This website uses cookies as well as similar tools and technologies to understand visitors’ experiences. By continuing to use this website, you consent to Columbia University’s usage of cookies and similar technologies, in accordance with the Columbia University Website Cookie Notice.

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

It’s hard to overstate how consequential President Trump’s “Liberation Day” tariffs have been for American economic policy. While the administration has paused the steep reciprocal tariffs it announced...

Please join the Women in Energy initiative at the Center on Global Energy Policy at Columbia SIPA for a student roundtable lunch and discussion with Sunaina Ocalan, who will discuss...

Event

• Center on Global Energy Policy

1255 Amsterdam Ave

New York, NY 10027

About Us

We are the premier hub and policy institution for global energy thought leadership. Energy impacts every element of our lives, and our trusted fact-based research informs the decisions that affect all of us.

This commentary represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. More information is available at Our Partners. Rare cases of sponsored projects are clearly indicated.

The United States, one of the world’s two largest greenhouse gas emitters, will require reliable critical mineral[i] supply for technologies associated with the energy transition, such as batteries for electric vehicles and to support reliability of the grid, if it is to meet its 2050 net-zero goals. Currently, its energy transition is flush with geopolitical challenges, specifically with respect to China, which dominates global critical mineral supply chains. To lessen dependence on China, the United States can produce more critical minerals domestically and, to a greater degree,diversify its foreign supply chains.

Efforts to diversify supply will not always be easy. Mineral-rich countries want to move away from an extractivist-export model and capture more economic development opportunities linked to their mineral richness through material processing and taking ownership of larger parts of the supply chain. For some supplier countries, this greater degree of control may not impede supply; for others, it could threaten investment in the extractives sector. Several Latin American countries have a history of pendulum swings between privatization/liberalization and resource nationalization, which can make it more challenging to discuss new partnerships with the US. Such partnerships have been criticized by leftist political actors[ii] as granting too much power to international companies, allowing them to extract and export under the guise of economic efficiency without significantly contributing to local development.

While all of these challenges are real, the energy transition holds geopolitical opportunities as well. One of them is for Latin America to become an equal partner with the United States and the West in efforts to avoid catastrophic climate change. In this commentary, the authors evaluate the potential of Brazil in particular under this dynamic. The authors discuss Brazil as a potential US trade partner in critical minerals by considering the country’s 1. reserves and production, 2. environmental landscape linked to mining, 3. evolving policy framework, and 4. market and investment ecosystem. The commentary synthesizes what the Brazilian government has done so far and where improvement is still needed. It finds that there is increasing investment from foreign companies to develop critical mineral mining in Brazil, especially from China. A potential critical minerals agreement (CMA) between the US and Brazil could support the US’s critical mineral needs while countering Chinese influence. To make such an agreement feasible, the Brazilian government and mining companies would need to address environmental concerns and the Brazilian government would need to improve the licensing approval process to streamline production.

