Trump is frustrated gasoline prices don’t mirror oil’s decline. Experts say it’s not that simple

U.S. gasoline prices decreased an average of 49 cents a gallon in the last month as expectations rose for an end to the war with Iran.

Get the latest as our experts share their insights on global energy policy.

This Energy Explained post represents the research and views of the author(s). It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

The energy transition is in the midst of its own transition. Spiking electricity demand and geopolitical events are driving up energy prices, while debates over the best sources...

Commentary by Kaushik Deb & Abhiram Rajendran • August 01, 2023

This commentary represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. More information is available at Our Partners. Rare cases of sponsored projects are clearly indicated.

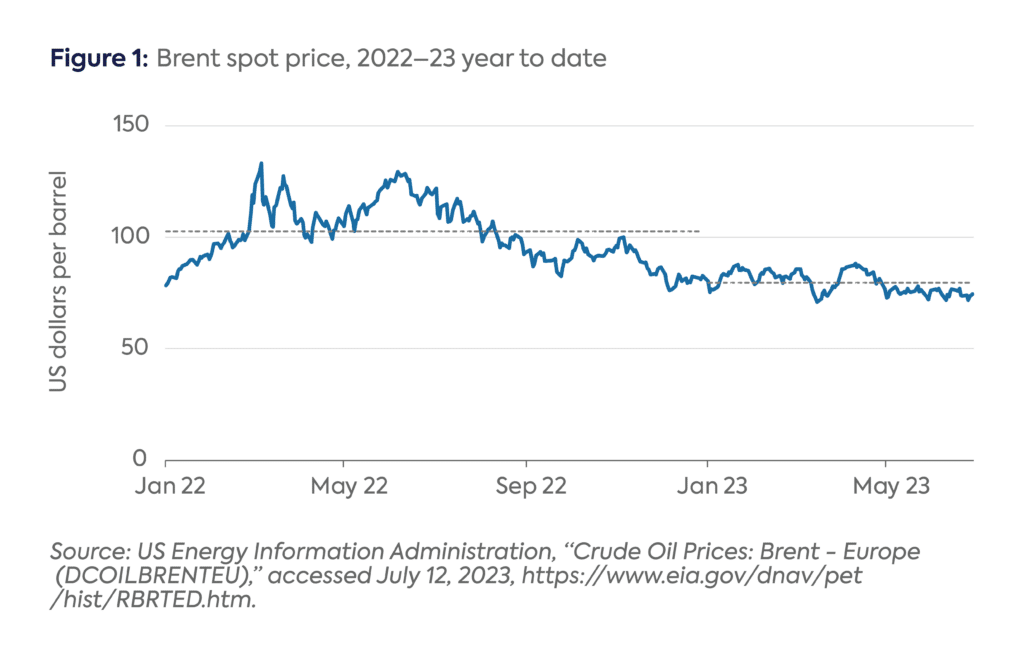

Global crude oil prices have remained muted for much of 2023. The average Brent crude oil price benchmark during the first half of the year was less than $80 per barrel (b) (Figure 1), a 26 percent decrease year over year and 23 percent below the average across 2022. The average external breakeven price[1] for the Organization of the Petroleum Exporting Countries (OPEC) and 10 other oil exporters,[2] collectively known as OPEC+, is estimated at $77/b, and the Brent price remained under this level for a total of 53 days within the first six months of 2023, impacting the ability of these countries to pay for their imports. More significantly for strictly OPEC members, the fiscal breakeven price, or the oil price at which the fiscal balance is zero, is estimated at $98/b,[3] and the Brent price has remained below that level since November 2022. This lackluster oil price environment is due to numerous macroeconomic headwinds which have weighed on oil demand growth.[4] Most significantly, China’s economic recovery turned out to be weaker than expected and remains fragile. That combined with overall economic stagnation in Europe and the United States has been a drag on oil market sentiment even as consumption has improved over the first half of 2023.

In response, OPEC+, has attempted to continue to cut production targets. Earlier this month, OPEC+ leaders Saudi Arabia and Russia announced further voluntary production and export cuts, with the former alone accounting for nearly half of the OPEC+ aggregate. As a result, by July 12 crude oil prices had returned to around $80/b, the desired range of OPEC+ members. Following the sluggish start to the second half of 2023, it is an open question how OPEC+ will navigate the new market conditions.

