Current Access Level “I” – ID Only: CUID holders, alumni, and approved guests only

Read more about the campus status level system and campus access information.

This website uses cookies as well as similar tools and technologies to understand visitors’ experiences. By continuing to use this website, you consent to Columbia University’s usage of cookies and similar technologies, in accordance with the Columbia University Website Cookie Notice.

La récente flambée des cours du brut ne sera pas suffisante pour redresser l'économie russe à long terme. Elle octroie néanmoins à Moscou un puissant lev...

In energy markets, all eyes are on the Strait of Hormuz. As of March 11, 2026, this vital passage is effectively closed to tanker traffic, stranding almost a...

This roundtable is open only to currently enrolled Columbia University students. To register, you must sign in with your UNI. The Center on Global Energy Policy at Columbia...

Event

• Center on Global Energy Policy

1255 Amsterdam Ave, New York, NY 10027

About Us

We are the premier hub and policy institution for global energy thought leadership. Energy impacts every element of our lives, and our trusted fact-based research informs the decisions that affect all of us.

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. Rare cases of sponsored projects are clearly indicated.

For a full list of financial supporters of the Center on Global Energy Policy at Columbia University SIPA, please visit our website at Our Partners. See below a list of members that are currently in CGEP’s Visionary Circle. This list is updated periodically.

The US Federal Reserve (Fed) commenced its monetary easing cycle on Wednesday with an aggressive 50 basis points policy rate cut. The United States is not alone in this respect. Among the majors, central banks of the Eurozone, England, Canada, Switzerland, and Sweden have already embarked on their rate-cutting cycles, with some looking to increase the pace.[1]

With inflation broadly falling back into the central banks’ target ranges, it is safe to say that the inflationary environment that followed the 2020 COVID-19 pandemic is now behind. Indeed, with the risk of economic slowdown increasing, global interest rates are expected to continue falling going into next year.

The sharp increase in interest rates over the past couple of years to tame inflationary pressures led to higher costs of capital which impacted many industries. Stocks of renewable energy companies, in particular, suffered heavily. It is therefore fair to ask whether the reversal in the interest rate cycle will spur a recovery in the renewable energy sector. This blog addresses this question and concludes that while the interest rate environment is decisively turning supportive, other factors may continue to weigh on the sector preventing a turnaround at least in the near term.

