China Halts U.S. LNG Imports Amid Tariff War

China has ceased importing liquefied natural gas from the United States since early February, as the ongoing tariff war impacts energy trade.

Current Access Level “I” – ID Only: CUID holders, alumni, and approved guests only

Get the latest as our experts share their insights on global energy policy.

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

It’s hard to overstate how consequential President Trump’s “Liberation Day” tariffs have been for American economic policy. While the administration has paused the steep reciprocal tariffs it announced...

Find out more about our upcoming and past events.

Energy finance is transforming rapidly amid shifting political and economic dynamics in the U.S. and globally. As the landscape becomes increasingly complex, we will explore key legal insights,...

Insights from the Center on Global Energy Policy

The World Bank’s Middle East North Africa (MENA) regional economic update[1] released on April 6, 2023 (with a live webinar I was pleased to moderate[2]) is one that may herald a sharp divide, both within the region, with its uneven economic trajectory and obstacles to human capital development, and globally, as a cleavage between energy exporters and importers. The report signals that in the geopolitics of the energy transition there are important political dimensions and disaggregated trends to consider, affecting the macroeconomic stability of the countries that produce much of the global supply of oil and gas. Its findings focus on the detrimental long-term effects on human capital development of even temporary economic shocks of inflation and food insecurity.

Oil importers and exporters across MENA, including exporters in the wealthier Gulf Cooperation Council (GCC), will experience a slowdown in economic growth this year. But energy-abundant countries with hydrocarbon exports are not all alike. Those with restricted monetary policies, namely the Gulf states with currency pegs to the US dollar, have weathered the current inflationary environment more easily than most developing-economy oil exporters in the MENA region.

The World Bank estimates that following the MENA regional average acceleration from 2.3 percent real GDP per capita growth in 2021 to 4.4 percent in 2022, there is likely to be a sharp decline to 1.6 percent this year and just 1.7 percent growth in 2024 (Table 1). Even in the GCC, where per capita GDP grew 5.5 percent in 2022, that growth is expected to decelerate to 1.8 percent in 2023. For developing oil exporter Iraq, less than 1 percent per capita GDP growth is expected in 2023.

So even as oil prices remain buoyant, supported by OPEC+ production cuts[3] just in April, the wages of oil do not necessarily translate to automatic growth in the current global economic environment, even in the best-positioned oil exporting countries of the MENA region. Regular shocks in energy and food prices, whether driven by conflict (as in the case of Russia’s invasion of Ukraine) or by climate change, will be a persistent feature of the decades ahead.

The energy transition is expected to proceed with significant swings in hydrocarbon pricing, as demand for oil may be more persistent than investment and readiness of supply. Those swings can be inflationary and difficult to predict, especially when combined with geopolitical impacts on energy supply, such as the sanctions against Russian oil in the West and the price caps on its sale to the rest of the world. Energy and food pricing are closely linked, in the production of fertilizer, in transport, and often in the simultaneous geographical scarcity (or synergy, in the case of Russia) of both agricultural production and domestic energy production.

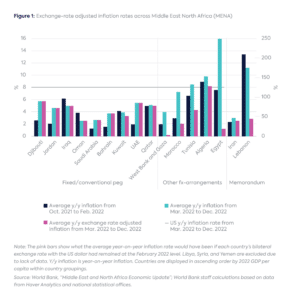

In the MENA region, several countries are significant importers of both food and fuel. In some, such as Egypt and Tunisia, this correlates with vulnerability to exchange rate volatility (Figure 1). Conflict states are especially vulnerable when their domestic food and energy production is damaged by war (Yemen) or by government dysfunction (Lebanon). And while global agricultural commodity prices as well as oil and gas prices have fallen from their mid-2022 highs, the aftereffects of low growth, high borrowing costs, and currency depreciation now combine to make headline—and especially food price—inflation persistent in much of the Middle East and North Africa.

Price shocks have long-term developmental consequences. Complex modeling in the MENA economic update[4] attempts to specify how food price inflation is detrimental to children’s learning and physical growth or stunting with intergenerational effects. In a region where children and young people are the dominant proportion of the population, the findings—particularly in a period of weakening post-pandemic economic recovery—are troubling. According to data from the OECD, young people (age 30 and under on average) were about 55 percent of the MENA population in 2022.[5] For comparison, on average, under-30 population in the OECD is about 35 percent of the total population.

The report estimates that as many as 200,000 to 285,000 newborns may have been at risk of stunting in the developing countries in the Middle East and North Africa due to rising food prices since the start of the war in Ukraine. About 8 million children in the MENA region are expected to be in food insecurity situations in 2023. But food insecurity in the Middle East has underlying causes that go beyond the war in Ukraine, including the current lower growth and higher borrowing costs that are putting additional pressure on government spending and fiscal priorities.

There are important differences between oil importers and exporters in the MENA region in terms of access to capital and abilities to balance demands of both monetary and fiscal policy. There is a relationship between inflation and debt, at least in terms of the ability to manage debt service priced in foreign currency, usually US dollars.

As the World Bank describes:

Depreciations vis-à-vis the US dollar that led to higher levels of inflation occurred mainly in oil-importing countries such as Egypt, Morocco, and Tunisia. Their current accounts were hit by increases in the prices of food products and oil, most of which are imported. In these economies, this hit coincided with high levels of debt and worsening global financial conditions…One possibility is that countries with higher levels of debt find it more difficult to destine resources to lean against currency pressures, which would increase the likelihood of experiencing larger depreciations and inflating prices of imported goods in domestic currency. (World Bank 2023: 11)

There are certainly points of intervention[6] for governments, international financial institutions, and aid organizations to consider, including cash transfers and support for maternal nutrition and care to counteract the risk of food insecurity for children. And it’s best to be cautious about deterministic readings of youth potential based on nutrition and in-utero effects alone; there are clearly many opportunities, as well as structural and environmental barriers to human capital across the region and globally. No one is destined to fail. But the current macroeconomic environment in MENA, combined with expected volatility in both energy and food prices due to energy transition and climate change, means that a generation of families with children will have to deal with these ups and downs in their household economic planning.

States in the region with more difficult inflationary and currency pressures will face debt management challenges and are likely to seek financial assistance,[7] in aid and investment, from the Gulf. My book The Economic Statecraft of the Gulf Arab States[8] explores this inter-regional dynamic in detail.

The experience of the Middle East and North Africa region illustrates the connections between food and energy security, and intra-regional variation in vulnerability to external shocks. The economic outlook for the MENA region depends on a number of external factors, including future oil and gas markets, climate change and environmental shocks, and the intra-regional politics of aid and investment, combined with access to finance and intervention from international financial institutions. Opportunities for protecting human capital development, through enabling food security and access to good nutrition, is just one piece of a set of development policy challenges.

[1] https://www.worldbank.org/en/region/mena/publication/middle-east-and-north-africa-economic-update.

[2] https://live.worldbank.org/events/altered-destinies-middle-east-north-africa-economic-update.

[3] https://foreignpolicy.com/2023/04/06/saudi-opec-oil-production-cut-price-geopolitics-biden-china/.

[4] https://www.worldbank.org/en/region/mena/publication/middle-east-and-north-africa-economic-update.

[5] https://www.oecd-ilibrary.org/sites/3ced02bf-en/index.html?itemId=/content/component/3ced02bf-en.

[6] https://www.worldbank.org/en/region/mena/publication/middle-east-and-north-africa-economic-update.

[7] https://www.wsj.com/articles/saudi-arabia-gulf-countries-want-better-returns-for-bailing-out-egypt-e6e8b047.

[8] https://www.bloomsbury.com/us/economic-statecraft-of-the-gulf-arab-states-9780755646661/.

President Donald Trump has made energy a clear focus for his second term in the White House. Having campaigned on an “America First” platform that highlighted domestic fossil-fuel growth, the reversal of climate policies and clean energy incentives advanced by the Biden administration, and substantial tariffs on key US trading partners, he declared an “energy emergency” on his first day in office.

November’s election for president of the United States will have crucial implications for the nation’s and world’s energy and climate policies.

The energy portion of India’s latest budget for 2024-2025 released last month provided some new announcements related to developing a national energy transition pathway

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

The Just Energy Transition Partnership (JETP) framework[1] was designed to help accelerate the energy transition in emerging market and developing economies (EMDEs) while embedding socioeconomic[2] considerations into its planning and implementation.

This analysis provides an overview of changes in production and economic outcomes in US oil and gas regions, grouping them by recent trends and examining their impact on local economies.