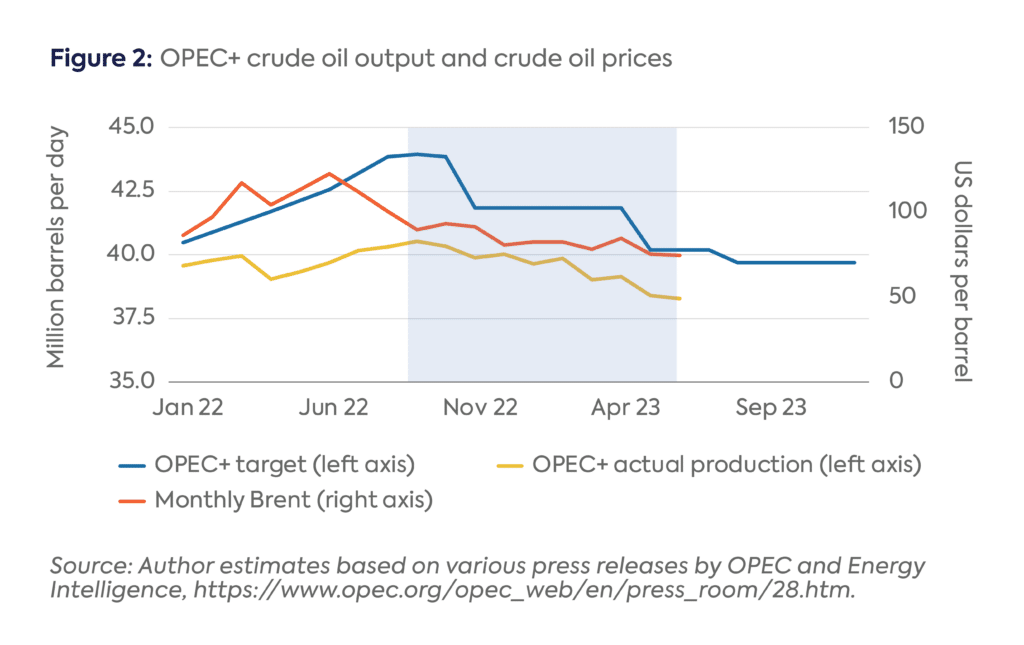

OPEC+ has consistently been in tightening mode since October 2022. Between September 2022 and June 2023 (shaded area in Figure 2), OPEC+’s overall production target has come down by 3.8 million barrels per day (b/d), a level that is expected to be sustained until the end of the year. The stated production target for 2024 would imply an increase of just 264,000 b/d from today’s levels.[5] The group’s quotas through February 2023 were decided and announced by the Joint Ministerial Monitoring Committee. But that changed when Russia voluntarily announced a cut in its production target by 500,000 b/d from March 2023, and eight other member countries joined Russia by announcing their own voluntary cuts in April 2023.[6] The latest salvo in this attempt to manage the market is the Saudi production cut of 1 million b/d for July and August 2023, which could potentially be extended by a few more months,[7] and the Russian cut of an additional 500,000 b/d in crude oil exports.[8] By coordinating the latest round of cuts, Saudi Arabia and Russia are also signaling their joint commitment to support crude oil prices. The Saudi production cut for July reportedly came as a surprise even to other OPEC+ member countries.[9]

More significantly, OPEC+’s actual production has consistently trended well below its stated targets (Figure 2). Chronic lack of investment and poor management of the upstream sector in numerous member states have structurally affected their ability to meet production quotas. Angola, Azerbaijan, Malaysia, Mexico, and Nigeria are all underperforming their production targets by more than 100,000 b/d. Beyond the core Middle Eastern OPEC members and Russia, the shortfall in actual production compared to the stated targets was 825,000 b/d in June 2023.[10] Nevertheless, oil prices have been range-bound between $70/b and $80/b so far in 2023, with a moderate downward slope from the higher end of the range at the start of the year to the lower end by June, despite two rounds of unexpected cuts from OPEC+ in March and April, and then another in early June. In fact, the momentary bump in crude oil prices following the April 2023 announcement of the last set of production cuts was fully offset by macroeconomic concerns within two weeks.[11]

The key market features in the first half of 2023 were a lack of inventory draws (signaling weak market fundamentals) and macroeconomic concerns weighing on commodity markets in general. Questions about the health of the global economy added further uncertainty to the oil market balance. Rapid central bank rate increases to fight inflationary pressures led to a slowdown in manufacturing and industrial activity, as well as multiple banking/financial crises centered in the United States.[12] China was also an area of concern due to its slow pace of recovery from its zero-COVID policy and ongoing questions around its unsustainable level of domestic debt in the property sector.[13] While Chinese oil imports in the second quarter of 2023 (2Q23) were extremely robust, concerns about domestic demand linger because much of the increase in imports went into storage to build inventories.[14] On the other hand, despite somewhat sluggish Organisation for Economic Co-operation and Development (OECD) consumption, emerging market demand remained resilient in the first half of the year (macroeconomic concerns notwithstanding). Based on the latest monthly updates from the International Energy Agency (IEA) and the US Energy Information Administration (EIA), oil demand increased from 100 million–100.5 million b/d in 1Q23 to 101 million–101.5 million b/d in 2Q23.[15] In its analysis, OPEC also reported consumption levels of more than 101 million b/d in 2Q23.[16]

Supply resilience has been a thorn in the side of OPEC+ decision makers in the first half of the year, putting pressure on them to intervene and remove excess supply from the market. Despite a G7-imposed price on Russian oil and an EU-wide embargo on seaborne oil imports from Russia, Russian oil exports have been strong: led by buying from India and China, they rose from roughly 3.4 million b/d of exports in the first few months of the year to as high as 3.7 million b/d by June before cuts started kicking in.[17] Iran also proved to be a source of rebounding supply, rising from about 1 million b/d at the start of the year to more than 1.5 million b/d by May.[18] Elsewhere, non-OPEC+ supply from the United States and Latin America has also picked up. Thus, despite the OPEC+ cuts since March, the overall market has been adequately supplied, OECD inventories rose gradually between January and June, and Chinese stocks drove non-OECD inventories higher in 2Q23.[19] This constellation of factors left OPEC+ with little choice but to cut production targets, increasingly limiting its ability to support prices.

Based on the demand outlook from the major agencies as well as other industry forecasters, the supply cuts from OPEC+ led by Saudi Arabia are set to lead to a fairly sizeable draw in inventories in 3Q23 and possibly a further cut in 4Q23. If demand hits expected levels for 3Q23, the inventory draws could be as large as 1.5 million to 2 million b/d. The US Department of Energy’s (DOE) program to refill its Strategic Petroleum Reserves (SPR) will also contribute to the market tightness in the second half of 2023.[20] With one tranche expected in September and another in October, a total of 12 million barrels of SPR refill has already been solicited by the DOE—modest but further incremental demand.

A hard landing of the US and other Western economies (perhaps more of a concern in Europe than the US given recent data) and continued weakness of the Chinese economic recovery remain the key risks to forecasts of a supply deficit and crude prices in the $80/b range for the remainder of 2023. If either of these are realized, annual demand growth may be weaker than the 2.1 million b/d that the EIA, IEA, and OPEC currently forecast (on average).[21] However, with Saudi Arabia’s deep cuts in place for at least July and August, the oil inventory drawdowns should be at least 500,000–1 million b/d this quarter, even amid slightly weaker demand. The cut in Russian exports will also be supportive of markets. After their outperformance in the first half of 2023, Russian oil export levels are showing signs of dropping—below 3.2 million b/d in early July, down from 3.6 million–3.7 million b/d in June.[22] Whether Russia continues to honor its pledge over the coming months will influence market balances, and potentially buoy prices at or above the $80/b threshold.

Record-high budget surpluses and oil company profits in 2022 have given way to lower oil revenues in 2023 thus far. With coming production cuts likely to hit oil revenues even further, the macroeconomic prospects for OPEC+ countries remain bleak for the rest of the year. For instance, the contribution of the oil sector to Saudi GDP is expected to decline in 2023, with the fiscal balance returning to deficit after a surplus in 2022, the first in almost a decade.[23] The International Monetary Fund estimates a fiscal breakeven oil price for Saudi Arabia of more than $80/b, which will inch higher after the further voluntary cuts announced for July and August are implemented.[24] Appearing to be targeting higher prices, Saudi Aramco hiked its official selling price (OSP) for Asian buyers in July 2023 accordingly.[25] Other major OPEC producers, namely, Iraq, the United Arab Emirates, and Kuwait, have also increased their OSPs for July[26] in the face of worsening fiscal balances.[27] Thus, sustaining the current strategy of supporting crude prices with production cuts will strain the fiscal balances of OPEC+ countries.

Group cohesion will also be tested in the coming months. The heavy lifting in terms of production cuts has been largely done by Saudi Arabia, and to a lesser extent the other Middle Eastern OPEC members. It is only now that Russian exports are starting to decline. This trend will be closely watched by the core OPEC members, particularly those that voluntarily decided to cut production. For Russia, the recent increase in the price of Russian crude will offset some of the loss in oil revenue from lower exports, but the overall impact will be limited by the G7 price cap on Russian crude.[28] In terms of the Middle Eastern member countries, rising tensions between the two largest producers, Saudi Arabia and the UAE, over crude oil exports as well as geopolitical and strategic matters have been reported.[29] Overall, OPEC+ spare capacity was more than 4 million b/d before July and currently exceeds 5 million b/d with the incremental Saudi cut—over 75 percent of which lies with Saudi Arabia and the UAE (up to 90 percent in the Middle East), contributing to the potential rivalry between these two states.[30] The growth in exports from OPEC members currently outside the production quota system is also likely to put pressure on the coalition. This would likewise affect the proposed review of the post-2025 production quotas for all OPEC+ that is said to be based on their production in 2023.[31] More significantly, the production quotas for the major African producers, namely Algeria, Angola, and Nigeria, have provisionally been reduced given their underperformance in 2023. Together, these three countries lagged just under 1 million b/d compared to their production target in June 2023,[32] and are increasingly likely to see their influence diminish as the coalition renegotiates production targets for 2024 and beyond.[33]

OPEC+ strategy remains a tightrope walk between supporting crude oil prices and maintaining group cohesion. While extending the current production cuts will affect oil revenues and hence fiscal balances, reversing them will push prices below breakeven levels. As important as OPEC+ targets have been to managing supply, other factors are more strongly influencing oil markets. And while the drama of OPEC+ meetings and heated rhetoric around supply cuts will continue to capture the headlines, the past few months have revealed that the group’s ability to manage the crude oil market and influence prices is weaker. Only a stronger recovery in demand can enable OPEC+ to regain its control of the market and the ability to support prices. The coalition’s unity will also be tested if weak market fundamentals and the pressure on fiscal balances continue. OPEC+ production targets matter, but only if there is an appetite to consume its barrels.

[1] The oil price at which the current account balance is zero.

[2] The ten other oil exporters include Azerbaijan, Bahrain, Brunei, Kazakhstan, Malaysia, Mexico, Oman, Russia, Sudan, and South Sudan.

[3] International Monetary Fund, “Regional Economic Outlook: The Middle East and Central Asia–Statistical Appendix,” May 2023, https://www.imf.org/-/media/Files/Publications/REO/MCD-CCA/2023/April/English/may-2023-meca-regional-economic-outlook-statistical-appendix-eng.ashx.

[4] Energy Intelligence, “Break-Even Price Outlook,” May 4, 2023, https://www.energyintel.com/2023-05-04/break-even-price-outlook-may-2023-update.

[5] Organization of the Petroleum Exporting Countries, “35th OPEC and non-OPEC Ministerial Meeting No 08/2023,” June 4, 2023, https://www.opec.org/opec_web/en/press_room/7160.htm.

[6] Kaushik Deb and Abhiram Rajendran, “OPEC+ Cuts Production Targets, Again,” Energy Explained, Center on Global Energy Policy, April 11, 2023, https://www.energypolicy.columbia.edu/opec-cuts-production-targets-again/.

[7] Saudi Press Agency, “Ministry of Energy: Saudi Arabia Will Extend the Voluntary Cut of One Million Barrels per Day for Another Month to Include August,” July 3, 2023, https://www.spa.gov.sa/en/620f8a971dh.

[8] The Russian Government, “Alexander Novak’s Statement on Oil Market Situation,” July 3, 2023, http://government.ru/en/news/48920/.

[9] Dmitry Zhdannikov, Ahmad Ghaddar, and Alex Lawler, “Inside OPEC+, Saudi ‘Lollipop’ Oil Cut Was a Surprise Too,” Reuters, June 9, 2023, https://www.reuters.com/business/energy/inside-opec-saudi-lollipop-oil-cut-was-surprise-too-2023-06-09/.

[10] S&P Global, “OPEC+ June Crude Output Relatively Steady Ahead of Further Saudi Cut: Platts Survey,” July 12, 2023, https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/oil/071123-opec-june-crude-output-relatively-steady-ahead-of-further-saudi-cut-platts-survey.

[11] Lily Jamali, “To Stay Atop the Oil Market, OPEC Became OPEC+. But Keeping the Cartel in Sync Isn’t Easy,” Marketplace, June 28, 2023, https://www.marketplace.org/2023/06/28/keeping-oil-cartel-opec-in-sync-isnt-easy/.

[12] International Monetary Fund, “World Economic Outlook: A Rocky Recovery,” April 2023, https://www.imf.org/-/media/Files/Publications/WEO/2023/April/English/text.ashx.

[13] Kimberley Long, “China’s Economy Faces Local Debt and Real Estate Woes,” Banker, June 29, 2023, https://www.thebanker.com/China-s-economy-faces-local-debt-and-real-estate-woes-1688024393.

[14] Andrew Hayley, “China’s June Crude Imports Soar 45.3% Year over Year as Inventories Build,” Reuters, July 13, 2023, https://www.reuters.com/markets/asia/chinas-june-crude-imports-soar-453-previous-year-2023-07-13/.

[15] International Energy Agency, “Oil Market Report,” July 2023, https://www.iea.org/reports/oil-market-report-july-2023; US Energy Information Administration, “Short-Term Energy Outlook STEO July 2023,” July 11, 2023, https://www.eia.gov/outlooks/steo/.

[16] Organization of the Petroleum Exporting Countries, “Monthly Oil Market Report,” July 13, 2023, https://www.opec.org/opec_web/en/publications/338.htm.

[17] Tsvetana Paraskova, “Russia’s Crude Oil Exports Still Higher than before It Pledged to Cut,” OilPrice.com, June 20, 2023, https://oilprice.com/Energy/Energy-General/Russias-Crude-Oil-Exports-Still-Higher-Than-Before-It-Pledged-To-Cut.html.

[18]Alex Lawler, “Iran’s Oil Exports Hit 5-Year Highs as US Holds Nuclear Talks,” Reuters, June 16, 2023, https://www.reuters.com/markets/commodities/irans-oil-exports-output-hit-five-year-highs-us-holds-nuclear-talks-2023-06-16/.

[19] International Energy Agency, “Oil Market Report,” July 2023, https://www.iea.org/reports/oil-market-report-july-2023.

[20] US Department of Energy, “DOE Announces 6 Million Barrels for Strategic Petroleum Reserve Replenishment,” June 9, 2023, https://www.energy.gov/articles/doe-announces-6-million-barrels-strategic-petroleum-reserve-replenishment; US Department of Energy, “DOE Announces Plans to Purchase Another 6 Million Barrels of Oil for Strategic Petroleum Reserve Replenishment,” July 7, 2023, https://www.energy.gov/articles/doe-announces-plans-purchase-another-6-million-barrels-oil-strategic-petroleum-reserve.

[21] International Energy Agency, “Oil Market Report,” July 2023, https://www.iea.org/reports/oil-market-report-july-2023; US Energy Information Administration, “Short-Term Energy Outlook July 2023,” July 11, 2023, https://www.eia.gov/outlooks/steo/.

