This website uses cookies as well as similar tools and technologies to understand visitors’ experiences. By continuing to use this website, you consent to Columbia University’s usage of cookies and similar technologies, in accordance with the Columbia University Website Cookie Notice.

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

As President Biden’s national security advisor, Jake Sullivan laid out a strategy for what he called a “foreign policy for the middle class.” Using the metaphor of a...

Please join the Women in Energy initiative at the Center on Global Energy Policy at Columbia SIPA for a public roundtable featuring Claire Steichen, Founder of Clear Strategy Coaching. The fast-evolving energy...

Event

• Online

About Us

We are the premier hub and policy institution for global energy thought leadership. Energy impacts every element of our lives, and our trusted fact-based research informs the decisions that affect all of us.

This commentary represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. More information is available at Our Partners. Rare cases of sponsored projects are clearly indicated.

Introduction

Prior to 2022, the European Union (EU) natural gas market was reasonably well developed and well supplied, with the EU drawing upon diverse sources in Norway, the UK, Algeria, and, most importantly, Russia, as well as liquefied natural gas (LNG) from various sources, including Russia.[1] This market structure gave buyers in the European Union the ability to pick and choose among their suppliers, which favored Russian pipeline gas chiefly because of legacy infrastructure and price. Policy makers and fuel purchasers would in principle be able to impose environmental conditions on imported fossil fuels without suffering undue price escalation. The rejection of a large US LNG contract in 2020, presumably on environmental grounds, reinforced this expectation.[2] In reality, scant evidence exists that EU policy makers have until recently used their position to advocate in a structured manner for higher environmental standards with their key suppliers of natural gas.

On December 15, 2021, the European Commission (EC) published a proposal for a regulation on methane emission reductions in the energy sector.[3] The EC aimed to require domestic oil, natural gas, and coal producers to measure, report, and verify methane emissions, prescribe stricter rules to detect and repair methane leaks, and limit venting and flaring within the EU. In addition, the EC proposed global monitoring tools to improve transparency of methane emissions associated with the imports of oil, natural gas, and coal into the EU. This latter proposal is a stepping stone toward possible regulation of imported fuels, which constitute a large fraction of the energy the EU consumes.

Seventy-two days later the Russian Federation attacked Ukraine with ground, air, and amphibious forces. The invasion and subsequent escalation of trade disputes and mutual embargoes, explicit and implicit, upset established trading patterns between the European Union and the Russian Federation. New trade patterns bring with them a new set of concerns when designing regulations with extraterritorial effect. This is particularly true when pipeline natural gas imports from the Russian Federation are replaced by liquefied natural gas imports from the United States.

In this commentary, the authors describe changes in the natural gas trade that confronted the European Union in 2022. They then discuss Russian attitudes toward greenhouse gas control in general, and methane emission control in particular, and contrast these with contemporary attitudes and actions in the United States. Finally, the authors describe European emission control proposals in the context of the changing landscape of international energy trade, along with remaining challenges.

Recent turmoil in the European natural gas market has injected uncertainty into many economic and environmental plans and initiatives. However, as the authors will show, the drafters of the EC’s proposed methane regulations have fortuitously created a legislative pathway reasonably well adapted to the current situation.

The Changing Nature of the International Gas Trade

In the last several decades, natural gas has assumed increasingly important roles in the world’s energy economy. It is less polluting than coal at every stage of its life cycle, and when used as a fuel has a significantly smaller greenhouse gas footprint than either coal or oil. As concerns about global climate change have come to the fore, the latter consideration has loomed large in the energy planning of many of the world’s largest consumers of fuels.

The Russian Federation is the second largest producer of natural gas in the world (after the United States), and the world’s largest exporter of this commodity.[4] The great hydrocarbon basins of western Russia have increasingly been seen as plentiful, low-cost sources of energy for the Europe Union, which has over the years largely depleted or shut down its own gas fields. Russian gas has mostly been supplied by pipelines, which are the most efficient way to move gas across continents and small seas like the Baltic and the Mediterranean. Recently, Russian pipeline gas has been supplemented by liquefied natural gas shipped through the Arctic from the Yamal Peninsula.

With domestic production of gas accounting for only 11 percent of its needs,[5] the EU took measures to diversify its sources of natural gas, while improving its internal transmission infrastructure. Norway, Algeria, and Qatar are regular suppliers. Nonetheless, in January 2021 Russia supplied 40 percent of the European Union’s consumption of natural gas.[6]

Russian President Vladimir Putin has made no secret of his ambition to reassemble the Greater Russia that was controlled from Moscow for centuries before the breakup of the Soviet Union in 1991. In 2014 Russia seized Crimea and parts of Donbas, with no evidence that these conquests satisfied Russian territorial ambitions. The European Union took no action to resist the Russian advances of 2014, and the reduction of gas exports from Russia to Europe that began in mid-2021 may have been the first steps in putting pressure on Europe to maintain its passivity with respect to Russian encroachments on Ukraine.[7]