Reserves and Production

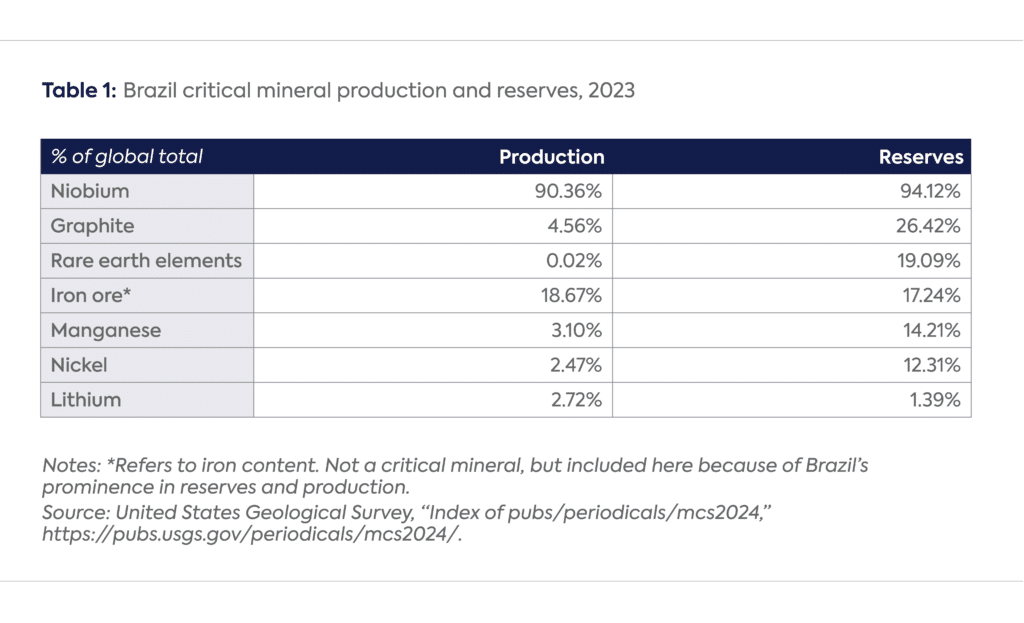

Brazil’s mineral richness aligns well with US needs. It holds about one-quarter of global reserves in graphite, and just under 15% of global reserves in nickel and manganese,[iii] though its production levels currently do not reflect its reserves (see Table 1). That said, Brazil’s critical mineral industry is growing, reaching a trade surplus of $27.9 billion in 2022.[iv] It is among the five largest mineral producers in the world and has the world’s largest share of niobium.[v]

Currently, China dominates the production and supply of many of these critical minerals. It has a 76.8% share of the world’s production of natural graphite[vi] and more than 90% of refined spherical graphite, primarily used in batteries.[vii] For rare earth elements, China produces 70% of worldwide supply.[viii] China does not produce a lot of nickel in-country, but it dominates global supply chains through its operations in the world’s largest producer, Indonesia, where China’s high-pressure acid leach method has become a key source of high-grade nickel for the battery industry. China also processes about 70% of nickel sulphate. For manganese, although China does not have a lot of domestic production it handles more than 90% of the mineral’s processing into the high-purity form that can be used in batteries.[ix]

Given its large reserves in many of these metals, Brazil could be a viable partner to the US in achieving the latter’s critical mineral diversification plans. Brazil is rapidly investing in the expansion of all of its mining activities, with more than 9,000[x] active mining projects underway and a private investment forecast in the mining sector of $64.5 billion between 2024 and 2028.[xi] This level of investment represents a high in the past decade, with a special focus on logistics, environmental standards, and critical mineral development. Brazil seeks to provide the necessary minerals to battery manufacturers “wherever they are located” and to strengthen its integrated supply chain not only in-country but also with other South American partners.[xii] Most of the private investment indicated will be foreign, and where this money comes from will simultaneously impact the global energy transition and geopolitics.

Environmental Challenges

Thirty percent of Brazilian critical minerals are located in the Amazon region.[xiii] This implies a need for deeper discussion on whether it is possible to simultaneously preserve the Amazon region and develop the region’s mineral resources necessary for the energy transition.[xiv] Successful environmental stewardship, such as by managing risks related to biodiversity loss and deforestation, can enable a deeper global debate on the implications of sustainable mining, mineral rights,[xv] and the responsible exploration of the resources available. Expanding mining in sensitive regions, such as the Amazon rainforest, will require high-levels of managerial scrutiny and consultation to ensure that environmental harm is contained as much as possible. Brazil has been expanding its geological mapping (currently covering about 27% of the country) to ensure resources are mined in a strategic, efficient, and sustainable manner by: prioritizing strategic mining areas; finding communities interested in engaging in mining activities; and improving the identification of mineral deposits, reducing the need for extensive exploratory drilling.[xvi] It is also building an environmental, social, and governance (ESG) taxonomy for the mining and mineral processing sector according to best national and international practices, which will guide investment criteria and indicators on how activities relate to sustainable practices and to a sustainable economy.[xvii]

As momentum for expanding mineral mining in Brazil builds, the potential for environmental harm cannot be ignored. Currently, 122 tailing dams in Brazil are flagged by the government as “concerning,” 97 of which involve structural concerns.[xviii] Tailing dams store byproduct waste and water from mineral extraction, which are often toxic. The collapse of the tailing dam in Brumadinho in 2019 led to 270 deaths and severe environmental impacts[xix] described as the greatest in Brazilian history and the largest for tailing dams in the world.[xx] Securing Brazil as a critical mineral partner requires supporting the reinforcement of responsible mining practices and higher environmental and safety standards, especially given the heightened attention mineral consumers and investors are giving to ESG performance.