[22] Charles Kennedy, “Russia’s Crude Oil Exports Start to Show Signs of Decline,” OilPrice.com, July 11, 2023, https://oilprice.com/Latest-Energy-News/World-News/Russias-Crude-Oil-Exports-Start-To-Show-Signs-Of-Decline.html; “Russia Finally Cuts Crude Exports, at Most Opportune Moment,” Bloomberg, July 13, 2023, https://www.bloomberg.com/news/articles/2023-07-13/russia-finally-cuts-crude-exports-at-the-most-opportune-moment.

[23] Jadwa Investment, “Q1 2023 GDP Update,” June 2023, http://www.jadwa.com/sites/default/files/2023-06/Q1%202023%20GDP%20update.pdf; Jadwa Investment, “Q1 2023 Budget Performance Report,” May 2023, http://www.jadwa.com/sites/default/files/2023-06/Q1%202023%20GDP%20update.pdf.

[24] International Monetary Fund, “Regional Economic Outlook: The Middle East and Central Asia–Statistical Appendix,” May 2023, https://www.imf.org/-/media/Files/Publications/REO/MCD-CCA/2023/April/English/may-2023-meca-regional-economic-outlook-statistical-appendix-eng.ashx.

[25] S&P Global, “Asian Buyers Likely to Cut Saudi Crude Nominations after Aramco Hike in July OSP Differentials,” June 6, 2023, https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/oil/060623-asian-buyers-likely-to-cut-saudi-crude-nominations-after-aramco-hike-in-july-osp-differentials.

[26] “UAE’s ADNOC Sets August Murban Crude OSP at $75.61/bbl,” Reuters, July 11, 2023, https://www.reuters.com/article/emirates-adnoc-murban/uaes-adnoc-sets-august-murban-crude-osp-at-75-61-bbl-idUKL4N38X3L2; “Kuwait Raises July Crude Prices for Asia–document,” Reuters, June 12, 2023, https://www.reuters.com/article/kuwait-oil-prices/kuwait-raises-july-crude-prices-for-asia-document-idUSL4N3841PJ.

[27] International Monetary Fund, “Regional Economic Outlook: The Middle East and Central Asia–Statistical Appendix,” May 2023, https://www.imf.org/-/media/Files/Publications/REO/MCD-CCA/2023/April/English/may-2023-meca-regional-economic-outlook-statistical-appendix-eng.ashx.

[28] Alaric Nightingale and Lucia Kassai, “Russia’s Flagship Crude Oil Surpasses G-7 Price Cap for First Time,” Bloomberg, July 12, 2023, https://www.bloomberg.com/news/articles/2023-07-12/russia-s-flagship-crude-surpasses-g-7-price-cap-for-first-time#xj4y7vzkg.

[29] Summer Said, Dion Nissenbaum, Stephen Kalin, and Saleh al-Batati, “The Best of Frenemies: Saudi Crown Prince Clashes With U.A.E. President,” July 18, 2023, https://www.wsj.com/articles/frenemies-saudi-crown-prince-mbs-clashes-uae-president-mbz-c500f9b1.

[30] Energy Intelligence, “Oil Price Driven by More Than Macro Fears,” https://www.energyintel.com/00000189-4bfc-d60a-a38f-cffe88ba0000.

[31] Organization of the Petroleum Exporting Countries, “35th OPEC and non-OPEC Ministerial Meeting No 08/2023,” June 4, 2023, https://www.opec.org/opec_web/en/press_room/7160.htm.

[32] Rosemary Griffin, Herman Wang, and Charlie Mitchel, “OPEC+ June Crude Output Relatively Steady Ahead of Further Saudi Cut: Platts Survey,” July 11, 2023, https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/oil/071123-opec-june-crude-output-relatively-steady-ahead-of-further-saudi-cut-platts-survey.

[33] S&P Global, “FEATURE: Sliding Oil Production Costs Africa Influence at OPEC,” May 31, 2023, https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/oil/053123-feature-sliding-oil-production-costs-africa-influence-at-opec.

The White House declared last week that President Trump finally "broke OPEC" after the United Arab Emirates withdrew from the cartel.

Full report

Commentary by Kaushik Deb & Abhiram Rajendran • August 01, 2023