB, GIZ, Bill and Melinda Gates Foundation, Nestle, and Greenpeace.

Tom holds two master’s degrees and a PhD at the Graduate Institute of International and Development Studies in Geneva. Prior to joining Columbia University, he was a visiting fellow at the LSE Department of Government and an Aramco-OIES fellow at the Oxford Institute for Energy Studies. In 2015-2016 he was a Fulbright fellow at Columbia University. In his free time, Tom enjoys reading, good food, football, skiing, and chess.

Dr. Gautam Jain is a Senior Research Scholar at the Center on Global Energy Policy (CGEP) of Columbia University’s School of International and Public Affairs (SIPA). He focuses on the role of financial markets and instruments—including thematic bonds, blended finance structures, and carbon markets—in the energy transition, with an emphasis on emerging economies.

Dr. Jain has an extensive background in the financial industry where he covered emerging markets as a portfolio manager and strategist. He has worked at asset management firms and an investment bank, including The Rohatyn Group, Barclays Capital, and Millennium Partners. He has helped manage emerging market local debt and hard-currency bond portfolios, encompassing currencies, interest rate instruments, and sovereign credits. He specialized in portfolio construction and asset allocation incorporating macroeconomic, policy, and political developments in emerging markets.

He holds a Ph.D. in Operations Research from Columbia University. He also has an M.S. in Industrial Engineering from Iowa State University and a B.Tech. in Mechanical Engineering from the Indian Institute of Technology, Bombay. He is a CFA charter holder, a Cornell EMI Fellow, an Adjunct Professor at Columbia University’s School of International and Public Affairs, and a consultant for the United Nations to support the workstream of the Global Investors for Sustainable Development (GISD) Alliance on “Tackling Local Currency Risk”.

He has co-authored publications in the Journal of Derivatives, the Journal of Banking and Finance, the Journal of Applied Probability, Probability in Engineering and Informational Science, and the International Journal of Production Economics. He has also contributed chapters for the 2020 and 2021 Cornell EMI Annual Reports.

Cina Vazir serves as an independent consultant and advisor for policymakers, companies, non-profits, and investors in the mining and energy sector.

Most recently, Cina was a Managing Consultant at Wood Mackenzie, where he advised corporations on complex decisions related to capital allocation, strategy, and public-private negotiations for minerals, oil, and gas. Before that, he worked on natural resources across a variety of organizations including Rio Tinto, Steyn Reddy Associates, and the World Bank. In these roles, he covered topics ranging from portfolio strategy to industrial policy and ESG. Cina first entered the commodity industry as a successful retail investor in junior mining equities.

Earlier in his career, Cina served in the U.S. Peace Corps and later worked in strategy consulting. He holds a Bachelor of Arts from the University of Michigan and a Master in Public Policy from the Harvard Kennedy School.

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

President Donald Trump has made energy a clear focus for his second term in the White House. Having campaigned on an “America First” platform that highlighted domestic fossil-fuel growth, the reversal of climate policies and clean energy incentives advanced by the Biden administration, and substantial tariffs on key US trading partners, he declared an “energy emergency” on his first day in office.