Evolving Policy Landscape

Brazil is developing a regulatory structure to support critical mineral mining, but bottlenecks created by a long licensing period for mining involving multiple governmental levels exist.[xxi] And while the country generally treats local and foreign investors equally under its laws,[xxii] activities within Brazilian border zones, for example, require a majority Brazilian ownership and workforce.[xxiii]

Indicative of its awareness of the potential to become a key critical minerals player, the Brazilian government has attempted to attract foreign investment by offering benefits such as tax exemptions for exports,[xxiv] reduced costs of financing, and reduced income tax rates.[xxv] However, mining taxes remain high[xxvi] and the overall tax environment remains complex and spread across jurisdiction levels, despite ongoing reforms aimed at enhancing transparency and regulatory certainty.[xxvii]

The government is also creating a number of initiatives to support the development of a national mining industry that is attractive to foreign investors. It is devising a new strategic national plan for critical minerals[xxviii] that, among other things, aims to restructure the National Mining Agency and unclog an estimated 70,000 mining licenses awaiting approval.[xxix] Finding the balance between facilitating license approvals and engaging with stakeholders on environmental and Indigenous rights is paramount.[xxx]

The country’s national geology department established an exclusive division on critical minerals, which has streamlined approval for strategic projects, specifically in lithium and rare earth elements.[xxxi] It has engaged in marketing campaigns and international forums to promote Brazil’s mineral wealth,[xxxii] such as announcing the Guide for Foreign Investors in Critical Minerals for the Energy Transition in Brazil and hosting a Brazilian Mining Day[xxxiii] at international conferences (such as the Prospect and Developers Association of Canada in 2024[xxxiv]). The country is participating in global dialogues on critical minerals, including joining the UN Panel on Critical Energy Transition Minerals,[xxxv] which promotes equitable standards and practices in the sector.[xxxvi]

The Brazilian government has also recently released its industrial policy, “Brazil New Industry,” which directs about $60 billion (R$300 billion) to modernize the country’s industrial sector,[xxxvii] focused on increasing autonomy and further developing clean energy sources.[xxxviii] Its Growth Acceleration Plan directs about $61 million (R$307 million) to mining-related R&D[xxxix] (which has doubled since 2020[xl]), and its Green Mobility and Innovation[xli] program offers over $3.8 billion (R$19 billion) in tax incentives for companies wishing to invest in the electric vehicle (EV) supply chain in Brazil.[xlii] Through these initiatives, the Brazilian National Development Bank (BNDES) seeks to obtain company shares to de-risk investments in strategic sectors, such as critical minerals, batteries, and EVs. The bank has about $1.6 billion (R$8 billion) in its budget for acquisitions.[xliii]

In February 2024, Brazil announced the creation of a new investment fund in partnership with BNDES and the Ministry of Mines and Energy totaling $200 million (R$1 billion) to attract investments in mineral exploration projects that support the energy transition and fertilizer supply chains.[xliv] The fund aims to increase local production of the materials required for EV batteries[xlv] and promote ESG practices in the invested companies.