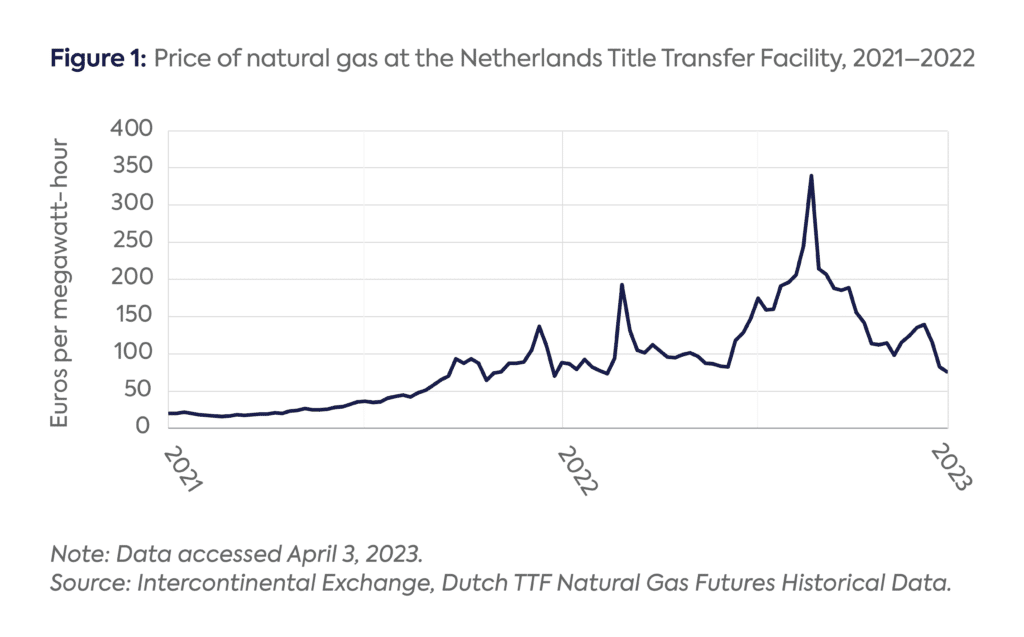

This time, however, Europe stood firm in moral, financial, and material support of the defense of Ukraine, and in the summer of 2022, Russia more sharply limited its natural gas exports to Europe in response. From January 2022 to March 2023, Russian pipeline exports of gas to the EU fell from 12.99 billion cubic meters (bcm) per month to 2.02 bcm per month, an 84 percent decline.[8] The result was a scramble for gas supplies that has, so far, been successful, but at the cost of unprecedented volatility in the cost of natural gas, which averaged €142 per megawatt hour (MWh) (€42 per million British thermal units [MMBtu]) for March to November 2022[9] (see Figure 1), during which time the euro swung from $1.21 to $0.98. During the same period the price of US natural gas at Henry Hub averaged approximately $7/MMBtu.[10] Prices have recovered to more normal levels since, and concerns about physical shortages have eased. However, sabotage of the Nord Stream 1 and 2 pipelines on September 26, 2022, makes it unlikely that Russian pipeline exports to the EU will resume at previous levels in the foreseeable future.

