Current Access Level “I” – ID Only: CUID holders, alumni, and approved guests only

Read more about the campus status level system and campus access information.

This website uses cookies as well as similar tools and technologies to understand visitors’ experiences. By continuing to use this website, you consent to Columbia University’s usage of cookies and similar technologies, in accordance with the Columbia University Website Cookie Notice.

As higher energy prices ratchet up projections for inflation, Becky Anderson speaks to Karen Young from The Center on Global Energy Policy at Columbia University about different inflation scenarios.

On March 20, Governor Kathy Hochul proposed significant changes to New York’s Climate Leadership and Community Protection Act (CLCPA), the landmark climate law passed in 2019.

Today marks the last day of CERAWeek, the annual energy industry conference sometimes described as the Davos of energy. As oil and gas CEOs and government officials gathered...

This roundtable is open only to currently enrolled Columbia University students. To register, you must sign in with your UNI. The Center on Global Energy Policy at Columbia...

Event

• Center on Global Energy Policy

1255 Amsterdam Ave, New York, NY 10027

About Us

We are the premier hub and policy institution for global energy thought leadership. Energy impacts every element of our lives, and our trusted fact-based research informs the decisions that affect all of us.

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. Rare cases of sponsored projects are clearly indicated.

For a full list of financial supporters of the Center on Global Energy Policy at Columbia University SIPA, please visit our website at Our Partners. See below a list of members that are currently in CGEP’s Visionary Circle. This list is updated periodically.

Amid plans to nearly double its steel production capacity by 2030 to serve its growing infrastructure needs, the world’s No. 2 steel producer India[1] has released plans to reduce greenhouse gases from the sector,[2] which account for about 10 percent of the nation’s total emissions.[3] This piece explores India’s steel sector and the challenges it may face to reduce emissions on par with other producing nations. These include India’s steel production’s heavy reliance on coal, the structure of its market, and the market’s technology mix. The piece also discusses India’s green steel plans within an international context where steel is the latest area of climate and trade competition between countries. India’s definitions of “green” or lower emissions steel may suit domestic needs. While carbon tariffs disproportionately increase costs for Indian steel exports, these exports are a fraction of total production. Likewise, India’s planned carbon emissions trading scheme may make a dent in steel emissions if designed stringently. Lastly, India’s green steel plans will leverage international partnerships.