Rally in the Renewable Energy Sector Followed by a Swoon

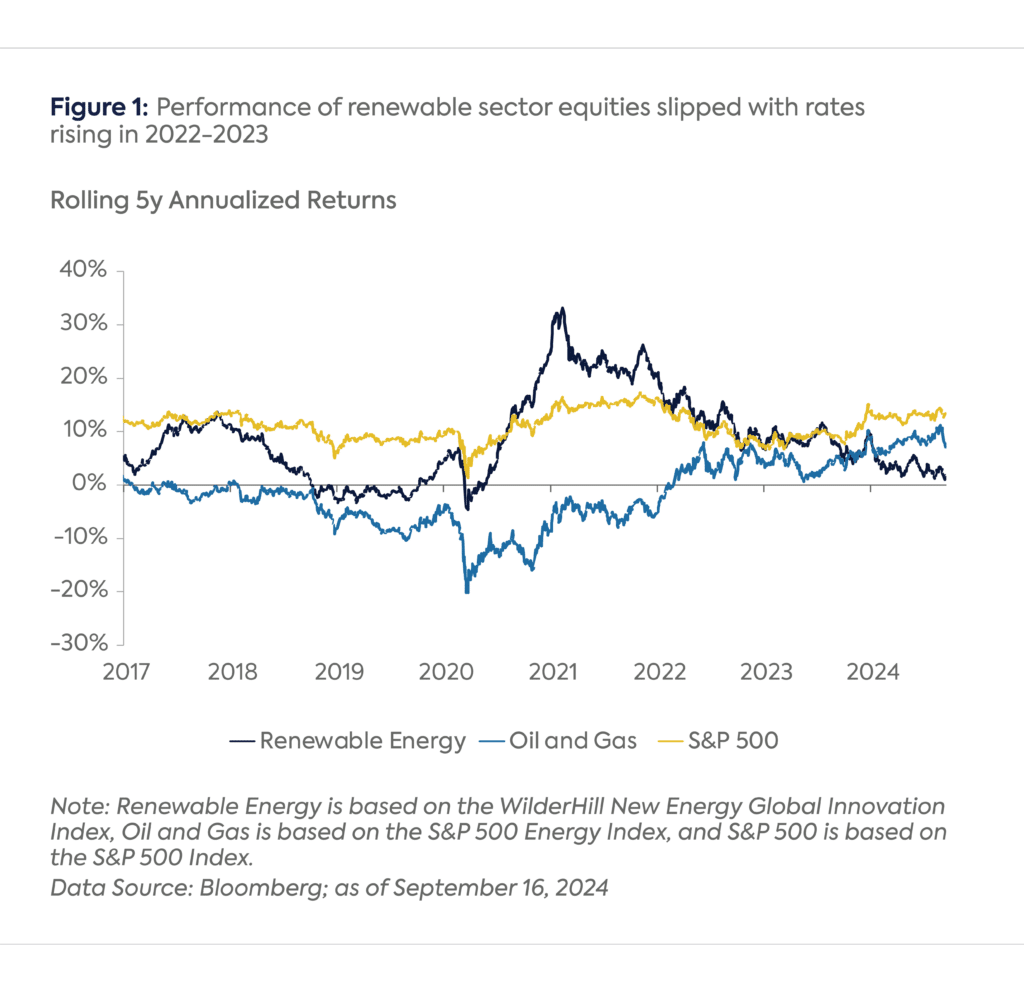

Equities in the renewable energy sector got a big boost in 2020, with the returns from the sector continuing to be high in 2021 and early 2022 relative to the pre-pandemic period (see Figure 1). Several factors were behind this performance:

The cost of producing electricity from solar PV and onshore wind, which had been coming down for over a decade, dropped below that of traditional sources for the first time in many countries in 2019-20.[2]

Policy support in many countries helped lower the cost of deployment of renewable energy sources. The impending expiration of some of these tax credits and subsidies at the end of 2020 in a few countries, prominently in China and the United States, spurred growth in the sector.[3]

The growing awareness that climate change is caused by greenhouse gas emissions amplified by the onset of the COVID-19 pandemic, provided an impetus to adding renewable energy sources even though energy demand was low that year.[4]

The expected support for climate policies from the incoming Biden administration in the United States, especially in contrast with the outgoing Trump administration, was supportive for the sector going into 2021.

The performance of the renewable energy sector started reversing in 2022, which coincided with the aggressive rate-hiking cycle by the Fed and other central banks around the world. In the United States, the policy rate was raised from close to 0% to over 5% in less than 18 months. The increase in interest rate impacted stock valuations across the board, but it was particularly penalizing for renewable energy companies.

Companies in the sector require high upfront capital investment with cash flows expected in future years. The sharp rise in interest rates implied a much lower present value of these cash flows and, therefore, stock valuations. Even the significant policy support provided in the United States―in the form of the passage of the Bipartisan Infrastructure Bill in November 2021 and the Inflation Reduction Act (IRA) in August 2022―could not reverse the sector’s underperformance, partly because it was clear that it would take a few years to deploy the funds provided by these programs.

A Few Headwinds Still Remain Especially in the United States

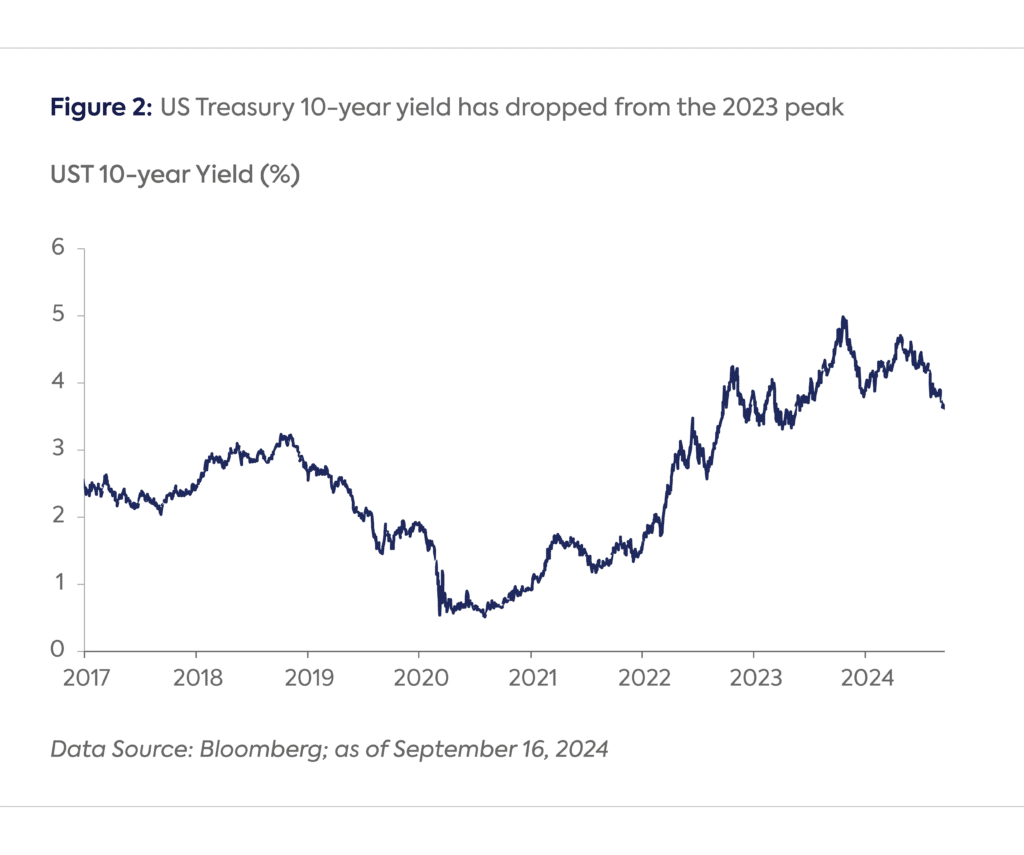

The interest rate cycle is now turning with the market expecting the Fed to lower rates by another 2 percentage points or so in a year, bringing the policy rate below 3 percent, according to Bloomberg. The yield curve is already reflecting much of this, with the 10-year late around 1.5 percentage points below its peak (Figure 2). The drop in long-end rates is important because of its relevance in discounting future cash flows as well as being the benchmark for the borrowing rate of a company, which is typically priced at a spread over the US Treasury yield of the bond’s tenor.

Although the low interest rate environment should be supportive of the renewable energy sector, several headwinds remain in the near term:

The upcoming US presidential election is a wildcard: The US presidential election remains a toss-up according to the latest polls.[5] With a large share of the benefits of the IRA flowing to Republican states, even under a Trump presidency, much of the bill is expected to remain intact.[6] Nevertheless, since the climate policies of the two candidates are a polar opposite, asset managers and asset owners are unlikely to take significant positions one way or another ahead of the election. As an example of election-related uncertainty, even a bipartisan proposal like the energy permitting reform legislation is unlikely to advance to the Senate floor until after the election.[7]

The risk of a recession remains: With inflation back within the target ranges, central banks are lowering interest rates to avert an economic slowdown. Despite these efforts, with the risk of a recession growing, investors are unlikely to seek out renewable energy companies with uncertain cashflows in an unpredictable policy environment.[8]

Ongoing antidumping investigations into solar panels along with the imposition of tariffs in the United States: The US Department of Commerce is in the process of investigating China’s dumping of crystalline silicon photovoltaic modules by routing it through other countries.[11] The pall of these antidumping and countervailing duties investigations is hanging over future investments in solar energy in the United States as are the steep tariffs on solar modules, which were hiked further this year.[12] With investments in wind energy continuing to shrink, especially in the United States, the deployment of solar energy is all the more important.[13]

Benefit of Lower Cost of Capital Should be Forthcoming

As interest rates drop, the resulting lower cost of capital should help accelerate these investments in 2025, assuming that some of the headwinds dissipate and the election outcome in the United States is climate-friendly.

The author is immensely grateful to Dr. Noah Kaufman for his valuable feedback on an earlier draft of the blog.

Foundations and Individual Donors Anonymous Anonymous the bedari collective Jay Bernstein Breakthrough Energy LLC Children’s Investment Fund Foundation (CIFF) Arjun Murti Ray Rothrock Kimberly and Scott Sheffield

Iran has among the world's largest natural gas resource bases, but its ability to supply regional and global markets is constrained by sanctions, underinvestment, and limited export infrastructure.

From the east to west and north to south, in red states and blue states, attention to data centers is skyrocketing in state capitals across the United States.

Two trade agreements recently negotiated by the Trump administration contain novel and coercive provisions with little precedent in US trade policy or the global trade system.

Plug-in electric vehicles (EVs) are reshaping the transportation energy landscape, providing a practical alternative to petroleum fuels for a growing number of applications. EV sales grew 55× in the past decade (2014–2024) and 6× since 2020, driven by technological progress enabled by policies to reduce transportation emissions as well as industrial plans motivated by strategic value of EVs for global competitiveness, jobs and geopolitics. In 2024, 22% of passenger cars sold globally were EVs and opportunities for EVs beyond on-road applications are growing, including solutions to electrify off-road vehicles, maritime and aviation. This Review updates and expands our 2020 assessment of the scientific literature and describes the current status and future projections of EV markets, charging infrastructures, vehicle–grid integration and supply chains in the USA. EV is the lowest-emission motorized on-road transportation option, with life-cycle emissions decreasing as electricity emissions continue to decrease. Charging infrastructure grew in line with EV adoption but providing ubiquitous reliable and convenient charging remains a challenge. EVs are reducing electricity costs in several US markets and coordinated EV charging can improve grid resilience and reduce electricity costs for all consumers. The current trajectory of technology improvement and industrial investments points to continued acceleration of EVs. Electric vehicles are increasingly adopted in the USA, with concurrent expansion of charging infrastructure and electricity demand. This Review details these trends and discusses their drivers and broader implications.

CGEP recently hosted a private roundtable conducted on a not-for-attribution basis that focused on key geopolitical issues and oil markets in various hotspots, including the Middle East, Russia/Ukraine, China, and the Americas.