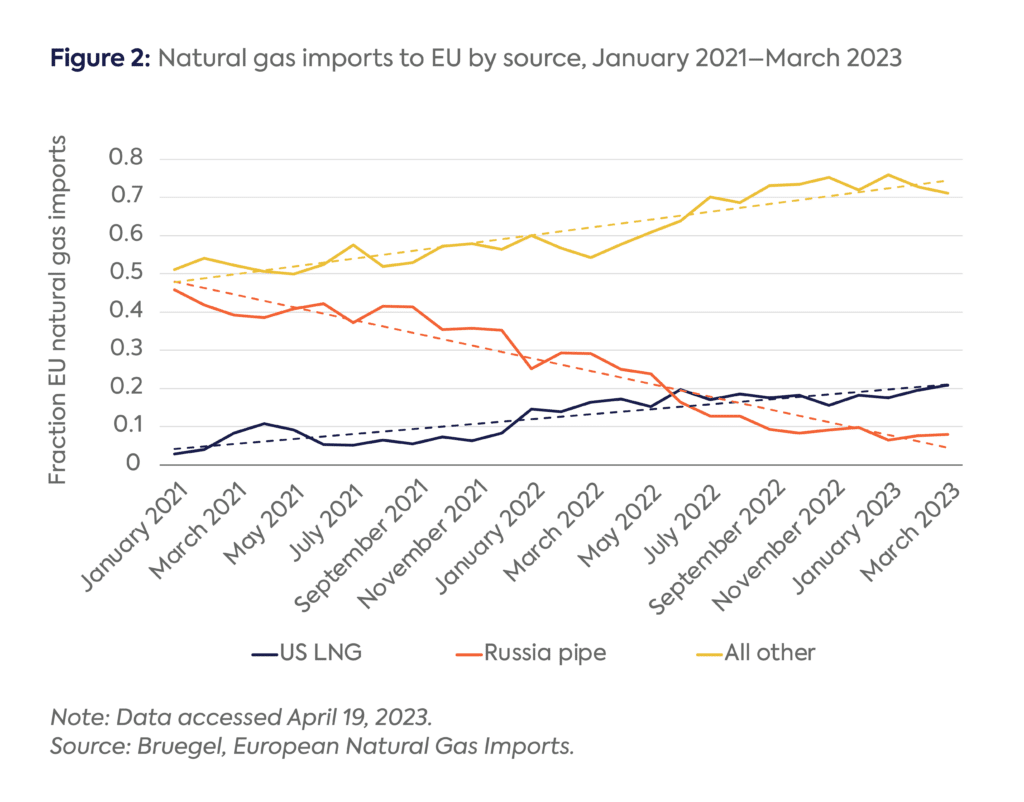

Throughout 2022, Europe labored mightily to construct new energy import channels, particularly for liquefied natural gas. Revitalizing or resuming domestic production (as in the Netherlands, for example) seems never to have been truly under consideration. In 2021, the EU imported 74 bcm of LNG; a year later it imported 123 bcm,[11] an increase of 49 bcm. Of that increase, 36 bcm came from the United States[12]).

EU natural gas imports by source between January 2021 and March 2023 is provided in Figure 2. The decline of natural gas pipeline imports from Russia was compensated by increases of US LNG and other imports. In addition, demand decreased in 2022 and 2023 due to conservation efforts and an unusually warm winter in 2022–23.

Exports from the United States to Europe are likely to grow still larger. In the first half of 2022, LNG exports to all destinations from the United States totaled 11.1 billion cubic feet per day (an annual rate of 115 bcm).[13] By January 2026, US export capacity is expected to reach 20 billion cubic feet per day (an annual rate of 207 bcm),[14] and market forces may well dictate that much of those volumes go to European markets. Although the majority of new offtake agreements have been signed by non-EU buyers, many of these agreements are with portfolio players—aggregators who deal with a variety of suppliers and customers[15]—and US LNG contracts generally are notable for their absence of destination clauses.[16]

Russian Attitudes Toward Greenhouse Gas Emissions

The Russian Federation has a complicated relationship with climate change in general and greenhouse gas (GHG) emissions in particular. Climate modeling suggests that temperature and precipitation changes resulting from increasing concentrations of greenhouse gases in the atmosphere will benefit the human population of European Russia while not significantly improving the habitability of northern Siberia and the Russian Far East.[17] Although Russia is at present the largest exporter of wheat in the world, and its agricultural sector would seem to benefit from global warming, the overall outlook for agriculture is complex and certainly not all positive.[18] Fossil fuels are the main source of export earnings and, predictably, the leadership of the Russian Federation has adopted a skeptical stance toward the connection between hydrocarbon production and consumption and potential adverse effects of climate change.[19] Like most countries, Russia has done little to limit carbon dioxide emissions.

Carbon dioxide emissions are an inescapable consequence of fossil fuel use; their reduction will inevitably entail large economic and social disruptions. This is not true of methane, the emissions of which are not a necessary aspect of oil and gas production and consumption. There is no economic benefit associated with releasing methane into the atmosphere. Therefore, major oil and gas producers have willingly joined methane reduction programs.[20] The major Russian gas exporters, Gazprom and Novatek, have joined methane reduction consortia, and President Putin himself has spoken of the desire to reduce releases of methane.[21]

Lack of Evidence for Methane Emission Control

While both the government and gas producers of Russia have acknowledged the importance of methane emission control, evidence of progress is unreliable. Methane emissions are unusually difficult to measure or estimate, even in jurisdictions where other industrial outputs and pollutants are accurately reported. For example, carbon dioxide emissions resulting from combustion of fossil fuels are accurately determined from the quantity of fuel consumed and the amount of carbon dioxide released per unit of consumed fuel, both of which are generally well known. By contrast, methane emissions are not released in proportion to the production of a commodity.[22] Large emitters are usually intermittent and therefore need to be continuously monitored in order to be reported accurately.[23]

This problem is far from unique to Russia—internationally, reliable data on methane emissions from fossil fuel industries is scarce. But a combination of natural and human factors make Russian data particularly unreliable. The difficulty of recovering methane emission data from Russia is a major barrier to the measure-report-verify (MRV) program proposed by the European Commission to better understand the life cycle GHG emissions of its imported fossil fuels.

Russian Government Reports

Russia is a signatory of the United Nations Framework Convention on Climate Change (UNFCCC). As one of the 43 Annex I nations—which include most industrialized countries, including the Russian Federation and Ukraine, but not China[24]—Russia submits an annual report of its greenhouse gas emissions to the secretariat of the UNFCCC. Like the reports of other Annex I nations, Russia’s relies on the emission factor method. Although this method is widely used, it has been repeatedly shown to be a poor estimator of methane emissions.[25] Moreover, the Russian implementation of the emission factor method is particularly crude, and subject to dramatic year-to-year variations.[26]

Non-Governmental Organization Inventories

A number of non-governmental organizations also publish estimates of methane emissions. The most widely quoted is the International Energy Agency (IEA), with a reputation for gathering and disseminating reliable resource and economic data. The IEA methodology illustrates the uncertainties in estimating methane emission data.[27] It uses the EPA’s 2022 Inventory of US Greenhouse Gas Emissions and Sinks,[28] among other credible sources, and scales US emission intensity to other nations based on country-specific factors such as infrastructure age, type of operator, and average flaring intensity. Note that measurements play little if any role in any of these estimates. The reason is simple: measurements are inadequate relative to the scale of the problem in the United States, and there are scarcely any measurements at all elsewhere.

Aircraft Surveillance

Faced with inadequacy of spreadsheet inventories, numerous government, academic, and NGO groups have undertaken surveys of oil and gas industry infrastructure. The most widespread and successful of these have been performed by aircraft, which can efficiently survey large oil- and gas-producing basins. Recent surveys have occasionally visited tens of thousands or hundreds of thousands of individually identified gas and oil production and transmission sites in the United States,[29] with smaller surveys being conducted in Canada,[30] Mexico,[31] and a few other hydrocarbon-producing nations. Accuracy has been validated by controlled-release measurements.[32] In the United States and Canada such surveys may be conducted by anyone obeying routine flight safety rules, without the permission of the government or resource owners and operators. This is not the case in Russia, and the authors are not aware of any aircraft surveillance of oil and gas facilities there.

Satellite Surveillance

Global total methane emissions can be estimated with reasonable accuracy by satellites. However, country-level emission estimates are far more uncertain, even for a large country such as Russia, and for particular economic segments such as the fossil fuel industry.[33]

At least some of the uncertainty of satellite-based determinations is due to the inescapable limitations of the data and processing. Satellite data do not distinguish between natural and anthropogenic sources, nor between fossil fuel and other anthropogenic sources. Moreover, wet snow and limited and low-angle daylight are important limitations at high latitudes, affecting satellite performance in large portions of the Volga-Urals, Timan-Pechora, and Western Siberia sedimentary basins, which are among Russia’s prime oil- and gas-producing regions. However, satellite surveillance techniques are steadily improving.[34]

Influencing Fossil Fuel Exporters

Until 2022 Europe was virtually a monopsony purchaser of western Russian pipeline gas. This gave the EU a strong basis upon which to dictate environmental terms and conditions, and Russia appeared to recognize it would have to pay attention to methane emissions for the sake of pacifying its most important natural gas customer.[35] However, Russia is also infamous for its relatively lax environmental controls[36] and an unreliable greenhouse gas emission reporting regime,[37] so Europe could have expected an uphill battle to persuade its neighbor to the east to take all the measures necessary to bring Russian upstream and midstream practices up to European standards. Barring unexpected regime change, it now appears highly unlikely Europe will seek to regain its commanding purchasing power over Russia.

As a fossil fuel supplier, the United States presents a different picture. Although US government greenhouse gas reporting systems still use the antiquated emission factor method that requires no measurements of equipment operating in the field, these data have been supplemented by rapidly accumulating knowledge supplied by academics and environmental advocates. Accurate, efficient data collection has been enabled by a developing ecosystem of technically adept methane measurement service providers.[38] The idea that natural gas produced using methods that reduce its greenhouse gas impact might command market advantages[39] is being implemented by a plethora of industry associations and commercial service providers through voluntary emission reduction efforts.[40] As a result, official reports have been increasingly overshadowed by private sector methane measurements that have improved steadily in both quality and quantity over the last 10 years.[41]

Largely as a result of this activity, the United States is moving aggressively on its own course of methane emission reduction. Methane control regulations from 2012 and 2016 have had little or no effect,[42] and 2020 rule changes, minimal in any event, were largely withdrawn by Congress.[43] In November 2022, the Environmental Protection Agency released a fourth attempt to regulate emissions of methane,[44] and the Inflation Reduction Act of 2022[45] includes many constructive measures expected to have real methane emission reduction effects.[46]

The United States and the European Union have embarked on simultaneous but apparently uncoordinated development of methane regulations.[47] Given that the United States is the world’s largest producer of natural gas, and on track to be a leading exporter of natural gas to Europe, closer intergovernmental cooperation would appear to be mutually beneficial.[48] In this respect, the cautious approach of the European Commission legislative proposal may prove salutary. Europe’s plan to gather information prior to extending its methane control regime to imported fossil fuels will give the trading partners an opportunity to coordinate their environmental protocols.

Furthermore, over the next two years, gas supplies to Europe are expected to be constrained and commercial channels will be under stress.[49] Perhaps fortuitously, this period coincides with the information gathering effort just referred to.

Therefore, the displacement of Russia by the United States as a leading provider of natural gas, taken together with recent US and EU actions on methane, could have the effect of simplifying and accelerating Europe’s campaign to reduce the greenhouse gas footprint of its imported fossil fuels. The following section examines details of the EC methane emission reduction regulation proposed in late 2021 within this context to gauge its prospects for success.

EC Draft Regulation: Context, Objectives, and High-Level Overview

The EC legislative proposal of December 2021 had two objectives: (1) to improve the accuracy of data on the main sources of methane emissions associated with energy produced and consumed in the EU, and ensure further reduction of methane emissions across the energy supply chain within the EU; and (2) to improve the availability of methane emission information on imported fossil fuels with the objective of eventually providing incentives for their reduction. Given that the majority of energy consumed in the EU (particularly from oil and natural gas) is imported to the region, the second objective seems the more relevant from an emission reduction point of view. Yet, as EU law typically applies only within EU jurisdiction, it is also the more challenging one.

