Trump is frustrated gasoline prices don’t mirror oil’s decline. Experts say it’s not that simple

U.S. gasoline prices decreased an average of 49 cents a gallon in the last month as expectations rose for an end to the war with Iran.

Get the latest as our experts share their insights on global energy policy.

This Energy Explained post represents the research and views of the author(s). It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

The energy transition is in the midst of its own transition. Spiking electricity demand and geopolitical events are driving up energy prices, while debates over the best sources...

Commentary by Robin Mills & Ahmed Mehdi • February 15, 2023

This commentary represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. More information is available at Our Partners. Rare cases of sponsored projects are clearly indicated.

It has been over two months since the European Union (EU) ban on Russian crude oil[i] entered into force, triggering friction in oil markets and petroleum supply chains. The ban takes effect against major uncertainties, especially the speed and size of recovery in Chinese demand and the global economic outlook. Three key players each have decisions to make in response: Will the EU and US impose further restrictions on Russian oil (in addition to the price cap now in force for more than two months and the product ban that came into effect on February 5)? Will Russia be able and willing to redirect all or most flows from Europe to Asia in the face of the G7-inspired price cap and EU insurance ban? How will the oil policies of the Organization of the Petroleum Exporting Countries (OPEC), the group with 10 additional oil exporters (known as OPEC+), and Saudi Arabia evolve in response?

The Middle East, as the world’s key oil-exporting region and leader, remains central to the market’s reaction and outcomes. This three-part series covers crude oil (this commentary), refined oil products (Part 2) and geopolitical implications (Part 3) to understand the impact of the war on oil flows and pricing since February 2022 and to extract clues to the future reactions of exporters, traders, and refiners.

Six key conclusions emerge for crude oil:

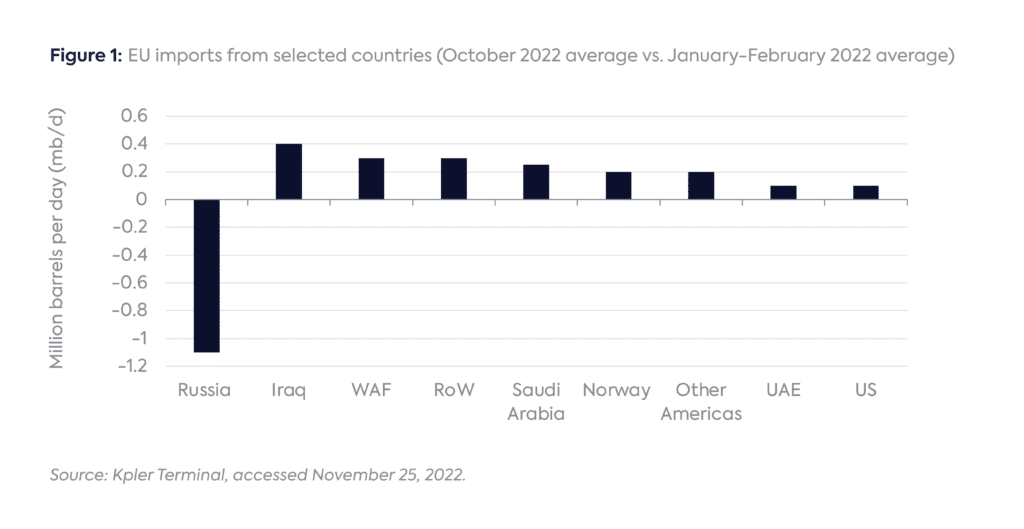

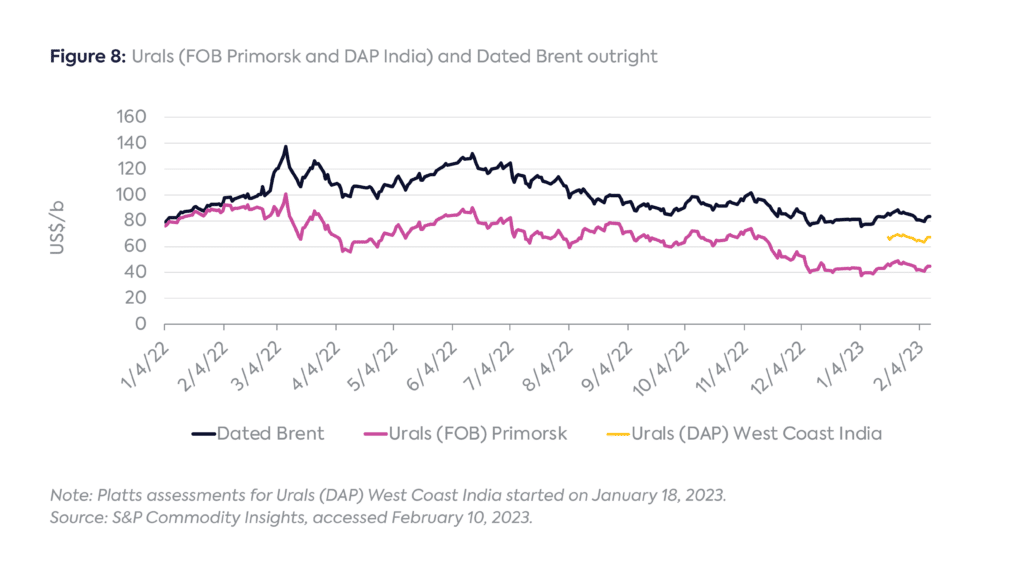

Prior to Russia’s invasion of Ukraine on February 24, 2022, Urals[ii]—Russia’s key crude export grade—served as a baseload for Europe’s refineries, with Russian crude historically making up around 20 percent of Europe’s crude diet. Prior to the EU’s December 2022 ban, refiner self-sanctioning played a significant role in driving down Russia’s exports to Europe. Between March and November 2022, Russian crude exports to the EU averaged approximately 1.78 million barrels per day (Mb/d), roughly 0.7 Mb/d lower than the January–February 2022 (preinvasion) average and 0.3 Mb/d lower than the 2021 average.

During 2022, as a replacement, the EU turned to a variety of sources, particularly the Middle East, West Africa, the US, and Norway. The role of West African producers, such as Nigeria, as “swing” players (given their ample spot liquidity and destination-free status) enabled traders to redirect their volumes to Europe flexibly; likewise, Norway’s Johan Sverdrup, a key Atlantic grade that was previously often exported to China, is now staying local to be bid on by European refiners, as the medium-sour grade is a healthy substitute for Urals.[iii] The EU’s overall crude intake actually increased with ongoing demand recovery and higher runs on the back of strong middle distillate refining margins.

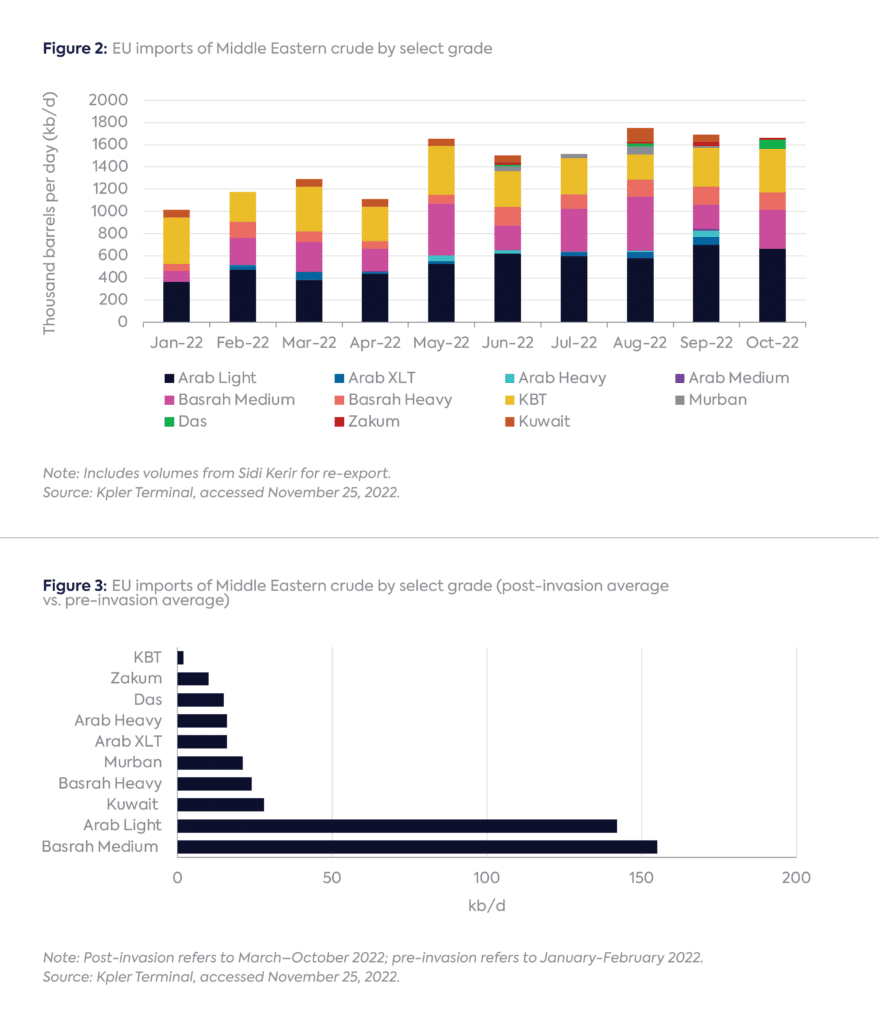

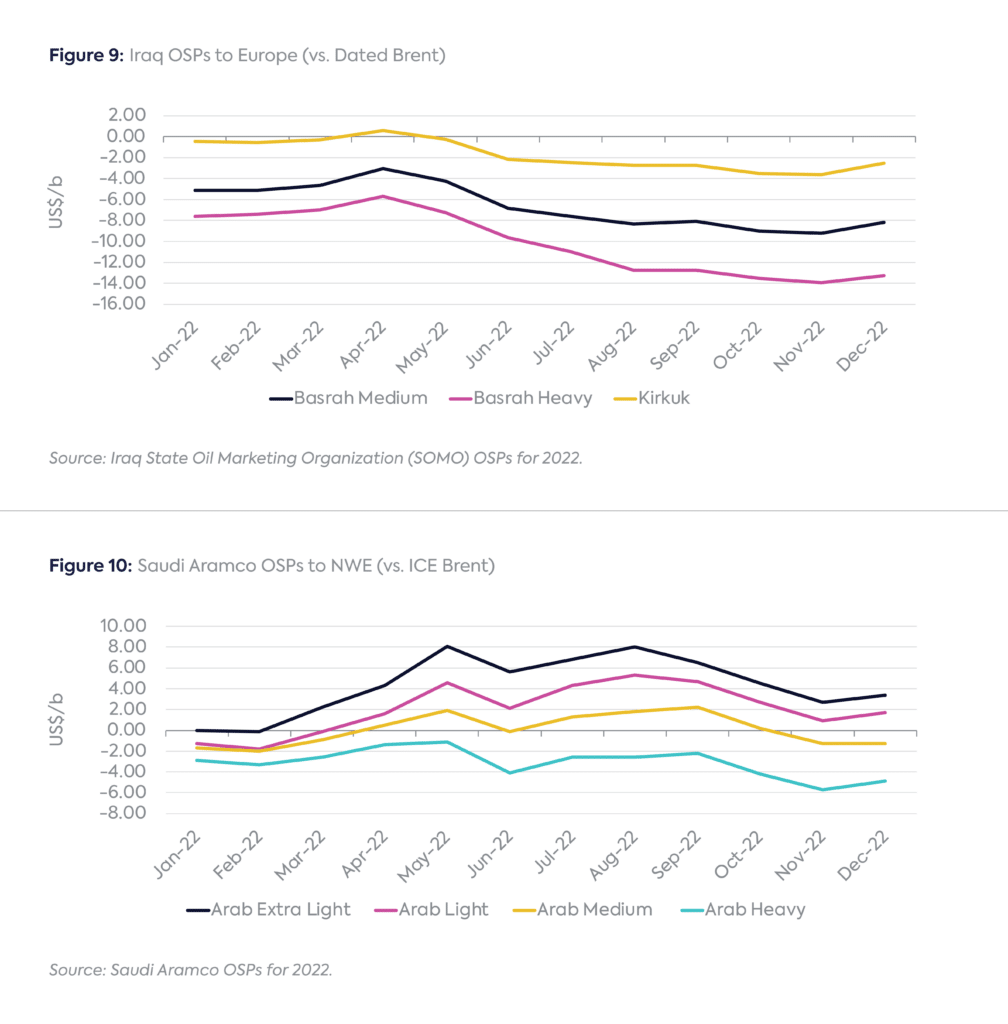

Among the key Middle Eastern players, Iraq and Saudi Arabia have made the biggest inroads, primarily via their grades of Basrah Medium[iv] and Arab Light,[v] respectively (see Figures 3 and 4). Although not an exact match for Urals, Arab Light in particular has benefited from a higher yield of diesel and lower fuel oil yield (see below). Production targets under the OPEC+ agreement[vi] (grouping OPEC, Russia, and several other non-OPEC states) steadily increased between May 2021 and when the cuts were introduced in October and November 2022.[vii] Kurdish Blend Test (KBT),[viii] exported by the Kurdistan Region of Iraq, has made the least inroads, partly due to internal Iraqi politics[ix] and partly because of competition from Russian crude in the Mediterranean, which will ease now that the EU ban is in force.

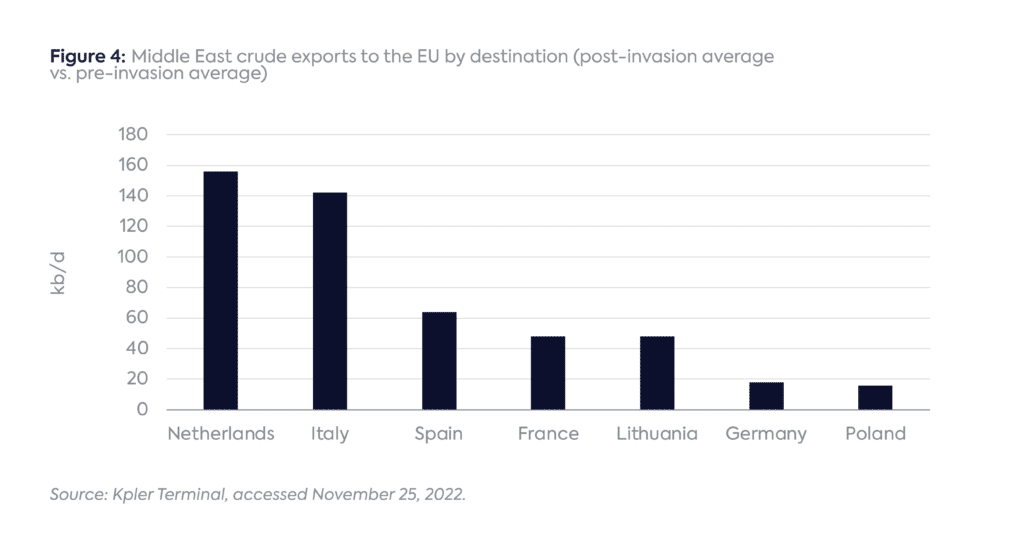

As Figure 4 shows, the largest markets where Middle Eastern crude has increased market share are Italy, the Netherlands, Lithuania, and Poland—the latter a country of strategic focus for Saudi Aramco, which has expanded its downstream footprint there in recent years.[x] Iraq, which supplied around 600 kb/d of crude under term contracts to Europe prior to the invasion, has also increased market share in Italy, particularly with Italian refiner Saras, a major term client of Iraq’s State Oil Marketing Organisation (SOMO).[xi] An additional outlet for Middle Eastern crude in Italy may reopen when the status of the ISAB refinery in Sicily, owned by Russian company Lukoil, is resolved. ISAB ramped up its purchases of Russian crude following the start of the war, but after the Italian government intervened to assure continuity of supply following the EU ban, ISAB was sold to a private equity group backed by the trading company Trafigura.[xii]

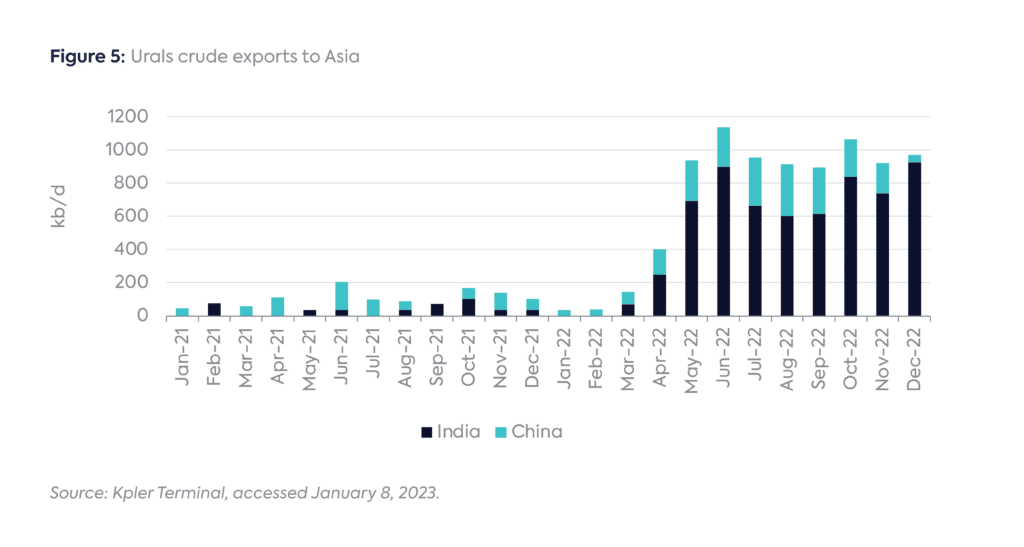

The increases in Saudi and Iraqi exports to Europe were driven not only by the easing of OPEC+ cuts throughout 2022 but also by the displacement effect of increased Russian Urals heading to Asia since the outbreak of the war (see Figure 5).

This redirection of Urals to Asia has had numerous effects on Middle Eastern players, most importantly:

Since the EU embargo on Russian seaborne crude imports, most Russian crude entering Europe has been via pipeline (estimated to be around 700 kb/d) in addition to a small amount of seaborne volume (around 200 kb/d to Bulgaria, the only country allowed to import seaborne volumes until the end of 2024). Of the 700 kb/d currently transiting the Druzhba pipeline, about 0.3–0.5 Mb/d can continue under exemptions to central/southeast European countries, such as Hungary, that argue they lack access to alternatives. Germany and Poland have agreed not to use the northern leg of the Druzhba pipeline, which runs through Belarus (avoiding Ukraine), for Russian crude despite the exemptions,[xx] though they have sought to deliver Kazakh crude through Druzhba (potential transactions that Russia will probably find ways to prevent).[xxi] From a 2021 average of 2.1m b/d of crude imports from Russia, going forward, Europe will now likely take in only around 300-400 kb/d of Russian crude – a dramatic drop.

The EU/G7’s price cap on Russian crude, which is set at $60/b, came into effect in early December 2022.[xxii] The workability of the cap—akin to a Western-imposed OSP on Russian crude—is already being questioned, however. This is not surprising. Even prior to its introduction, the cap faced numerous obstacles: differences between the US and EU over where the cap should be set; how it will be policed given that over-the-counter trade transactions are “off the books”; the fact that it is not dynamic[xxiii] (meaning it does not move automatically with the flat price or shifts in crude differentials and benchmark values, though it can be adjusted over time by further decisions[xxiv]); and which of a growing number of potential exemptions should be granted.

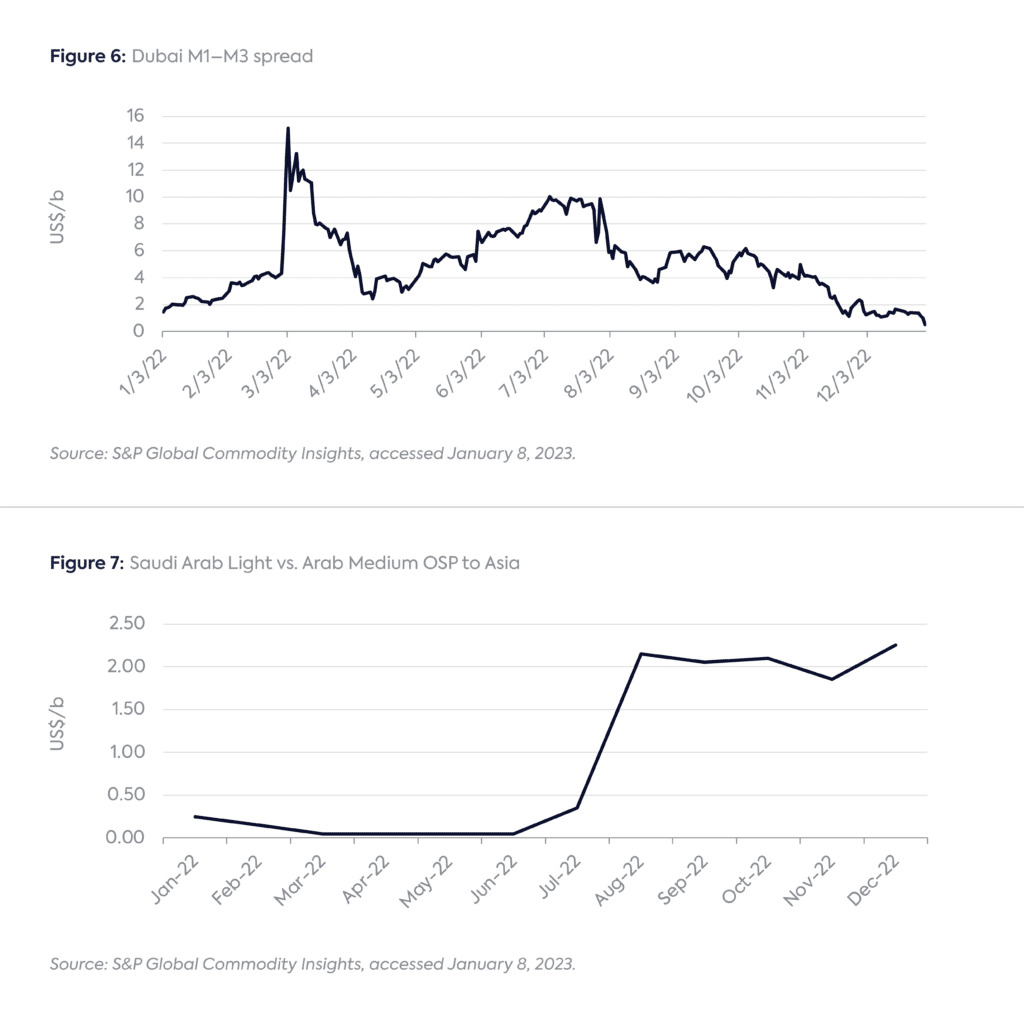

The spread between the price cap and the outright price of Urals in the market has also been influenced by a range of factors: set the cap too low and Russia will lack any incentive to participate, raising the risk of unilateral cuts; set the price too high and the cap becomes redundant, acting simply as a nondynamic OSP that fails to deprive the Kremlin of revenue while making oil supply chains less efficient and even reducing the current discounts that customers are demanding. The workability of the price cap is also indirectly influenced by OPEC+ policy. By protecting an implicit floor price, Saudi Arabia has made it difficult for the West to introduce a price cap far below that level, as such a move changes the “price cap band”: a price cap too far below OPEC+’s implied floor price of circa USD $80/b[xxv] will increase the risk of unilateral cuts by Russia. It is also worth noting that Russian crude sales to Asia are on a delivered rather than a free on board (FOB) basis—a situation that the price cap pricing basis does not entirely capture, given that delivered pricing terms between buyer and seller remain opaque and difficult to capture (e.g., payment terms, pricing terms, and shipping costs).

For now, the disputes over the principle and practicalities of a cap mean that it appears watered down to the point of ineffectiveness. However, the mere existence of such a mechanism could be concerning for both Russia and OPEC+. It is too early to make a call on the effectiveness of the price cap; however, as pressures grow on Russia’s supply chain, Russia will face a choice between “self-sanctioning” by cutting exports deliberately, as announced on February 10, 2023 (by 500 kb/d), avoiding the cap (at a higher cost and eventually with some unavoidable loss of exports), or accepting the principle. Though it would recoup part if not all of the cost of a voluntary export cut in higher prices—how much would depend critically on the response of its OPEC+ colleagues—if and when it accepted the principle of a price cap even tacitly, and if a cap that is set “too high” (i.e., at or above current discounted Russian prices) operates without major market disruption, the G7 would have the option to lower the cap and/or tighten enforcement.[xxvi]

Saudi Arabia would also be very wary of an effective price cap, which it fears might one day be turned against it or other OPEC+ members in a kind of “buyers’ cartel,” or even as a way to capture rents in a climate-conscious world with long-term shrinking oil demand.

Clearly, the Middle East’s importance is growing in the current market. The gross quantity the Middle East produces and exports is crucial. But beyond that, decisions on target markets, pricing, and crude trade will be influential in determining how effective sanctions are and how much pain Europe and key Asian markets suffer in the process.

As Russia now gears to shift yet more of its crude east, there are six key strategic issues to watch for in the region:

For now, the Middle East crude exporters have gained overall from the Russia shock, mainly via higher prices. They have adapted to new competition, moderate loss of market share in India has been compensated for by higher sales to Europe, OSPs have shown increase, and Middle East players themselves can benefit from using, refining, and trading Russian oil. Iran is probably the exception because of the greater competition in its only remaining sizeable market, China, although it has managed to boost exports recently.

However, the more stringent measures on Russia have not yet shown their full effect. As the situation drags on, the Russian position in OPEC+ could become a burden by, for instance, preventing the organization from increasing output targets even as its own exports drop. Competition from Russian barrels in Asia complicates pricing for Asian term clients as discounted Russian crude puts pressure on spot valuations. Setting optimal OSPs to maximize pricing while defending market share has become trickier. All of this could very well give rise to Saudi-Russian tensions, or at least to Saudi Arabia’s prized oil market flexibility being compromised by the need to accommodate Moscow. As Russia and Saudi production profiles diverge over time, OPEC+ power relations will likely shift, opening a potentially new chapter for the organization.

[i] European Council, “EU Sanctions against Russian Explained,” January 18, 2023, https://www.consilium.europa.eu/en/policies/sanctions/restrictive-measures-against-russia-over-ukraine/sanctions-against-russia-explained/.

[ii] Urals is a blend of crude oils from many Russian fields. It is classified as a medium-gravity sour crude, with an American Petroleum Institute (API) gravity of 31.5° and sulfur content of 1.44 percent. S&P Global, “Specifications Guide Europe and Africa Crude Oil,” July 2022, https://www.spglobal.com/commodityinsights/plattscontent/_assets/_files/en/our-methodology/methodology-specifications/emea-crude-methodology.pdf.

[iii] Johan Sverdrup (28° API, 0.8 percent sulfur): Michael Carolan, “Johan Sverdrup Emerges as Potential Benchmark Saviour,” Argus Media, June 14, 2021, https://www.argusmedia.com/en/news/2224380-johan-sverdrup-emerges-as-potential-benchmark-saviour. Phase 2 of the field started production in mid-December, with plateau production expected to reach 720 kb/d.

[iv] 28° API, 3.67 percent sulfur; S&P Global, “Specifications Guide Europe and Africa Crude Oil,” July 2022, https://www.spglobal.com/commodityinsights/plattscontent/_assets/_files/en/our-methodology/methodology-specifications/emea-crude-methodology.pdf.

[v] 33° API, 1.77 percent sulfur; S&P Global, “Specifications Guide Europe and Africa Crude Oil,” July 2022, https://www.spglobal.com/commodityinsights/plattscontent/_assets/_files/en/our-methodology/methodology-specifications/emea-crude-methodology.pdf.

[vi] OPEC, “Declaration of Cooperation,” 2022, https://www.opec.org/opec_web/en/publications/4580.htm.

[vii] Sam Meredith, “OPEC+ to Cut Oil Production by 2 Million Barrels per Day to Shore Up Prices, Defying U.S. Pressure,” CNBC, October 5, 2022, https://www.cnbc.com/2022/10/05/oil-opec-imposes-deep-production-cuts-in-a-bid-to-shore-up-prices.html.

[viii] “Iraq Restarts Kirkuk Crude Flows through KRG Pipeline,” Argus Media, November 16, 2018, https://www.argusmedia.com/en/news/1794182-iraq-restarts-kirkuk-crude-flows-through-krg-pipeline.

[ix] In February 2022, the Iraqi Federal Supreme Court ruled that the Kurdistan Regional Government’s (KRG) oil and gas law was unconstitutional, depriving it of the right to manage its upstream oil sector and sell oil independently. Although this ruling does not have an immediate practical effect, it may deter some European refiners from lifting KBT, which could put their existing crude purchase contracts with federal (non-KRG) Iraq at risk. See https://www.gibsondunn.com/recent-iraqi-supreme-court-decision-likely-to-trigger-investment-arbitration-claims/.

[x] Fareed Rahman, “Saudi Aramco Completes New Oil Deals with Poland’s PKN Orlen,” The National, November 30, 2022, https://www.thenationalnews.com/business/energy/2022/11/30/saudi-aramco-completes-new-oil-deals-with-polands-pkn-orlen/.

[xi] Zhiyuan Li, “Saras Refinery Runs Lower 15% q/q, Likely to Miss Q3 Guidance,” Kpler, November 9, 2021, https://www.kpler.com/blog/saras-refinery-runs-lower-15-q-q-likely-to-miss-q3-guidance.

[xii] Reuters, “Italy Set to Nationalise Lukoil Refinery—Paper,” November 29, 2022, https://www.reuters.com/business/energy/italy-set-nationalise-lukoil-refinery-paper-2022-11-29/; Julia Payne and Giuseppe Fonte, “Russia’s Lukoil Reaches Deal to Sell Italian Refinery,” Reuters, January 9, 2023, https://www.reuters.com/business/energy/trafigura-with-consortium-agrees-buy-lukoils-isab-refinery-sources-2023-01-09/.

[xiii] Ministry of Petroleum and Natural Gas, “Total 23 Refineries Working in the Country with Refining Capacity of 249.22 Million Metric Tons per Annum,” February 10, 2022, https://pib.gov.in/PressReleaseIframePage.aspx?PRID=1797261.

[xiv] Quotas in the latest round were increased to the highest level since the first round of 2021, but most of these go to five state-owned companies; only one private player, Zhejiang Rongsheng Petrochemical, receives export allowances. Shi Weijun, “Markets Await Chinese Product Export Quotas,” Petroleum Economist, October 24, 2022, https://pemedianetwork.com/petroleum-economist/articles/trading-markets/2022/markets-await-chinese-product-export-quotas/.

[xv] Bloomberg, “New Oil Traders Fill Void as Top Names Abandon Moscow Ties,” May 17, 2022, https://www.bloomberg.com/news/articles/2022-05-17/new-oil-traders-fill-the-void-as-top-names-abandon-moscow-ties?sref=uK5WXUhK.

[xvi] Florence Tan, “Sinopec Plans to Extend Cuts in Saudi Crude Oil Imports to June, July: Officials,” Reuters, April 25, 2018, https://www.reuters.com/article/us-china-oil-sinopec-corp/sinopec-plans-to-extend-cuts-in-saudi-crude-oil-imports-to-june-july-officials-idUSKBN1HW18Z.

[xvii] Florence Tan and Nidhi Verma, “UPDATE 3—Saudi to Supply Full June Crude Volumes to Most Buyers in Asia—Sources,” Reuters, May 11, 2021, https://www.reuters.com/article/saudi-asia-oil-idAFL1N2MY07I.

[xviii] Market News, “ADNOC to Cut 5% of Crude Volumes to Term-Lifters for December,” November 28, 2022, https://marketnews.com/adnoc-to-cut-5-of-crude-volumes-to-term-lifters-for-december.

[xix] S&P Global, “Platts Dubai/Oman Benchmarks,” February 2021, https://www.spglobal.com/commodityinsights/plattscontent/_assets/_files/en/our-methodology/methodology-specifications/dubai_oman_benchmarks_faq.pdf.

[xx] Reuters, “Poland, Germany Seek EU Sanctions on Russian Druzhba Oil Pipeline,” November 27, 2022, https://tribune.com.pk/story/2388425/poland-germany-seek-eu-sanctions-on-russian-druzhba-oil-pipeline.

[xxi] Julian Lee, “Germany’s Pivot to Piped Kazakh Oil Looks Like a Pipe Dream,” Bloomberg, December 21, 2022, https://www.bloomberg.com/news/articles/2022-12-21/germany-s-pivot-to-piped-kazakh-oil-looks-like-a-pipe-dream.

[xxii] Edward Fishman, “How the Price Cap on Russian Oil Will Work in Practice,” Center on Global Energy Policy, November 30, 2022, https://www.energypolicy.columbia.edu/publications/how-price-cap-russian-oil-will-work-practice/.

[xxiii] Jan Cienski, “Watch Out for Next Winter, Energy Chief Warns Europe,” Politico, November 30, 2022, https://www.politico.eu/article/fatih-birol-warning-energy-winter-europe/.

[xxiv] Reuters, “Russian Oil Price Cap Can Be Adjusted to Market Developments—EU Head,” December 2, 2022, https://www.reuters.com/business/energy/russian-oil-price-cap-can-be-adjusted-market-developments-eu-head-2022-12-02/.

[xxv] Or, indeed, the US’s implied floor for Strategic Petroleum Reserve refilling of $70/b (for West Texas Intermediate, trading as of late January 2023 at about $7/b below ICE Brent).

[xxvi] European Commission, “Questions and Answers: G7 Agrees Oil Price Cap to Reduce Russia’s Revenues, while Keeping Global Energy Markets Stable,” December 3, 2022, https://ec.europa.eu/commission/presscorner/detail/en/QANDA_22_7469.

[xxvii] Net global refining capacity will expand by 1.6 Mb/d in 2023, according to the International Energy Agency, including 140 kb/d at Karbala (Iraq), 230 kb/d at Duqm (Oman), and 135 kb/d at Visakha (India). Several large, new refineries in China should come online in 2024. Insights Global, “EIA: New Refineries Will Increase Global Refining Capacity in 2022 and 2023; China Leads,” July 28, 2022, https://www.insights-global.com/eia-new-refineries-will-increase-global-refining-capacity-in-2022-and-2023-china-leads/; International Energy Agency Oil Market Report, December 15, 2022, https://www.iea.org/reports/oil-market-report-december-2022.

[xxviii] For example, this study, concluded in 2019 before COVID-19 and the war, was already quite negative on Russia’s ability to maintain production levels beyond 2030: Nikita O. Kapustin and Dmitry A. Grushevenko, “A Long-Term Outlook on Russian Oil Industry Facing Internal and External Challenges,” Oil & Gas Science and Technology Revue, IFP Energies Nouvelles, 74, no. 72 (September 13, 2019), https://ogst.ifpenergiesnouvelles.fr/articles/ogst/full_html/2019/01/ogst190118/ogst190118.html.

[xxix] The measure of the gross profit from refining one barrel of reference crude into one barrel of product.

[xxx] The authors would like to thank Steve Sawyer, refining specialist at Facts Global Energy, for this point.

[xxxi] Julian Lee and Anthony Di Paola, “Russia Delivers First Crude Cargo to UAE’s Ruwais Refinery,” Bloomberg, November 14, 2022, https://www.bloomberg.com/news/articles/2022-11-14/russia-delivers-first-crude-cargo-to-uae-s-ruwais-refinery.

[xxxii] See https://www.adnoc.ae/en/our-projects/crude-flexibility.

[xxxiii] International Energy Agency Oil Market Report, December 15, 2022, https://www.iea.org/reports/oil-market-report-december-2022.

[xxxiv] Ibid.

[xxxv] Salma El Wardany and Verity Ratcliffe, “Libya’s Crude Oil Exports Drop Sharply after Key Ports Halt,” Bloomberg, July 1, 2022, https://www.bloomberg.com/news/articles/2022-07-01/libya-s-crude-oil-exports-drop-sharply-after-key-ports-halt.

[xxxvi] Libby George, “Nigeria’s Oil Output at 32-Year Low as Thieves Hobble Output,” Reuters, September 9, 2022, https://www.reuters.com/business/energy/nigerias-oil-output-drops-below-1-mln-bpd-2022-09-09/.

[xxxvii] Joshua Askew, “Iran Protests: What Caused Them? Are They Different This Time? Will the Regime Fall?,” Euronews, December 20, 2022, https://www.euronews.com/2022/11/25/iran-protests-what-caused-them-who-is-generation-z-will-the-unrest-lead-to-revolution.

The White House declared last week that President Trump finally "broke OPEC" after the United Arab Emirates withdrew from the cartel.

Full report

Commentary by Robin Mills & Ahmed Mehdi • February 15, 2023