This website uses cookies as well as similar tools and technologies to understand visitors’ experiences. By continuing to use this website, you consent to Columbia University’s usage of cookies and similar technologies, in accordance with the Columbia University Website Cookie Notice.

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

It’s hard to overstate how consequential President Trump’s “Liberation Day” tariffs have been for American economic policy. While the administration has paused the steep reciprocal tariffs it announced...

Please join the Center on Global Energy Policy at Columbia University SIPA for a rapid response briefing with Kadri Simson, CGEP Distinguished Visiting Fellow, Institute of Global Politics Carnegie Distinguished Fellow,...

Event

About Us

We are the premier hub and policy institution for global energy thought leadership. Energy impacts every element of our lives, and our trusted fact-based research informs the decisions that affect all of us.

India issued its first pair of sovereign green bonds in January, joining a growing list of countries to issue sovereign thematic bonds.[1] India has set ambitious decarbonization goals, including increasing nonfossil electricity capacity to 500 GW[2] and producing 5 million tons of green hydrogen by 2030.[3] The bond sale was followed by the release of the 2023–24 Annual Union Budget of India, which detailed budgetary allocations for several green initiatives using green bonds to finance infrastructure to decarbonize electricity generation, carbon-intensive industries, and railways.[4] This experience of issuing bonds for large-scale green projects holds lessons for India’s future decarbonization financing strategies and other emerging market and developing economies (EMDE) considering similar measures.

Greenium Achieved

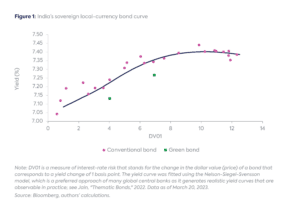

The debut green bonds were a success as they were issued with a premium and, just as importantly, in the local currency. The Ministry of Finance raised $1 billion between the two bonds, which increased to $2 billion following a second sale in February, and sold the bonds with an estimated premium of 5–6 basis points each.[5] The average premium for the two bonds in the secondary market is at 9 basis points as of March 20, 2023 (Figure 1), which is in line with the average premium observed across emerging market sovereign and quasi-sovereign green bonds.[6] The country thus managed to capture more than half of the premium in the primary market sale.

The denomination of the bonds in the Indian rupee is important because local currency issuance by EMDE makes up a minuscule of the green bond market (estimated at less than 3 percent of the global total).[7] Issuing in a local currency minimizes asset-liability currency mismatches, or countries holding liabilities in a foreign currency while generating investments and revenues in the local currency. Moreover, bonds issued in local currencies can help foster the growth of the domestic sustainability-focused fixed-income asset management industry, which can then support further issuances by the sovereign and other domestic corporations.

Laying the Groundwork

India’s sovereign green bond issuance was the culmination of a process that resulted in the release of a green bond framework in November 2022.[8]Establishing such a framework is key to ensuring transparency and integrity in a country’s green bond market.[9]

The framework is not legally binding, but it encourages investor confidence and reduces the risk of greenwashing. However, most countries see that creating such a framework adds time, money, and effort to issuing green bonds, leading to the temptation of simply selling conventional bonds, thereby missing out on important sources of green financing. The effort involved in creating a proper framework at the outset can be substantial, but later issuances can move more swiftly if they benefit from the properly laid groundwork. Green bond frameworks can support further issuance by assuring investors about transparent faithfulness to the International Capital Markets Association’s Green Bond Principles (GBP).[10]

India’s framework has notable features worth highlighting in each of the four core components of GBP:

Use of proceeds: The taxonomy explicitly excludes projects related to fossil fuels (except for the use of compressed natural gas in transport), nuclear energy, and large hydropower plants with a capacity greater than 25 megawatts.

Project evaluation and selection: The framework calls for the establishment of a Green Finance Working Committee. While almost all the frameworks released by different countries include such a committee, India’s is unique because, in addition to representatives from relevant ministries, it includes the central government’s independently run knowledge and policy development agency, the NITI Aayog. Additionally, all proceeds raised via a green bond are to be allocated within 24 months of issuance. Few countries have an explicit window for allocation, although Colombia’s allocation period of 12 months is even shorter.[11]

Management of proceeds: India’s framework calls for the maintenance of a “green register” of projects and for ministries to designate projects’ level of preparedness. The green register—if it is made public—should provide transparency by including details about the allocations of green bonds’ proceeds to eligible projects. Sharing the projects’ level of preparedness—which will range from 1–3 depending on if the project is ready for investment, under development, or in the conceptualization stage—would be a similar step toward transparency. The country has already used such an approach to develop a pipeline of infrastructure projects that could provide a template for a similar register of projects benefiting from the proceeds of the sovereign green bonds.[12]

Reporting: In addition to self-reporting by the government of India, the framework calls for annual third-party post-issuance external reviews, which is a recommendation but not a core component of the GBP. Although conducting these reviews adds to the cost of issuing green bonds, it assures investors that the bond proceeds are being used as intended and diminishes the risk of greenwashing.

For the green bond market to become a viable source of funding for India’s green ambitions, ESG-focused international investors will need to augment local investors. One approach for attracting external investors could be to lower or possibly eliminate withholding taxes on green bonds; in July, those tax rates for foreign investors are due to jump back to 20 percent from the current rate of 5 percent.[15] Lowering the tax rate on the coupon of green bonds has been shown to increase demand meaningfully.[16] An example in the domestic context is the tax-free bond issued by the Indian Renewable Energy Development Agency Limited in 2016, which was oversubscribed by more than five times.[17] A similar tactic could help attract foreign investors as well. The loss of tax revenue could potentially be made up indirectly by the perceived improvement in creditworthiness as a result of long-term investment in environmental sustainability.[18]

A second approach could be to address the issues that have bogged down the addition of Indian bonds into global debt indexes,[19] such as by making the bonds easy to settle and clear through international clearinghouses like Euroclear, providing clarity on taxation, and removing investment caps on foreign investors. Inclusion in bond indexes commonly used as benchmarks would likely attract international private capital.

Room to Grow

The issuance of India’s first sovereign green bonds is the beginning of what could be an important pillar of the country’s strategy for financing its decarbonization objectives. Various estimates put the investment required for India to achieve its clean energy targets at $160-200 billion per annum.[20]The $2 billion of the inaugural sovereign green bond is a small step in addressing this need, and as it corresponds to only around 1 percent of the government’s gross borrowing for the current fiscal year, there is ample room to increase the use of this strategy.[21]

Moreover, sovereign green bonds provide a local currency benchmark for domestic companies and agencies, and India’s national framework provides a template to follow for those entities. As a next step, developing a detailed green taxonomy could further support the decarbonization effort by helping companies and investors identify projects that meet sustainability criteria.[22]

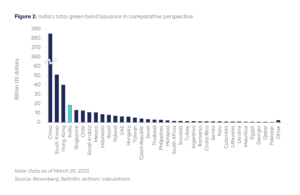

With a total of $19 billion of green bonds issued by March 20, 2023—only 13 percent of which were denominated in the rupee before the recent sovereign issuance—India currently stands fourth among EMDE and developed Asian countries (Figure 2). The sovereign issuance could help India catch up with some of its peer nations, especially if it increases the share of green bonds denominated in the local currency.

India’s detailed green bonds framework and effort toward transparency and efficiency bode well for the growth of this key source of financing for the country’s green growth strategy. With the issuance of India’s first municipal green bond last month, the national approach may already be inspiring subnational initiatives.[23] Indeed, India’s experience issuing green bonds may inform other emerging economies eager to finance climate-compliant infrastructure development.

The authors thank Mel Peh for her research assistance on this article.

President Donald Trump has made energy a clear focus for his second term in the White House. Having campaigned on an “America First” platform that highlighted domestic fossil-fuel growth, the reversal of climate policies and clean energy incentives advanced by the Biden administration, and substantial tariffs on key US trading partners, he declared an “energy emergency” on his first day in office.

The energy portion of India’s latest budget for 2024-2025 released last month provided some new announcements related to developing a national energy transition pathway

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

The Just Energy Transition Partnership (JETP) framework[1] was designed to help accelerate the energy transition in emerging market and developing economies (EMDEs) while embedding socioeconomic[2] considerations into its planning and implementation.

Commentary

by Gautam Jain & Ganis Bustami• March 03, 2025

This analysis provides an overview of changes in production and economic outcomes in US oil and gas regions, grouping them by recent trends and examining their impact on local economies.