How does the EC envision achieving these objectives? To comply with World Trade Organization rules, Europe must impose upon its domestic producers any environmental rules it may seek to impose on its imports. Therefore, the December 2021 regulation contains rules for the accurate measurement, reporting, and verification of methane emissions in the energy sector within the EU, as well as for the abatement of those emissions, including through leak detection and repair surveys, and restrictions on venting and flaring.

The second step is to promulgate rules that advance transparency of methane emissions from fossil fuels imported to the EU. This regulation applies to (1) oil and natural gas upstream exploration and production, gathering, and processing; (2) natural gas transmission, distribution, underground storage, and liquid natural gas terminals operating with fossil and/or renewable methane; and (3) underground and surface coal mines, and closed and abandoned coal mines. Some provisions have been watered down in the most recent version of the proposal,[50] including the extension of inspection times for all equipment from three months to six months, the exemption of these rules for offshore wells deeper than 700 meters, and the exemption of some offshore abandoned or inactive wells. In addition, the inspection of flare stacks was altered from weekly to monthly.

Section 58 of the legislative proposal states that importers of fossil energy should be required to disclose to relevant member states information related to measurement, reporting, and mitigation of methane emissions undertaken by foreign producers and exporters. These include the application of regulatory or voluntary measures to control their methane emissions. Article 28 requires the EC to establish and maintain a methane transparency database containing importer requirements within 18 months of enactment, and Article 29 requires the EC to establish a global methane monitoring tool based on satellite data and input from several certified data providers and services two years after enactment.

Perhaps to counter the watered-down rules, a provision was inserted requiring the EC to look into the implications of extending the objective of the regulation related to EU countries to those exporting to the EU as part of the first revision of the law. The EC is to submit this analysis to the European Parliament and the Council no later than 12 months after the regulation is enacted and, depending on the outcome of such an analysis, submit appropriate legislative proposals to extend the regulation to importers.[51]

The EC could be proposing this legislation as a signal to the world that it wants to lead in addressing fugitive and vented methane emissions, and wants to work with its international partners to do so. As part of the legislative process, the EC organized several workshops and consultations prior to publication of this proposal.[52] All oil and gas associations expressed support for putting leak detection and repair (LDAR) obligations into EU law.[53] All industry respondents also indicated that they think routine venting and flaring can be phased out. Moreover, 72 percent of respondents indicated that EU legislation on methane in the energy sector should extend obligations to companies importing fossil fuels into the EU. Therefore, the proposal includes a review clause explicitly referring to the EC’s prerogative to submit amending legislative proposals to impose more stringent measures on importers once more granular global methane emission data become available.

With regard to monitoring and evaluating the obligations set out in this proposal, the main responsibility will lie with “national competent authorities,” which in many cases will be the national regulatory authorities at the EU member state level. The proposal also provides a role for independent accredited verifiers for emission data verification. The International Methane Emissions Observatory (IMEO) will provide additional scrutiny of submitted methane emission data, including the possibility to cross-reference them with other sources such as satellite imaging and related data products.

Currently, countries report data to the UNFCCC, and can typically do so in three tiers, which represent methodological complexity. Tier 1 utilizes global-average default emission factors, Tier 2 uses country-specific emission factors, and Tier 3 requires “rigorous source emission models.”[54] Currently, reporting at the most basic Tier 1 level is still very common among EU member states. Voluntary industry-led initiatives are the principal course of action for improvement of methane emission quantification and mitigation, the Oil and Gas Methane Partnership (OGMP) being a prominent example.[55] The EC’s proposed regulation builds on the most recent OGMP framework (at the time of writing, 2.0), which has five levels of reporting. Source-level reporting begins at level 3 in this framework, which allows for generic emission factors to be used. OGMP 2.0 level 4 reporting requires direct measurements of source-level emissions (allowing the use of specific emission factors), whereas level 5 reporting requires the addition of complementary site-level measurements. Further building on OGMP 2.0, the EC proposes EU operators deliver direct source-level measurements of their emissions from operated assets within 24 months of the regulation being enacted, and from non-operating assets within 36 months. Finally, the EC will work with the IMEO to set up a methane supply index, to better inform natural gas purchasers of the environmental footprint of their purchases.

More details of the EC draft regulation can be found in the Appendix.

In December 2022, European energy secretaries reached a preliminary deal on the proposed regulation.[56] The European Parliament in May 2023 issued its opinion that the rules as agreed in December should be strengthened, and that their provisions should apply to companies importing fossil fuels to the EU no later than 2026.[57] Final negotiations between the EU institutions (trilogues) can now commence, and the draft regulation will likely be adopted later this year, or early next.

Jurisdictional Considerations and WTO Compatibility

How do you regulate GHG emission reductions for products you consume that originate outside of your jurisdiction? How do you increase GHG quantification and transparency to begin with? This legislative proposal offers a roadmap. As described, member states in the coming years will be required to collect information regarding methane emissions associated with their imports, and that information will have to be disclosed. Ideally, this will create a “race to the top,” in which producers selling their product in the EU will strive to meet certain thresholds when it comes to methane emission measurement. The question of how the EC influences GHG emission reductions outside its jurisdiction may not be as unprecedented as it sounds.