Market and Investment Framework

Brazil’s energy resource mix, at about 45% renewable,[xlvi] is increasingly attractive to international investors interested in decarbonizing their supply chains, including mining interests.[xlvii]

Rare earth minerals investments have been gaining traction with international players. In August 2023, Meteoric Resources NL, a mineral exploration company headquartered in Australia, signed a protocol of intention to invest over $200 million (R$1 billion), with an additional $250 million in preliminary support from the US Export-Import Bank,[xlviii] in one of the world’s largest rare earths projects.[xlix] In February 2024, Viridis Mining and Metals of Australia signed a protocol of intent to invest $272 million (R$1.35 billion) in another rare earths project in the same Brazilian state of Minas Gerais,[l] which claims record recovery rates.[li] Meanwhile, Brazil Rare Earths mining company raised about $33 million (A$50 million) on the Australian Securities Exchange in December 2023[lii] to support exploration of a large-scale rare earths project in the state of Bahia.[liii]

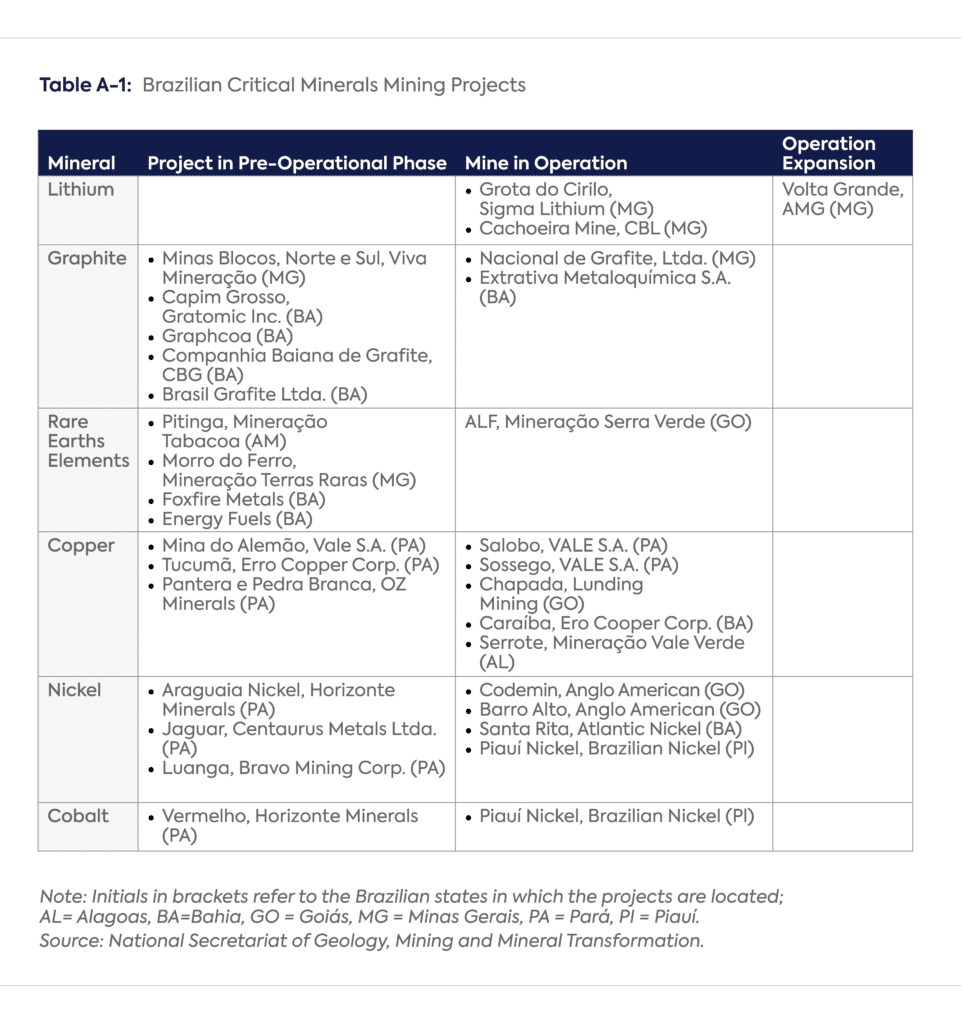

Brazil is advancing at least six rare earths projects,[liv] each requiring adequate processing equipment. The US is seen by the local market as the most reliable partner for such equipment, opening trade opportunities for the US.[lv]

Investments in lithium in Brazil have also grown in popularity with international investors, with four mining companies (Sigma Lithium,[lvi] Atlas Lithium,[lvii] Lithium Ionic,[lviii] and Latin Resources[lix]) announcing lithium exploration projects. The country’s cost competitiveness leads some experts to believe mining it in Brazil remains profitable,[lx] despite a 70–80%[lxi] decrease in prices from 2023 to 2024. Atlas Lithium advisor and ex-CFO of Sigma Lithium, Rodrigo Menck, estimates Brazilian lithium costs to be one-third or less of the production costs in Australia, including labor, raw materials, and transportation.[lxii] Lithium projects in the region also have received a “green” seal for their environmental standards, due to the lack of tailing dams and the country’s clean energy mix.[lxiii]

However, expanding the lithium value chain in Brazil could be costly, with several experts suggesting that investment needs for lithium processing plants are high.[lxiv] This could influence the government’s plan to refine minerals locally and further extract value.[lxv] That said, AMG Brazil, a private company specializing in critical minerals, special materials, and energy,[lxvi] is considering building a lithium carbonate conversion plant projected to cost $250 million and produce 15,000 tons annually.[lxvii]

In addition, Sigma Lithium, a Canada-based lithium producer, announced a 27% increase in its audited mineral resource estimates[lxviii] for Grota do Cirilo,[lxix] making the Brazilian mine the world’s fourth largest pre-chemistry lithium operation.[lxx] BYD, Volkswagen, and CATL, companies that heavily depend on lithium products for their supply chain, have shown interest in acquiring the company. A government-launched initiative called “Lithium Valley,” which was celebrated by ringing the Nasdaq[lxxi] opening bell in May 2023, aims to attract foreign investments for exploring 45 high-purity lithium deposits in the region and expanding the lithium supply chain in the country.[lxxii]

China is currently the largest purchaser of Brazilian minerals, buying about $23 billion in 2023, mostly of iron ore ($20 billion).[lxxiii] BYD, a privately owned company headquartered in China, announced locating its largest industrial hub outside China in Brazil, with an investment of over $1 billion (R$5.5 billion) and expected production of vehicles by the end of 2024.[lxxiv] Chengxin Lithium Group and Yahua Industrial Group, two Chinese chemical lithium companies that provide lithium hydroxide to Tesla, BYD, and LG, announced $50 million for Atlas Lithium, a US mineral exploration company with mineral properties in Brazil, to fund a Brazilian lithium development project.[lxxv]

US-Brazil Trade Opportunities

The US is the main destination for Brazilian exports of value-added manufactured goods, and was the largest source of foreign direct investment in Brazil in 2023, totaling $207.86 billion.[lxxvi] The US is Brazil’s second-largest mineral export partner, with trade amounting to $13 billion in 2023, while China remains the largest at $23 billion.[lxxvii]

A critical minerals agreement (CMA) between Brazil and the US could make Brazilian exports compliant with the Inflation Reduction Act (IRA), provided the company is not more than 25% Chinese-owned. This could support direct US investment into Brazilian projects instead of in international companies operating in the region by reducing trade barriers, enhancing the security of supply chains, and promoting joint ventures that align with both nations’ strategic interests and regulatory frameworks.

A CMA could be IRA-compliant depending how negotiations are conducted. The US-Japan CMA made Japanese exports IRA-compliant as long as they don’t involve foreign entities of concern.[lxxviii] Given Brazil’s wide range of mineral supply, a similar approach could be of interest to the US. Likewise, Brazil could benefit from such an agreement by ensuring buyer diversification, which could further attract investment into the country.

But the effectiveness of a CMA would hinge on Brazil’s willingness and ability to enhance its regulatory framework. The often slow process of obtaining permits and licenses dissuades some potential investors from participating in the market.[lxxix] Challenges related to infrastructure, including insufficient transportation networks and a shortage of energy supply, add further layers of complexity. Existing regulations also fail to account for recent industry advancements, including environmental considerations; though, as previously mentioned, the government is working on that.[lxxx]

Despite these challenges, the US has signaled interest in having preferential access to Brazilian production of minerals.[lxxxi] The Joint Statement on the Brazil Fazenda–US Treasury Climate Partnership, announced on July 26, 2024, indicates renewed recognition of the two countries’ potential in cooperating on clean energy supply chains, of which critical minerals can play an integral part.[lxxxii] A CMA could enhance the two countries’ cooperation in diplomacy, security, and technology, aligning with the US’s strategy to reduce reliance on China. For the same purpose of diversifying their critical mineral supply chains, France,[lxxxiii] Germany,[lxxxiv] and Italy[lxxxv] have secured bilateral agreements with Brazil.

