This website uses cookies as well as similar tools and technologies to understand visitors’ experiences. By continuing to use this website, you consent to Columbia University’s usage of cookies and similar technologies, in accordance with the Columbia University Website Cookie Notice.

David Turk, who serves as a distinguished visiting fellow at the Center on Global Energy Policy at Columbia University SIPA, will testify at a full committee hearing of...

Announcement• April 8, 2025

Energy Explained

Get the latest as our experts share their insights on global energy policy.

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

In energy policy circles, the word “resilience” often refers to future-proof systems or infrastructure designed for the transition away from fossil fuels. But resilience means something different to...

Please join the Women in Energy initiative at the Center on Global Energy Policy at Columbia SIPA for a student roundtable lunch and discussion with Kadri Simson, who most recently...

Event

• Center on Global Energy Policy

1255 Amsterdam Ave

New York, NY 10027

About Us

We are the premier hub and policy institution for global energy thought leadership. Energy impacts every element of our lives, and our trusted fact-based research informs the decisions that affect all of us.

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. Rare cases of sponsored projects are clearly indicated.

For a full list of financial supporters of the Center on Global Energy Policy at Columbia University SIPA, please visit our website at Our Partners. See below a list of members that are currently in CGEP’s Visionary Circle. This list is updated periodically.

National oil and gas companies in the Gulf Arab States, aspiring to establish themselves as pioneers in low-carbon energy production, are strategically investing in technologies that can mitigate emissions from oil production, specifically carbon capture technology. For companies like Saudi Aramco, the Abu Dhabi National Oil Company (ADNOC), Petroleum Development Oman, and Kuwait Petroleum Corporation, all of which have declared net-zero targets for 2045–50, the significance of carbon capture technology lies in its capacity to facilitate alignment with the Paris Agreement’s overarching goal of holding global warming to well below 2°C and toward 1.5°C. The adoption of carbon capture may underscore their commitment to environmental sustainability, but also, perhaps more importantly, represents a proactive measure to mitigate risks associated with future carbon pricing mechanisms and regulatory frameworks. In a carbon taxed world—likely to increase use of tools like the European Union’s Carbon Border Adjustment Mechanism (CBAM) and direct carbon taxes on imported products—carbon capture is a means to extend the business cycle of hydrocarbon production by making cleaner and more marketable fossil fuel product.

Can the Gulf States have their cake and eat it too? The ability to capture emissions in fossil fuel production serves the purpose of meeting domestic net-zero targets while also protecting export revenues. In this article, the authors discuss the region’s competitive advantages and challenges in scaling carbon capture technology as a way to safeguard its future.

Adapting to a Lower-Carbon Future

The Gulf States are adapting to the realities of the energy transition, and the region is already a leader in carbon capture. According to the Global CCS Institute, about 10% of CO2 captured globally is in the industrial facilities of the Gulf States.[1] But the region is adapting in other ways as well, increasing the penetration of renewables in the domestic energy mix and attempting to diversify economies against the possibility of falling global hydrocarbon consumption.

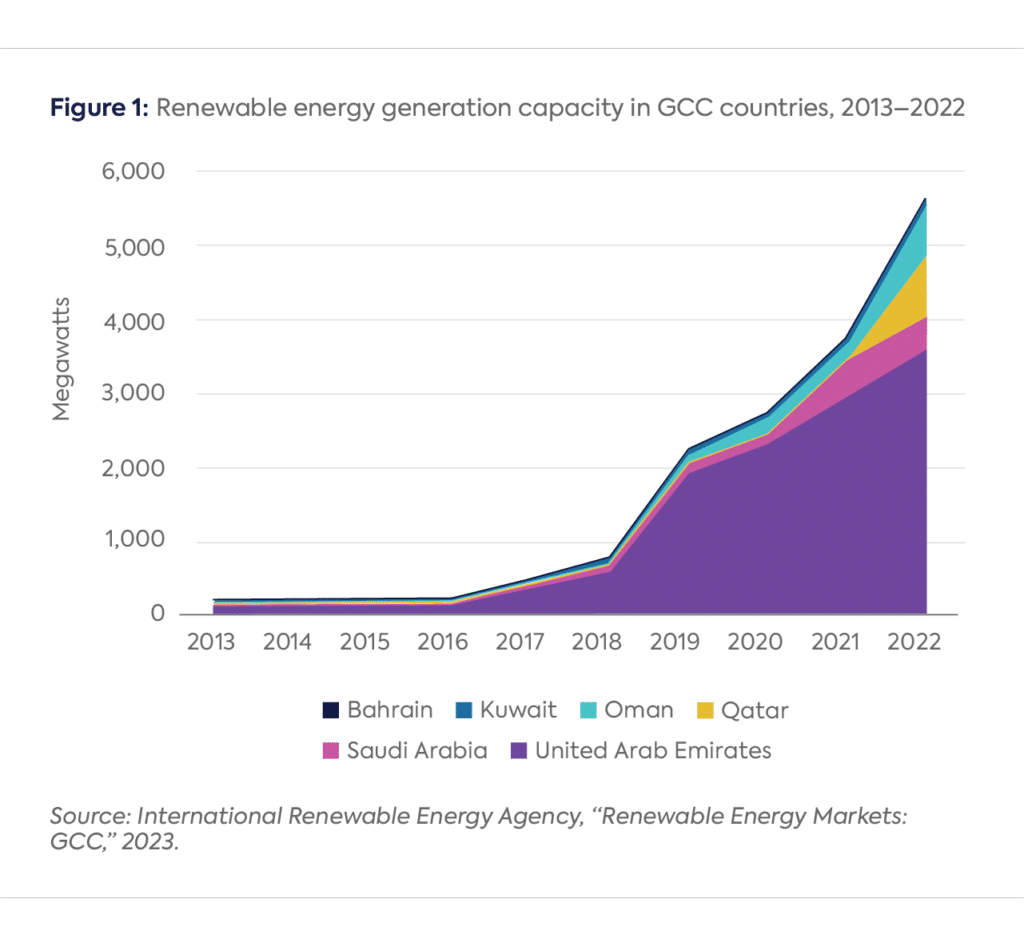

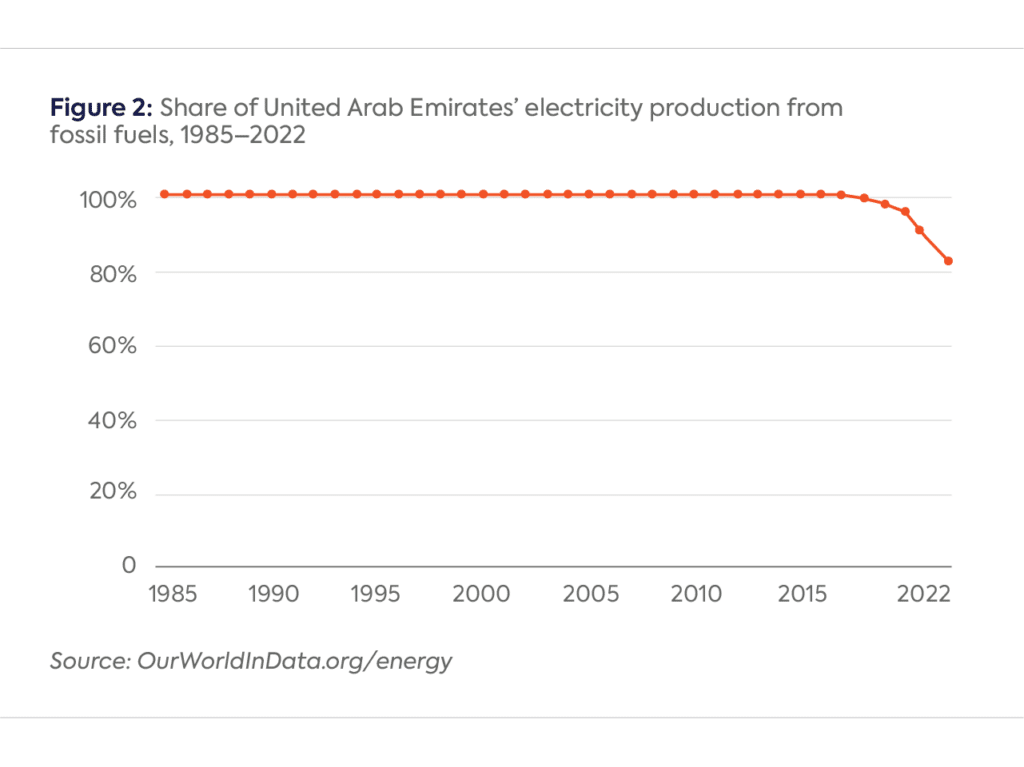

About 80% of CO2 emissions in Gulf States come from power, manufacturing, and fossil fuel operations. As power generation in the Gulf shifts toward solar, wind, and nuclear generation (Figure 1), emissions from electricity generation and heavy industry and manufacturing will decline gradually. For example, Saudi Arabia plans to shift its power mix from a near-total reliance on gas (61%) and oil (39%) in 2021 toward sourcing 50% of its power from renewables by 2030. In 2022, the kingdom had just 443 megawatts (MW) of renewable power generation capacity;[2] to compare, the total installed electricity generation capacity of the country’s primary source of electricity, the Saudi Electricity Company, was 83 gigawatts (GW) in 2021.[3] Similarly, the United Arab Emirates (UAE)—the Gulf state with the largest proportion of clean energy in its power mix—now generates only about 17% of its electricity from clean energy, including nuclear power (Figure 2). While progress on transitioning the power sector to lower its carbon emissions may seem slow, the region’s focus on changing the emissions profile of the hydrocarbon industry is ramping up quickly.

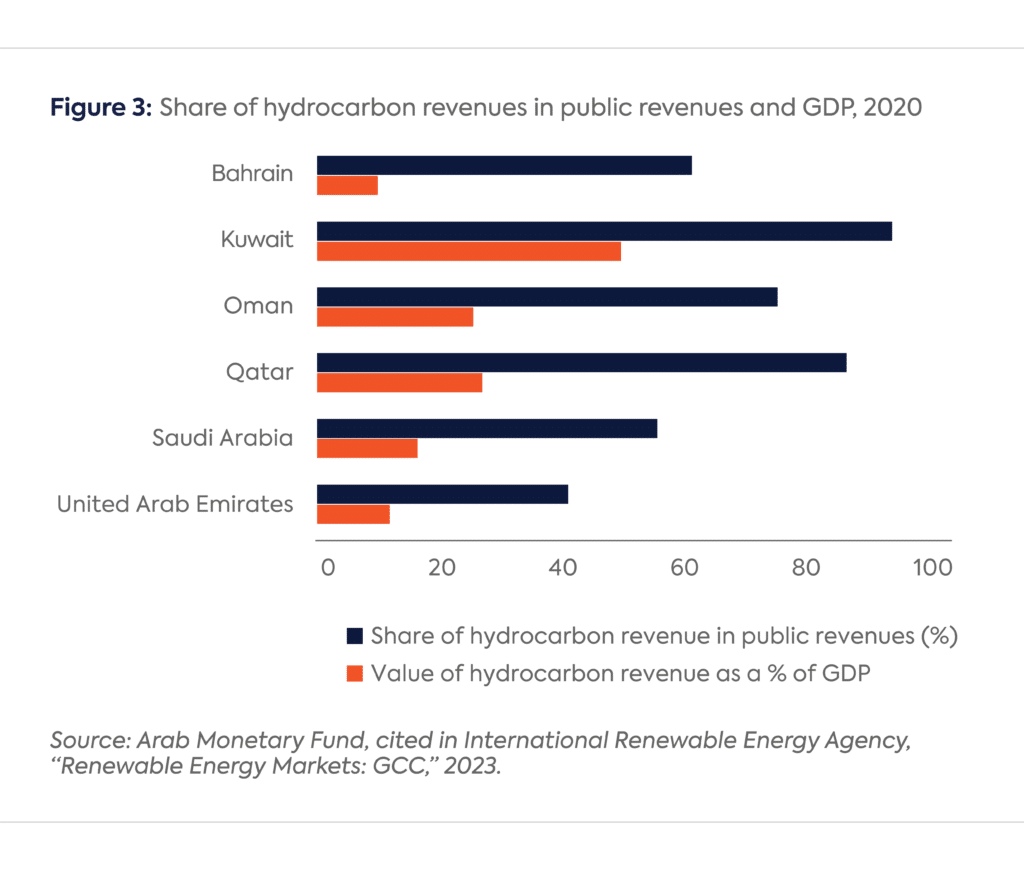

In addition, the share of hydrocarbon revenues as a proportion of total GDP is falling across the Gulf States as these economies diversify into business services, tourism, and logistics, among other sectors. However, except for the UAE, hydrocarbon revenues still account for more than half of government revenues of these countries (Figure 3). (Even in the UAE, oil revenues account for nearly 40% of federal government spending.)

Competitive Advantages in Carbon Capture Technology

According to Wood Mackenzie, about 20% of the emissions reduction needed to achieve global net zero by 2050 can be achieved by using carbon capture technology.[4] There are three main challenges to carbon capture implementation: high upfront capital costs,[5] competition for investment with renewable energy projects, and lack of clarity in regulatory environments in major consumer countries on carbon tax and border adjustment policies. Given these challenges, the Gulf States have several competitive advantages in the field of carbon capture technology.

First, their national oil companies boast some of the most cost-effective solutions for carbon capture and storage, ranging from $15 to $40 per metric ton, compared with costs in Europe that hover between $40 and $50 per metric ton.[6] Second, with their status as major global energy producers, Gulf States are positioned to harness economies of scale and maintain their current business models of oil and gas production. Third, the Gulf countries possess plenty of geological storage options, close to emissions clusters, with depleted gas reservoirs and saline aquifers offering an estimated storage capacity of 170 gigatons.[7] The Gulf States can further optimize these advantages—and some are already doing this—by building blue hydrogen facilities that mainly rely on carbon capture, storage, and utilization infrastructure. A study by the Oil and Gas Climate Initiative found the highest geological potential for storage in the Rub’ al Khali Basin, a sparsely populated large desert area across parts of Saudi Arabia, and in the basins of Kuwait.[8]

Carbon Capture Projects and Plans

The Gulf region’s unique strengths in cost efficiency, scale, and geological storage make it a pivotal player in advancing carbon capture technology on a global scale. In 2015, Saudi Aramco marked a historic moment in the Middle East by launching the region’s first large-scale carbon capture facility, boasting a capacity of 0.8 million metric tons per annum (mtpa).[9] ADNOC followed in 2016 by building a facility at Al Reyadah in Abu Dhabi that matches the capacity of its Saudi counterpart.[10] In 2019, Qatar unveiled a carbon capture facility at Ras Laffan LNG with a 2.1 mtpa capacity.[11] The region has 13 more projects in development that are expected to come online in the coming years,[12] including ADNOC’s new facility with a capacity of 1.5 mtpa—one of the largest announced in the Middle East so far—which triples ADNOC’s installed carbon capture capacity to 2.3 mtpa,[13] and a major carbon capture hub in Jubail, Saudi Arabia, which aims to capture and store 9 mtpa of emissions per year by 2027.[14]

In addition to these announced projects, carbon capture as a key technology to reduce emissions and achieve net-zero targets features prominently in the sustainability strategies of several national oil companies:

Saudi Arabia aims to increase its carbon capture capacity to 44 mtpa by 2035.[15]

UAE aims to boost its carbon capture capacity to 10 mtpa by 2030.[16]

QatarEnergy has set a goal to capture 9 mtpa of CO2 by 2035.[17]

Kuwait Petroleum Corporation and Petroleum Development Oman have announced ambitions to achieve net zero by 2050, with a significant portion attributed to the utilization of carbon capture and storage technologies.[18]

With the Oil & Gas Decarbonization Charter (OGDC), launched at COP28, countries have also agreed to invest in carbon capture technology as a tool to reach net-zero targets and accelerate climate action globally.[19] The OGDC covers about 50 oil and gas companies, accounting for about 40 percent of global oil production, including Saudi Aramco, ADNOC, and Petroleum Development Oman.[20] After COP28, ADNOC announced its acquisition of a 10% equity stake in Storegga, a UK-based company focused on carbon capture and storage.[21]

Risk of Uncertainty to Carbon Capture Investments

The Gulf States are testing the theory that their favorable geology for underground storage and proximity to gases from industrial production make them good candidates for large-scale adoption of carbon capture technology. But they face the challenge of scaling. The projects already up and running are much smaller than the projects in the pipeline. Take Saudi Aramco, which is gearing up for a huge blue hydrogen facility that would require more carbon capture. But here is the twist: Saudi Aramco has not sealed the deal on selling blue hydrogen yet. According to president and CEO Amin H. Nasser, the company will not invest in export infrastructure without offtake agreements.[22] This uncertainty reflects the bigger challenge of expanding in a still-undefined market.

For many, the sustainability of the oil and gas industry is incompatible with achieving larger climate goals. However, the Gulf region sees a role for cleaner fossil fuel and associated products, based on continued growth in demand for hydrocarbons alongside a shifting regulatory environment within those consumer markets. A strategy to change the emissions profile of products while earning revenues from them, along with the development of cleaner and lower-carbon energy options—such as blue hydrogen—is an attractive business model for national oil companies and governments.

Foundations and Individual Donors Anonymous Anonymous the bedari collective Jay Bernstein Breakthrough Energy LLC Children’s Investment Fund Foundation (CIFF) Arjun Murti Ray Rothrock Kimberly and Scott Sheffield

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

As Indian Prime Minister Narendra Modi makes his first visit to Washington in the second Trump administration, energy will likely take a front seat in United States-India relations. Due to...

During a speech at the World Economic Forum in Davos last month, President Donald Trump urged Saudi Arabia and OPEC to increase oil production to lower prices and exert...

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

The following document includes the responses submitted to the Department of Energy following the request for information on proposed national definition of a zero emissions building.

The power sector and transportation tend to dominate conversations about climate change, but there’s an under-the-radar source of climate pollution that must be addressed: industry.