India’s steel production is energy and emissions inefficient

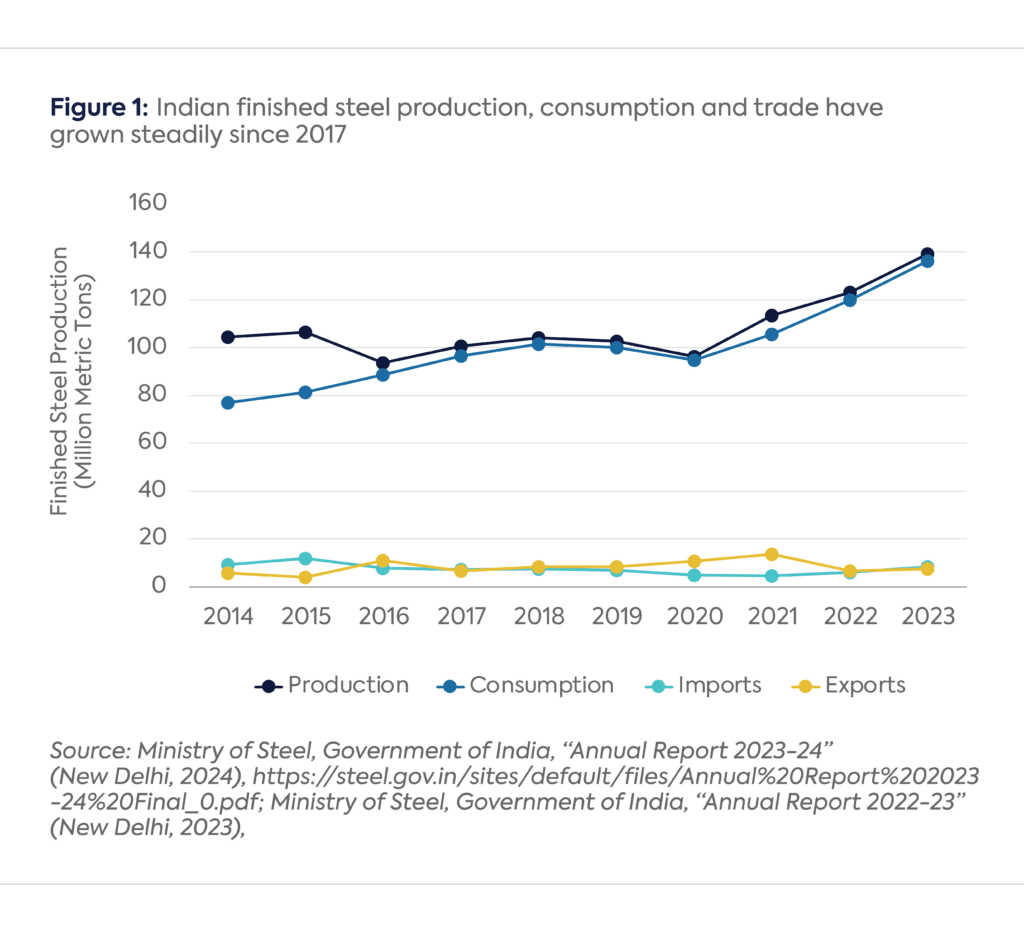

India’s steel production has grown since 2017, rising on average 6% per year, faster than global steel production and consumption.[4] The country consumes most of its own steel production (Figure 1).

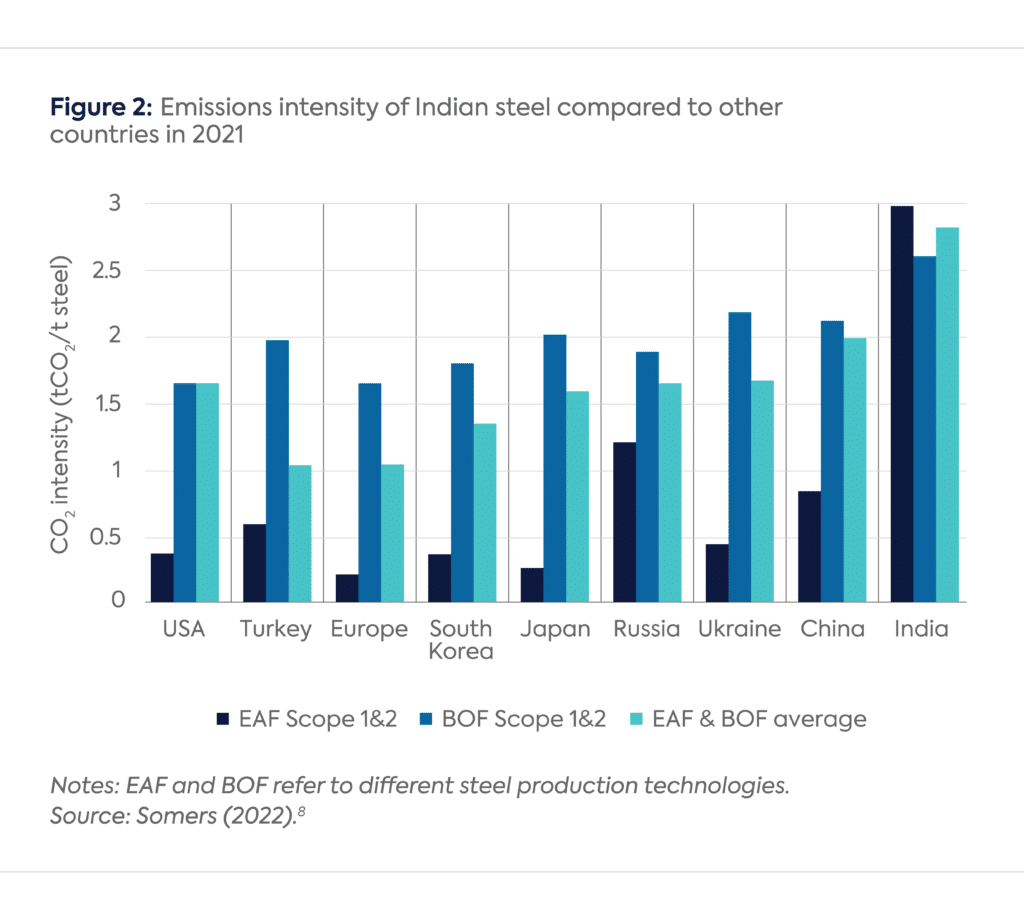

India is less efficient among major steel producing nations. Every ton of Indian steel uses more energy and emits more greenhouse gas emissions than steel produced in other major countries. (Figure 2). India ranks the third most energy intensive, using about a quarter more energy per ton produced than the global average.[6] Greenhouse emissions of Indian steel rank highest, about 30% more intensive than global averages.[7]

The energy and emissions of Indian steel are due to three factors: coal-dependence, market structure, and technology mix.[9]

While coal is a major input to make steel worldwide, India’s dependence on coal is especially large. Less than 10 percent of natural gas is used in steel processing, and a large share of the electricity used comes from coal.[10] This coupled with the lack of scrap material to produce recycled steel increases emissions and energy use.[11] In contrast, in the United States, natural gas directly fuels about a third of production or is a significant share of the electricity mix, and most production uses scrap steel.[12]

The Indian steel sector is also split into two producer segments that utilize different technologies for production. The first are a handful of integrated producers who can spend more capital on energy-saving technologies, expensive imported natural gas, or upskilling their workforces. Consequently, they can achieve economies of scale and produce larger amounts of steel from raw materials. These producers are mostly private companies with sizable international presences outside India (e.g. Tata Steel and JSW Steel), although a minority are state-owned enterprises.[13] The second are hundreds of medium and small enterprises who each have smaller production capacities. They vary in economic formality (i.e. registered and subject to government regulation), have less trained workers, and cater to regional steel demand. These producers depend on cheaper, inefficient technologies and domestic coal, increasing their emissions and energy use.[14]

Green steel in India will depend on implementation

The Ministry of Steel’s strategy to decarbonize Indian steel is ambitious and multipronged, the culmination of an 18-month process with stakeholders. In the short term, India will increase energy efficiency technologies, renewable energy, and steel recycling to reduce emissions from coal-based steel production. In the medium term, the strategy envisions increased hydrogen and carbon capture technologies. It also addresses bottlenecks such as defining “green steel,” adopting financing mechanisms for decarbonization, and workforce development.

The plan provides a policy signal and a strong evidence base to decarbonize Indian steel. However, actual budgetary allocations in the next Indian federal budget (out in February 2025) and government regulations will determine how effective the plan is. In addition, the list of proposed actions by the government are subject to political, economic, and bureaucratic constraints in the coming years.[15]

Putting India’s green steel plans in context

Indian “green” steel may be different than other countries. Most Indian steel is produced and consumed at home (Figure 1), meaning future Indian standards to define “green” steel are likely to suit domestic concerns. These standards may not be compatible in other regions with cleaner steel production like Europe or North America, a tradeoff the strategy recognizes.[16] If India takes a more relaxed definition of green compared to the EU, this might raise tension if the country seeks to gain credit for the European Union’s Carbon Border Adjustment Mechanism (CBAM) or Paris Agreement Article 6 carbon markets.

While the European Union’s CBAM increases the cost of Indian steel exports, these exports are a fraction of total Indian production. India’s objections to CBAM as unfair for developing countries has caught headlines.[17] While 10-20% of India’s steel production is exported (Figure 1), a quarter of Indian steel exports go to Europe and will disproportionately face costs from CBAM because of higher emissions.[18] Large integrated, multinational Indian companies are more likely to produce these higher-value exports.[19] They are better positioned than smaller independent producers to invest in steel decarbonization through technology, financing, and international markets.[20] CBAM may spur some decarbonization in the large Indian steel market through economic spillovers from these large, multinational companies (e.g. localization of supply chains for lower carbon steel). CBAM does hurt India’s steel export competitiveness, but unless those spillovers and exports increase, the carbon tariffs are only a limited lever to reduce emissions of the entire sector.

India’s planned compliance carbon trading market will address CBAM, but its impact on steel emissions is uncertain. India’s upcoming cap-and-trade carbon market will cover steel among other sectors, and is based on the country’s existing cap-and-trade mechanism for energy efficiency. This market only covers large producers, and the government plans to issue caps based on emissions intensity of steel produced with reductions of 13% by 2030. The lack of coverage by the carbon market for smaller producers along with historically lenient limits on energy efficiency mean emissions trajectories will depend on the stringency of the carbon compliance market. The strategy proposes emissions monitoring of smaller producers, opening the door for future inclusion into the compliance carbon trading market.[21]

India plans to leverage international partnerships. While the strategy spells out domestic action, the roadmap recognizes the need to attract international finance, technology, and partnerships.It is a clear articulation of “asks” on India’s part for further areas of bilateral and multilateral cooperation.

The author thanks Dr. Gautam Jain for his comments on an earlier draft of this piece.

Foundations and Individual Donors Anonymous Anonymous the bedari collective Jay Bernstein Breakthrough Energy LLC Children’s Investment Fund Foundation (CIFF) Arjun Murti Ray Rothrock Kimberly and Scott Sheffield

[7] Verma et al., “Greening the Steel Sector in India: Roadmap and Action Plan,” 40; J. Somers, “Technologies to Decarbonise the EU Steel Industry.” (Luxembourg: Publications Office of the European Union, 2022), 18, https://data.europa.eu/doi/10.2760/069150.

[8] Somers, “Technologies to Decarbonise the EU Steel Industry.”

[10] Alexandra Mallett and Prosanto Pal, “Green Transformation in the Iron and Steel Industry in India: Rethinking Patterns of Innovation,” Energy Strategy Reviews 44 (November 2022): 100968, https://doi.org/10.1016/j.esr.2022.100968.

On March 20, Governor Kathy Hochul proposed significant changes to New York’s Climate Leadership and Community Protection Act (CLCPA), the landmark climate law passed in 2019.

The United States is at a rare inflection point for nuclear energy, with unprecedented momentum behind deployment and regulatory reform as nuclear becomes central to energy security, AI competitiveness, and state and corporate climate goals.

The oil shock triggered by the crisis in the Persian Gulf has pushed crude above $100 per barrel, reviving familiar fears of economic turmoil in the United States driven by surging gasoline and diesel prices.