First, there are other examples where EU regulatory standards effectively set the tone for regulatory standards elsewhere, which constitute a growing body of academic literature.[58]

Second, because implementation of this legislative proposal will take several years, it would be useful to consider how methane might fit into the EC’s carbon border adjustment mechanism (CBAM).[59] Under this policy, which was approved by the European Parliament on April 18, 2023, the EC mainly aims to prevent “carbon leakage,” i.e., companies moving away from the EU because GHG emission rules are more stringent than in other jurisdictions.[60] It is worth noting that initially CBAM will be applied to specific sectors where the risks of carbon leakage are deemed significant: cement, iron and steel, aluminum, fertilizers, electricity, and hydrogen.[61] If CBAM were extended to energy imports more broadly, some estimates have suggested that carbon border taxes of €3 billion per annum (about $3.32 billion) could be levied on imports of oil and natural gas from outside the continent.[62]

Whereas some suggest that imposing methane rules outside the EC’s jurisdiction may raise legal concerns, others have pointed out that, in fact, under the WTO there is legal precedent for countries to enact trade barriers for environmental ends, as long as the measures do not unfairly discriminate against foreign firms.[63] The EC is surely not asking more of importers of fossil energy than it is of its remaining domestic producers.

Conclusion

The European Union is on a regulatory mission to reduce emissions of methane from its domestic oil and natural gas industry. Moreover, across the continent, this industry is in long-term decline, and the strong interest in renewable and low greenhouse gas emission sources will accelerate this trend. However, European fossil fuel demand will not decrease as fast as its domestic production, according to all recent IEA analyses. Therefore, Europe is likely to become more dependent on imported fossil fuels in the coming decades, and the second part of the EU methane reduction proposal affecting such imports is truly where important methane emission reductions are to be achieved.

When the European Commission issued its legislative proposal on methane emission reduction in the energy sector on December 15, 2021, there was every expectation that this extension of its greenhouse gas reduction program would primarily affect its trade in natural gas with Russia, which had, over the years, evolved toward a monopoly-monopsony relationship. Perhaps anticipating an uphill struggle with a supplier with little interest in, and possibly a net beneficiary of, global warming, the EU adopted a slow, cautious data gathering approach. In the meantime, European importers rejected American supplies of liquefied natural gas on vague environmental grounds.[64]

The invasion of Ukraine by the Russian Federation in February 2022 changed everything. For the first time since the end of the Cold War, Europe found Russian armored formations at its doorstep. The close commercial ties that characterized the energy trade with Russia unraveled in a matter of months, while liquefied natural gas cargoes from Texas and Louisiana were rerouted to Europe—a massive shift of trade patterns.

Until the ramp-up of (among others) US LNG export facilities is complete in 2026,[65] Europe may well be scrambling for supplies. This interval coincides with the EC proposal as well as an expected strengthening of methane reduction rules in the US emanating from the Inflation Reduction Act of 2022[66] and the Environmental Protection Agency proposed rule on methane emission reduction from oil and natural gas operations.[67] Thus it is possible that the European desire to import fuels with reduced greenhouse gas footprints will be met not by Russian opacity but by American readiness to supply those fuels. However, the verdict is out whether policy makers will in fact move in synchrony to draft ambitious rules to curtail fugitive methane throughout oil and gas supply chains.

Appendix: Key chapters of the EC proposal, with a focus on fugitive methane emissions in the oil and gas sector (based on the original proposal)

Chapter 2—Competent authorities and independent verification

The EC expects member states to appoint competent authorities, who in turn will carry out periodic inspections to check the compliance of operators. Where relevant, these shall include site checks or field audits. In addition, there may be nonroutine inspections, e.g., to verify that leak repairs were carried out in full. If there is suspicion of a methane leak, anyone can lodge a written complaint to the competent authorities. This complaint should contain evidence of the alleged breach.

Once companies have submitted emission data, verifiers will assess the conformity of the submitted emission reports with the proposed regulation, with specific attention to the choice and employment of emission factors, methodologies, calculations, etc., ultimately leading to the determination of methane emissions, and risks of inappropriate reporting or measuring.

The European Commission may submit publicly available data to the IMEO, as made available to it by the competent authorities in the member states.

Chapter 3—Methane emissions in the oil and gas sector in the EU

Oil and gas operators must submit a report containing source-level methane emissions estimated using generic emission factors for all sources within 18 months of the regulation’s enactment. Within 24 months, operators will also need to submit a report containing quantification of source-level methane emissions for operated assets. Reporting at such level may involve the use of source-level measurement and sampling as the basis for establishing specific emission factors used for emission estimation. Then, within 36 months, and by May 31 every year thereafter, operators must submit a report containing quantification of source-level methane emissions from operated assets, complemented by measurements of site-level methane emissions, thereby improving the assessment. Also within 36 months, companies established in the EU must submit a report containing quantification of source-level methane emissions for non-operated assets, provided these have not been reported by an operator in response to another obligation. Finally, within 48 months, and by May 31 every year thereafter, companies established in the EU must submit a report containing quantification of source-level methane emissions for non-operated assets, complemented by site-level methane emissions, thereby allowing assessment and verification.

In addition to these reports, operators must submit a leak detection and repair (LDAR) program to the relevant authorities within nine months of the regulation’s enactment. And by 12 months, operators must carry out LDAR surveys. Thereafter, LDAR surveys will be completed with different frequencies depending on the component. In lieu of LDAR surveys, operators may choose to use continuous monitoring systems. Part of Article 14 details minimum detection limits of devices used by operators. Operators must repair or replace all components found to be leaking as soon as possible, but no later than five days for a first attempt after leak detection and 30 days for a complete repair. Offshore oil and gas wells at a depth greater than 700 meters are exempt from these obligations.

Venting will only be allowed in case of emergency or malfunction, and where unavoidable and strictly necessary for the operation, repair, or testing of components. Otherwise venting is prohibited. Routine flaring is also prohibited. Flaring will only be allowed where either reinjection, utilization on site, or dispatch of the methane to a market are not feasible for reasons other than economic considerations. Operators must include relevant information of all venting and flaring in their periodic reports.

Finally, within 12 months of enactment, member states will need to establish and make publicly available an inventory of all recorded inactive wells on their territory. Member states with more than 40,000 inactive wells, temporarily plugged wells, and permanently plugged and abandoned wells can submit a plan for completing the inventory and will have more time. The regulation details which inactive wells, temporarily plugged wells, and permanently plugged and abandoned wells will have to be monitored for methane leakage, and under what conditions they can be exempt.

Chapter 5—Methane emissions occurring outside of the EU

Within nine months of the regulation’s enactment, and by June 30 every year thereafter, importers must provide the information set out in Annex VIII (see below) to the competent authorities of member states. Furthermore, within 12 months, and by December 31 every year thereafter, member states must submit this information to the EC.

By December 2027, or earlier if available, the EC will examine the application of an article[68] within the original proposal that dealt with importer requirements, particularly the reporting of available methane emission data, methane emission data analysis by the IMEO, information on monitoring, reporting, verification of mitigation measures of non-EU operators from whom energy is imported, and security of supply and level playing field implications.

Within 18 months of enactment, the EC will establish and maintain a methane transparency database containing the aforementioned information. It shall also include a list of countries where fossil energy is produced and exported to the EU, relevant information on each of these countries as to their regulatory framework pertaining to methane emissions, and GHG regulations more broadly. This database will be publicly available online.

Within two years, the EC will establish a global methane monitoring tool based on satellite data and input from several certified data providers and services. This tool too shall be available to the public.

Chapter 6—Final provisions

The EC will assess the potential impact of the extension of the obligations concerning the measurement, quantification, monitoring, reporting, and verification of methane emissions as well as their abatement to importers of fossil fuels into the EU, identifying potential barriers, and proposing possible solutions with a view to reducing methane emissions while not impacting energy prices and security of supply. Based on that impact assessment, the EC will present a report to the European Parliament and the Council within 12 months of enactment, accompanied, if appropriate, by a legislative proposal to amend the Regulation.

Annex VIII

Annex VIII[69] of the proposal requires importers of oil and natural gas to provide the following information:

Whether the exporter is undertaking measurement and reporting of its methane emissions, either independently or as part of commitments to report national GHG inventories in line with UNFCCC requirements

Whether the exporter is in compliance with UNFCCC reporting requirements or in compliance with OGMP 2.0 standards. This must be accompanied by a copy of the latest report on methane emissions. The method of quantification (such as UNFCCC tiers or OGMP levels) employed in the reporting must be specified for each type of emission.

Exporters of oil and gas must specify the regulatory or voluntary measures used to control their methane emissions, including measures such as leak detection and repair surveys or measures to control and restrict venting and flaring of methane. This must be accompanied by a description of such measures, including, where available, reports from leak detection and repair surveys and from venting and flaring events from the last available calendar year.

[11] Zachmann et al., “European Natural Gas Imports,” Figure 4.

[12] Pietro Lombardi, “The EU Will Ban Russian LNG ‘Sooner than Later,’ Spain’s Energy Minister Says,” Reuters, May 17, 2023, https://www.reuters.com/business/energy/eu-will-ban-russian-lng-sooner-than-later-spains-energy-minister-says-2023-05-16/.

[17] Chi Xu, Timothy A. Kohler, Timothy M. Lenton, and Martin Scheffer, “Future of the Human Climate Niche,” Proceedings of the National Academy of Sciences 117, no. 21 (May 2020): 11350–11355, https://www.pnas.org/doi/full/10.1073/pnas.1910114117.

[18] Thane Gustafson, Klimat: Russia in the Age of Climate Change (Cambridge, Massachusetts: Harvard University Press, 2021), chap. 7.

[22] Halley L. Brantley et al., “Assessment of Methane Emissions from Oil and Gas Production Pads Using Mobile Measurements,” Environmental Science and Technology 48, no. 24 (November 2014): 14508–14515, Fig. 5,

[23] Daniel H. Cusworth et al., “Intermittency of Large Methane Emitters in the Permian Basin,” Environmental Science and Technology Letters 8, no. 7 (June 2021): 567–573, https://pubs.acs.org/doi/10.1021/acs.estlett.1c00173.

[24] UNFCCC, “Parties to the United Nations Framework Convention on Climate Change,” October 25, 2022,

[25] Ramón A. Alvarez et al., “Assessment of Methane Emissions From the U.S. Oil and Gas Supply Chain,” Science 361, no. 6398 (June 2018): 186–188, https://www.science.org/doi/10.1126/science.aar7204; Jeffrey S. Rutherford et al., “Closing the Methane Gap in US Oil and Natural Gas Production Emissions Inventories,” Nature Communications 12 (August 2021): 4715, https://doi.org/10.1038/s41467-021-25017-4; Matthew R. Johnson et al., “Comparisons of Airborne Measurements and Inventory Estimates of Methane Emissions in the Alberta Upstream Oil and Gas Sector,” Environmental Science and Technology 51, no. 21 (October 2017): 13008–13017, https://pubs.acs.org/doi/10.1021/acs.est.7b03525; Stuart N. Riddick and Denise L. Mauzerall, “Likely Substantial Underestimation of Reported Methane Emissions from United Kingdom Upstream Oil and Gas Activities,” Energy & Environmental Science 16 (January 2023): 295–304,

[30] Matthew Johnson et al., “Application of Airborne LiDAR Measurements to Create Measurement-Based Methane Inventories in the Canadian Upstream Oil & Gas Sector,” American Geophysical Union 2021 Fall Meeting, https://agu.confex.com/agu/fm21/meetingapp.cgi/Paper/996598.

[31] Daniel Zavala-Araiza et al., “A Tale of Two Regions: Methane Emissions from Oil and Gas Production in Offshore/Onshore Mexico,” Environmental Research Letters 16, no. 2 (January 2021): 024019, https://doi.org/10.1088/1748-9326/abceeb.

[32] Evan D. Sherwin, Yuanlei Chen, Arvind P. Ravikumar, and Adam R. Brandt, “Single-Blind Test of Airplane-Based Hyperspectral Methane Detection via Controlled Releases,” Elementa 9, no. 1 (March 2021), https://doi.org/10.1525/elementa.2021.00063.

[33] Kleinberg, “Methane Emissions from the Fossil Fuel Industries of the Russian Federation.”

[34] Jonathan Elkind et al., “Nowhere to Hide: Implications for Policy, Industry, and Finance of Satellite-Based Methane Detection,” Center on Global Energy Policy, October 14, 2020, https://www.energypolicy.columbia.edu/publications/nowhere-hide-implications-policy-industry-and-finance-satellite-based-methane-detection/.

[35] Halff, Kleinberg, and Mitrova, “Russia’s Methane Emissions and the War in Ukraine.”

[36] Steven Mufson et al., “Russia Allows Methane Leaks at Planet’s Peril,” Washington Post, October 19, 2021,

[41] Lu Shen et al., “Satellite Quantification of Oil/Gas Methane Emissions in the US and Canada Including Contributions from Individual Basins,” Atmospheric Chemistry and Physics 22, no. 17 (September 2022): 11203–11215, Supplementary Information Table S1, https://doi.org/10.5194/acp-22-11203-2022.

[42] Robert L. Kleinberg, “Reducing Emissions of Methane and Other Air Pollutants from the Oil and Natural Gas Sector: Recommendations to the Environmental Protection Agency,” Environmental Protection Agency, July 6, 2021, https://www.regulations.gov/comment/EPA-HQ-OAR-2021-0295-0035.

[50] Cahill, “What’s Next for Oil and Gas Methane Regulations.”

[51] Council of the European Union, Proposal for a Regulation of the European Parliament and of the Council on Methane Emissions Reduction in the Energy Sector and Amending Regulation (EU) 2019/942—General Approach, December 15, 2022, section 66A, https://data.consilium.europa.eu/doc/document/ST-16043-2022-INIT/en/pdf.

[57] European Parliament, “Fit for 55: MEPs Boost Methane Emission Reductions from the Energy Sector,” press release, May 9, 2023, https://www.europarl.europa.eu/news/en/press-room/20230505IPR84920/fit-for-55-meps-boost-methane-emission-reductions-from-the-energy-sector.

[58] Anu Bradford, The Brussels Effect: How the European Union Rules the World (New York: Oxford University Press, 2020).

[68] Council of the European Union, Proposal for a Regulation of the European Parliament and of the Council on Methane Emissions Reduction in the Energy Sector and Amending Regulation (EU) 2019/942—General Approach, p. 47.

This analysis provides an overview of changes in production and economic outcomes in US oil and gas regions, grouping them by recent trends and examining their impact on local economies.

Rapidly reducing greenhouse gas emissions from fossil fuels to address the severe threats of climate change requires economic transformations that pose challenges for regions heavily dependent on coal, oil, natural gas, or other carbon-intensive industries.

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece...