“Everything up in the air”: LNG, the Strait of Hormuz, and Central & Eastern Europe’s energy future

"LNG shipments to Central & Eastern Europe are reliable as long as those gas markets are not overly dependent upon one supplier."

Get the latest as our experts share their insights on global energy policy.

On February 28, the US and Israel launched new attacks on Iran targeting primarily the country's leadership, security forces, and missile program.

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

It’s been a head-spinning day in the Iran war. Earlier today, following a temporary truce between Lebanon and Israel, Iran announced that the Strait of Hormuz would be...

Find out more about our upcoming and past events.

The Columbia Global Energy Summit 2026 is an annual event dedicated to thought-provoking discussions around the critical energy and climate challenges facing the global community.

Insights from the Center on Global Energy Policy

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. Rare cases of sponsored projects are clearly indicated.

For a full list of financial supporters of the Center on Global Energy Policy at Columbia University SIPA, please visit our website at Our Partners. See below a list of members that are currently in CGEP’s Visionary Circle. This list is updated periodically.

China’s demand for oil, long an important driver of global oil demand growth, slowed dramatically during January–September 2024. Between 2000 and 2023, China accounted for 50 percent of the growth in world oil demand, averaging an annual increase of 518,000 barrels per day (bpd).[1] However, analysts expect China’s oil demand will increase by far less in 2024. The International Energy Agency (IEA) now projects that the country’s oil demand will grow by 180,000 bpd this year, down from the 410,000 bpd it projected in July.[2] Similarly, Energy Intelligence now sees China’s oil demand increasing by fewer than 100,000 bpd, down from the 450,000 bpd it expected in January.[3] Looking ahead, ongoing gains will be muted by both cyclical and structural factors, with the latter already starting to weigh on consumption. In this Q&A, the authors discuss why China’s oil demand is slowing down, whether China’s stimulus will boost demand, and what the oil market implications are.

China’s oil demand is growing more slowly because of rising sales of new energy vehicles (NEVs)—a category that includes battery electric vehicles, plug-in hybrid electric vehicles, and fuel cell electric vehicles—China’s high-speed rail (HSR) network, and a property sector slump.

Gasoline demand growth is being reduced by NEVs. NEVs accounted for 38.6 percent of new car sales in China from January–September 2024, up from 31.6 percent for 2023.[4] New policy support is likely to further boost NEV sales. In August, Beijing doubled the subsidies for trading in old NEVs and internal combustion engine (ICE) vehicles for new NEVs and more fuel-efficient ICE vehicles.[5]

China’s HSR network has also taken a bite out of China’s oil consumption, to include road transport and aviation fuels. The IEA estimates that China would have needed an additional 300,000 bpd of oil had growth in the country’s railway use facilitated by HSR investment not happened.[6]

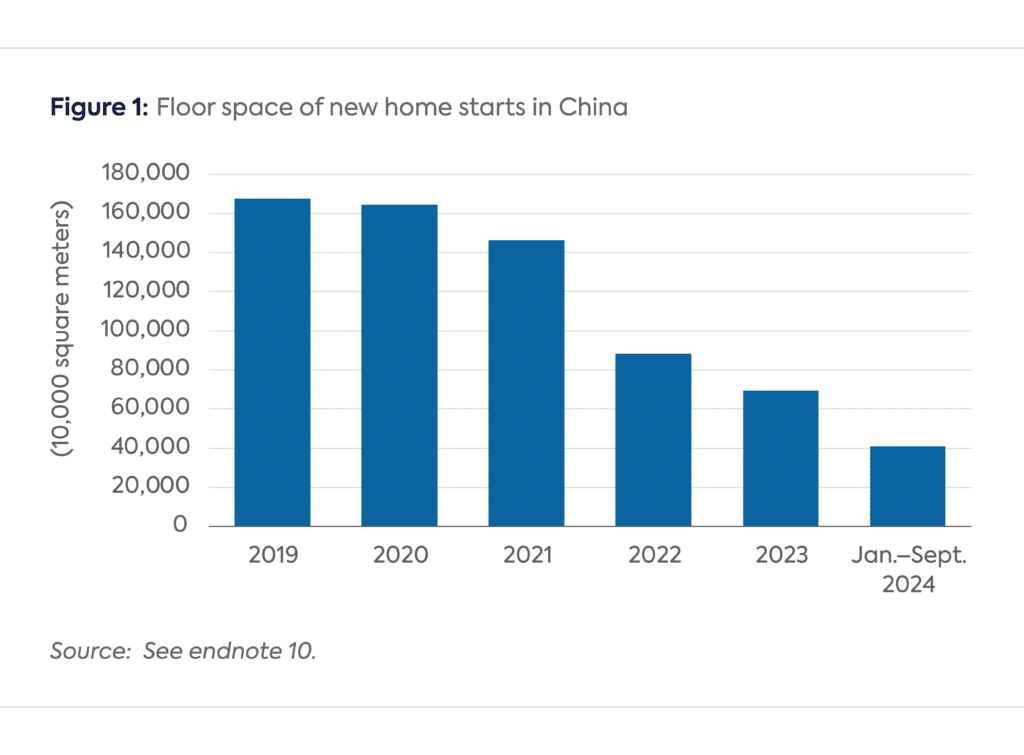

China’s property sector slump and liquefied natural gas (LNG) truck sales are weighing on demand for diesel, the largest component of China’s oil product consumption.[7] The floor space of new home starts decreased by almost 60 percent between 2019 and 2023 (see Figure 1). This decline undoubtedly has negatively impacted demand for diesel, which fuels construction equipment and the transport of construction materials.[8] The share of natural gas trucks in heavy-duty truck sales jumped from 9 percent in 2022 to 42 percent in January–August 2024.[9]

During January–June 2024, China’s gasoline consumption grew by just 0.32 percent over January-June 2023, while diesel consumption decreased by 3.52 percent over January–June 2023.[11] Gasoline and diesel could cease to drive China’s oil demand growth in the next few years, if they have not done so already. A PetroChina research institute said that demand for both fuels peaked in 2023 (see Table 1). Other analysts expect gasoline and diesel demand to peak before 2030. Even if demand for liquefied petroleum gas and other products such as jet fuel and petrochemicals continues to grow for several years, China’s total oil demand may still peak before the end of the decade.

Commodity Insights S&P Global

International Energy Agency

Kpler

PetroChina Planning & Engineering Institute

Vitol

Diesel

2027

2025

2026

2023

Gasoline

2025

2024

2023

2024 or 2025

Sources: See endnote [12].

Beijing has been announcing stimulus measures since late September, including:

Although Minister of Finance Lan Fo’an said in October that more stimulus policies would follow the conclusion of the National People’s Congress Standing Committee meeting on November 8,[17] Beijing did not release any. Instead, Beijing announced a 10 trillion-yuan ($1.4 trillion) debt-swap package to help local governments move off-the-books debt to lower-interest, on-the-books debt.[18] Minister Lan said more stimulus will come next year.[19]

The stimulus measures are unlikely to provide a strong boost to oil demand because their purpose is to steady the economy and achieve this year’s growth target of around 5 percent rather than stimulate rapid economic growth.[20] Indeed, the core mission of the stimulus is to stabilize the property sector because of its widespread impact on the rest of the economy.[21] The Politburo said as much in the readout of its late September meeting, pledging to stop the decline of the property market.[22]

Regarding implications for China’s oil demand, what is not included in the stimulus package is arguably more important than what is in it. The package does not include projects likely to strongly support oil demand such as large-scale infrastructure projects that featured in the investment-led stimulus Beijing began in November 2008 in response to the global financial crisis.[23] Also absent are many new housing construction projects, since Beijing’s focus is on the completion of unfinished homes and supporting sales, per the stimulus measures listed above and the Politburo’s statement that the government will strictly limit the construction of new housing projects.[24]

The slowdown ahead has implications for the oil market and oil prices. For world oil consumption to continue to grow at the historical one-plus million bpd per year rate, other countries/regions such as Africa, India, and Southeast Asia will have to achieve nearly all these gains. This is especially true given large markets such as the US and Europe may also be close to peak oil demand.

Some industry estimates, including OPEC’s, have total oil consumption increasing through the 2030s and beyond 2040, to over 120 million bpd.[25] Other agencies have demand approaching a peak between 2025 and 2030 or between 2030 and 2035[26] at a level of 105–108 million bpd, with the slowdown in China a key factor. Oil demand in 2024 is expected to average 102.5–103 million bpd,[27] meaning if the prior estimate of peak volume is correct, only about 2–5 million bpd of additional growth is expected.

This relatively limited total future growth would mean that the world is likely well supplied with oil over the coming decade. The OPEC-plus group of countries currently has 5–6 million bpd of spare capacity,[28] and non-OPEC-plus supply growth is expected to continue to rise over the coming years, led by the Americas (slowing in the US but increasing in Brazil and Guyana). This oversupply may lead to a much lower oil price range than that of the last few years—potentially in the $70s per barrel or lower. Conversely, if demand rapidly increases toward the 110 million bpd threshold or higher in the next 5–10 years, as estimated by OPEC for example, the market is likely to remain somewhat tighter and could support prices closer to $80-plus per barrel.

CGEP’s Visionary Circle

Corporate Partnerships

Occidental Petroleum Corporation

Tellurian Inc

Foundations and Individual Donors

Anonymous

Anonymous

the bedari collective

Jay Bernstein

Breakthrough Energy LLC

Children’s Investment Fund Foundation (CIFF)

Arjun Murti

Ray Rothrock

Kimberly and Scott Sheffield

[1] https://www.energyinst.org/statistical-review

[2] https://www.reuters.com/business/energy/iea-cuts-2024-oil-demand-growth-forecast-china-slowdown-2024-09-12/

[3] https://www.energyintel.com/00000192-4939-d673-a7b3-cb3dabfc0000

[4] https://www.jfdaily.com/news/detail?id=807987; https://www.scmp.com/business/china-business/article/3260353/petrochina-rapid-ev-uptake-means-oil-consumption-transport-peak-next-year-latest-china

[5] https://english.www.gov.cn/news/202408/16/content_WS66bf5a54c6d0868f4e8e9ff6.html; https://www.reuters.com/business/autos-transportation/china-car-sales-rise-snapping-five-month-decline-subsidy-boost-2024-10-12/

[6] https://iea.blob.core.windows.net/assets/493a4f1b-c0a8-4bfc-be7b-b9c0761a3e5e/Oil2024.pdf, p. 39

[7]https://m.cpca.com.cn/4064/202409/14820.html

[8] https://www.iea.org/commentaries/china-s-slowdown-is-weighing-on-the-outlook-for-global-oil-demand-growth

[9] https://www.ft.com/content/301f0161-e9a2-4b3b-bfdc-d838e765aceb

[10] https://www.stats.gov.cn/english/PressRelease/202001/t20200119_1723643.html; https://www.stats.gov.cn/english/PressRelease/202101/t20210119_1812512.html; https://www.stats.gov.cn/english/PressRelease/202201/t20220118_1826502.html; https://www.stats.gov.cn/english/PressRelease/202301/t20230118_1892298.html; https://www.stats.gov.cn/english/PressRelease/202402/t20240201_1947107.html; https://www.stats.gov.cn/english/PressRelease/202410/t20241025_1957149.html

[11] http://news.cnpc.com.cn/system/2024/07/11/030136907.shtml

[12] https://www.spglobal.com/commodityinsights/en/market-insights/blogs/oil/101424-china-peak-oil-demand-looms#:~:text=State%2Downed%20PetroChina’s%20Planning%20%26%20Engineering,b%2Fd%20gasoil%20this%20year; https://iea.blob.core.windows.net/assets/493a4f1b-c0a8-4bfc-be7b-b9c0761a3e5e/Oil2024.pdf, p. 39; https://www.kpler.com/blog/chinas-gasoil-demand-is-set-to-peak-in-2026-as-sweeping-changes-in-the-transportation-sector-take-a-toll; https://www.bloomberg.com/news/articles/2024-09-09/vitol-sees-chinese-gasoline-demand-peaking-this-year-or-next.

[13] https://www.economist.com/finance-and-economics/2024/09/27/at-last-china-pulls-the-trigger-on-a-bold-stimulus-package

[14] https://www.economist.com/finance-and-economics/2024/09/27/at-last-china-pulls-the-trigger-on-a-bold-stimulus-package

[15] https://www.bloomberg.com/news/articles/2024-09-24/china-to-boost-capital-at-mega-banks-for-first-time-in-a-decade

[16] https://www.cnbc.com/2024/10/17/chinas-housing-ministry-to-hold-briefing-on-efforts-to-bolster-the-property-market.html; https://english.www.gov.cn/news/202410/17/content_WS67111067c6d0868f4e8ebfd0.html

[17] https://www.bloomberg.com/news/articles/2024-10-26/china-s-stimulus-aims-to-boost-consumption-top-official-says

[18] https://www.bloomberg.com/news/articles/2024-11-08/china-unveils-839-billion-debt-swap-to-rescue-local-governments

[19] https://www.bloomberg.com/news/articles/2024-10-26/china-s-stimulus-aims-to-boost-consumption-top-official-says?sref=npQiEL5j&mc_cid=8c5fec622f&mc_eid=2b4248130b

[20] https://www.wsj.com/world/china/behind-xi-jinpings-pivot-on-broad-china-stimulus-08315195

[21] Thank you to Arthur Kroeber for this point and helpful discussions about the stimulus.

[22] https://www.bloomberg.com/news/articles/2024-09-26/china-holds-surprise-politburo-meeting-on-economy-amid-slowdown

[23] https://www.hoover.org/sites/default/files/research/docs/CLM28BN.pdf, p. 2

[24] https://www.bloomberg.com/news/articles/2024-09-26/china-holds-surprise-politburo-meeting-on-economy-amid-slowdown

[25] https://publications.opec.org/woo/chapter/129/2356

[26] https://www.iea.org/reports/world-energy-outlook-2024

[27] https://www.iea.org/reports/oil-market-report-october-2024

The US-Israeli war against Iran highlights the Gulf’s dual role as the backbone of global energy supply and a major source of systemic risk.

The war in Iran has significantly enhanced Latin America's geopolitical advantage as a reliable source of hydrocarbon resources.

Media reports suggest the Trump Administration is considering restrictions on US oil exports.

Iran has among the world's largest natural gas resource bases, but its ability to supply regional and global markets is constrained by sanctions, underinvestment, and limited export infrastructure.

Within days of the initial U.S. and Israeli attack on Iran on February 28, 2026, the world was plunged into an energy crisis.

Anne-Sophie Corbeau and leading experts explore how Europe's gas sector is being reshaped by geopolitical shocks.