The US and Brazil have already established a bilateral Critical Minerals Working Group, which supports bilateral cooperation, supply chain diversification, and security in critical minerals essential to the energy transition.[lxxxvi] Since its launch, however, little action has been taken. Post-IRA demand for nickel in the US has risen 14%,[lxxxvii] but US companies and the US government are currently purchasing cheap, high-quality nickel from Indonesia, which is extracted and processed with significant Chinese ownership and an environmental footprint. As the world’s eighth largest producer of nickel,[lxxxviii] Brazil could become a strategic partner to the US and help it meet its forecasted demand in a way that also aligns with the US’s diversification of supply and lower-carbon goals.

The Brazil-US collaboration could also be fortified if Brazil formally joined the US-led Minerals Security Partnership (MSP), an idea welcomed by Secretary of State Antony Blinken during a meeting with Brazilian President Luiz Inácio Lula da Silva in February 2024.[lxxxix] Brazil already participates in MSP discussions, which underscores its commitment to developing sustainable supply chains that support economic development goals.[xc] Its involvement in the March 2024 meeting included discussing project developments, expansion of critical mineral supply chains, and upstream and downstream processing.[xci]

Previous agreements between Brazil and the US, such as the Clean Energy Industry Dialogue[xcii] and the Agreement on Trade and Economic Cooperation,[xciii] have strengthened the partnership between the countries by enhancing trade efficiency, reducing tariffs, and boosting transparency and government standards.[xciv] This has paved the way for a more streamlined and cooperative business environment that could be furthered by establishing a CMA to ease trade relations and foster mutual investment opportunities.

Addendum

Notes

[i] The US Department of Energy characterizes the following as critical minerals: aluminum, antimony, arsenic, barite, beryllium, bismuth, cerium, cesium, chromium, cobalt, dysprosium, erbium, europium, fluorspar, gadolinium, gallium, germanium, graphite, hafnium, holmium, indium, iridium, lanthanum, lithium, lutetium, magnesium, manganese, neodymium, nickel, niobium, palladium, platinum, praseodymium, rhodium, rubidium, ruthenium, samarium, scandium, tantalum, tellurium, terbium, thulium, tin, titanium, tungsten, vanadium, ytterbium, yttrium, zinc, and zirconium. See, Critical Minerals & Materials Program, US Department of Energy, “What Are Critical Materials and Critical Minerals?” https://www.energy.gov/cmm/what-are-critical-materials-and-critical-minerals.

[xiv] The matter of concomitantly preserving the Amazon rainforest and sustainably mining its mineral resources is not addressed in the scope of this piece.

[xix] F. Zhu, W. Zhang, and A.M. Puzrin, “The Slip Surface Mechanism of Delayed Failure of the Brumadinho Tailings Dam in 2019,” Communications Earth & Environment 5 (2024): 33, https://doi.org/10.1038/s43247-023-01086-9.

[xx] C.d.S Vergilio et al., “Metal Concentrations and Biological Effects from One of the Largest Mining Disasters in the World (Brumadinho, Minas Gerais, Brazil),” Scientific Reports 10 (2020): 5936, https://doi.org/10.1038/s41598-020-62700-w.

[lxviii] Note: audited mineral resources refer to independently verified assessments of the quantity and quality of minerals, ensuring accuracy, reliability, and compliance with industry standards. See more at: Mark Campodonic, “External Mineral Resource Audits,” SRK News Issue #51: Mineral Resource Estimation, https://www.srk.com/en/publications/external-mineral-resource-audits.

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece...