Israel-Iran Energy War Disrupts Global LNG Supply for Years

Qatars LNG Facility Damage Forces 3-5 Year Repair, Contract Cancellations Attacks on Ras Laffan disrupt global supply, triggering force majeure on con

Current Access Level “I” – ID Only: CUID holders, alumni, and approved guests only

Get the latest as our experts share their insights on global energy policy.

On February 28, the US and Israel launched new attacks on Iran targeting primarily the country's leadership, security forces, and missile program.

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

As the conflict in the Middle East enters its 20th day, events on the ground have shifted into a critical new phase marked by direct strikes on core...

Find out more about our upcoming and past events.

This roundtable is open only to currently enrolled Columbia University students. To register, you must sign in with your UNI. The Center on Global Energy Policy (CGEP) at...

Commentary by Ahmed Mehdi & Tom Moerenhout • September 20, 2023

This commentary represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. More information is available at Our Partners. Rare cases of sponsored projects are clearly indicated.

It has now been just over a year since the US Congress signed into law the Inflation Reduction Act (IRA). Already, the IRA has been followed by more than US $110 billion in clean energy investments,[i] with just over $70 billion earmarked for the US battery supply chain,[ii] particularly downstream cell projects (so-called gigafactories).

The first part of this series examined the key drivers behind the adoption of the IRA, concluding that the bill attempts to de-risk investment in battery supply chains while reducing reliance on China, and that implementation will need to balance these objectives to be successful in increasing investment and electric vehicle (EV) deployment simultaneously. This second installment focuses on the workings of the IRA one year on. Specifically, it describes the key supply and demand incentives offered by the bill, assesses the impact of IRA supply-side policies on US battery economics to date, and examines the demand-side provisions of the IRA, which include notable eligibility constraints on the origins of battery components and critical minerals.

The commentary concludes that the IRA has already radically altered the US battery cost curve and ushered in a new chapter for the battery industry: a wave of mergers and acquisitions activity focused on free trade agreement (FTA)–compliant jurisdictions (particularly for lithium). It also notes, however, that the availability of IRA-compliant minerals and the pace of US EV adoption will heavily depend on the contours of the upcoming Treasury Department definition of China as a Foreign Entity of Concern (FEOC). The final details of FEOC implementation are still under consideration at the time of writing.

The IRA has a direct impact on US battery economics via credits intended to spur supply-side activity and demand-side procurement behavior. On the supply side, as with other energy transition projects, project developers can choose between an investment tax credit (the 48C credit) and a production tax credit (the 45X credit).

On the demand side, the US government offers clean vehicle tax credits that incentivize EV purchases by individual consumers (the 30D credit) as well as by commercial fleet operators (the 45W credit). Whereas the commercial fleet EV purchasing credit does not have any local content requirements for its components and minerals, the clean vehicle credit for individual consumers does.

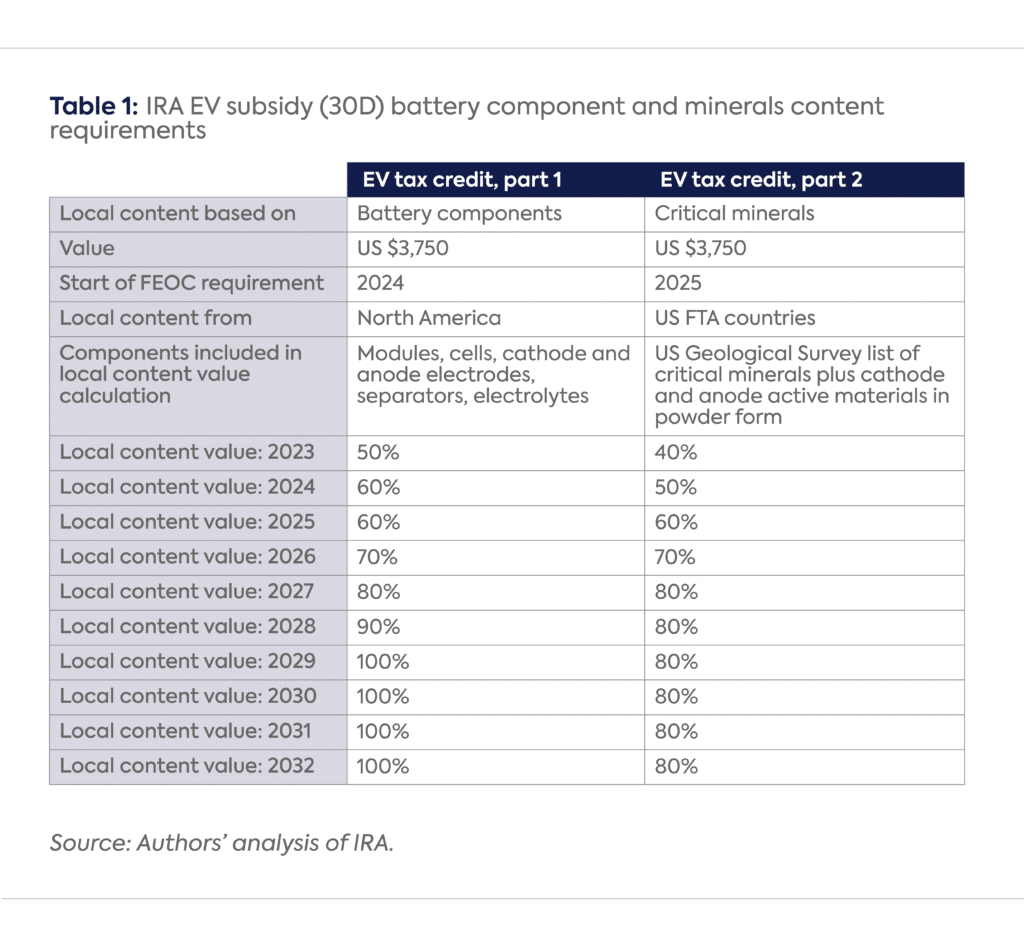

A total tax credit of $7,500 is available for purchases of full battery electric cars and plug-in hybrid electric vehicles that meet certain local content criteria related to the origin of the critical minerals in the batteries ($3,750 credit) and the components used in the batteries (another $3,750 credit). It is possible for eligible vehicles to qualify for only one of the two credits. Purchasers can transfer the tax credit amount to retailers and receive the credit amount as a direct reduction of the cost of the vehicle.

The impact of the IRA’s Advanced Manufacturing Production Tax Credit (AMPTC) and Advanced Energy Project Investment Tax Credit (AEPITC) has been substantial. This is not surprising. In 2022, the cost of producing a high-performance nickel-cobalt-manganese (NCM 811) battery cell in the US was around $135/kWh. For lithium-iron-phosphate cells (LFP), the cost averaged around $125/kWh.[v] In short, these credits introduce discounts of more than 30 percent for manufacturers, which is nothing short of a game-changer.

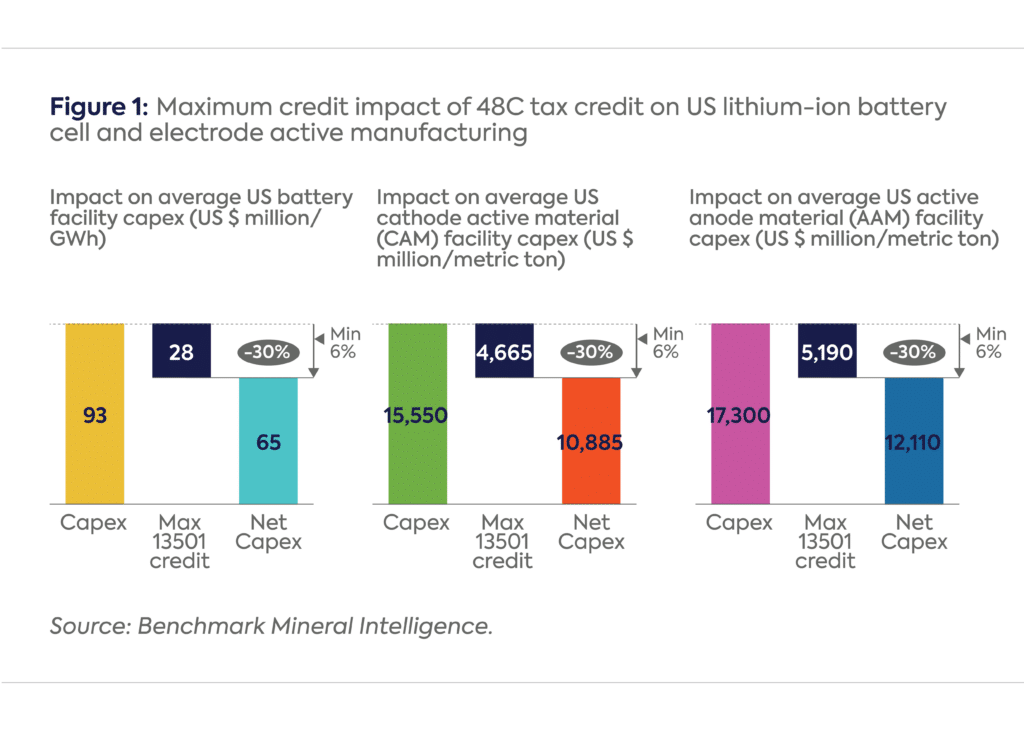

The investment tax credit shows just how much the IRA is affecting the global competitiveness of US-based battery cell manufacturing (see Figure 1). The capital expenditure (capex) needed to develop gigafactories varies significantly by region, with capex intensity in the US averaging around $90 million per gigawatt-hour (GWh), almost one-third higher than the average capex intensity in China, which lies around $60 million/GWh.[vi] At its maximum, including labor requirements, the investment tax credit reaches 30 percent, thereby helping bridge the capex gap with China. While China still holds a dominant position in raw material access and technology licensing, and newer cell entrants outside China continue to grapple with the realities and challenges of cell manufacturing (e.g., yield losses, labor shortages, thin margins), the tax credits do significantly increase the competitiveness of US gigafactories.

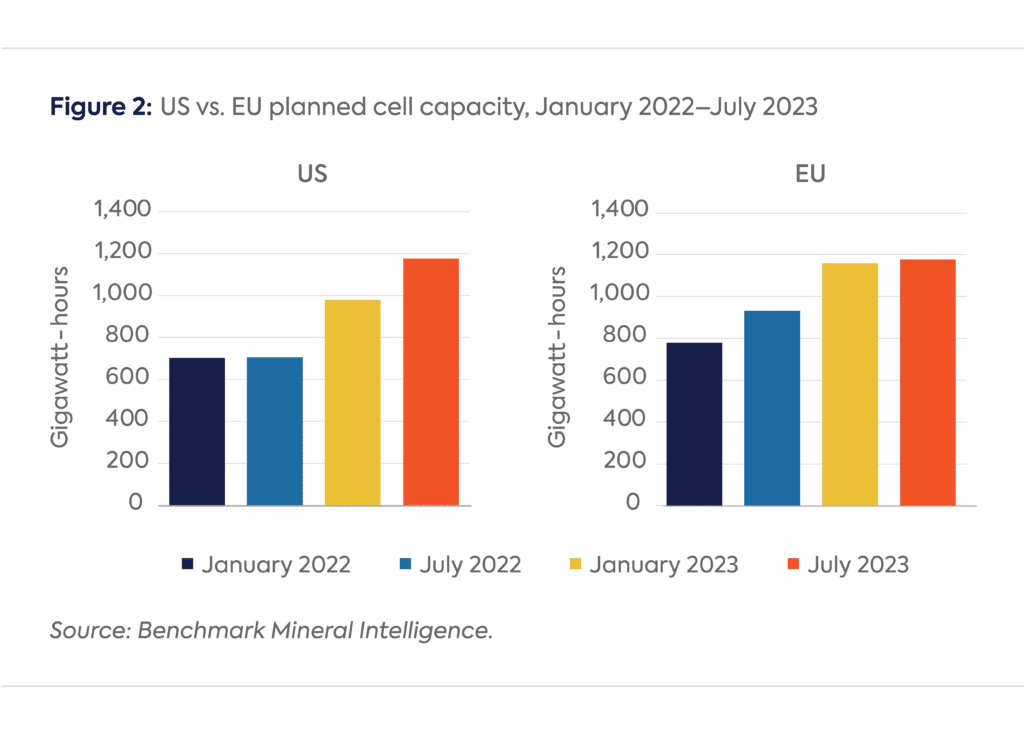

The result has been a flurry of gigafactory announcements in the United States. US gigafactory capacity in the pipeline through 2030 has increased from around 700 GWh in July 2022 (prior to the IRA) to just over 1.2 terawatt-hours (TWh) as of July 2023.[vii] Again, this is not surprising—the IRA effectively reshapes the US battery cost curve, lowering domestic costs by $45/kWh. In consequence, high-nickel US batteries now carry a cost advantage against imports of Chinese LFP cells. Importantly however, the tax credits reduce over time, from 100 percent to 75 percent in 2030, 50 percent in 2031, 25 percent in 2032, and 0 percent in 2033.

The success of the IRA in attracting gigafactory investment also means that the fiscal cost of the tax credits may be larger than initially estimated. That fiscal cost is not in the form of fiscal expenditure, however, but rather in the form of foregone tax revenue, which may be important from the public’s perspective. Figure 4 shows that the total cost of the production tax credit could reach around $150 billion by 2032.[viii] While the escalating cost of the US IRA has exacerbated opposition to the bill among Republicans (and led to objections from Democratic senator Joe Manchin),[ix] the AMPTC has benefited states with large Republican bases. Around 80 percent of clean-tech and semiconductor investments were announced in red states or states with broad Republican constituencies—most of them in South Carolina and Georgia, followed by Michigan and Ohio.[x] The reason for this is that Southern states command some of the lowest industrial electricity costs in the US (between $0.06–$0.08/kWh). It remains to be seen whether the benefits accrued by Southern states (via jobs, federal grants, etc.) will translate into any cross-partisan unity on the IRA.

The IRA has also accelerated a new wave of what have been dubbed “subsidy wars,”[xi] testing industrial policies in numerous key regions, particularly the EU. Despite the EU offering its own response to the IRA—in the form of the Critical Raw Minerals Act—corporate players there (e.g., Freyr and VW) have not shied away from trying to exploit the opportunities offered by the IRA and thus moving investment to the US. As a result, US planned cell supply through 2030 is now set to match and potentially outpace Europe (see Figure 2).

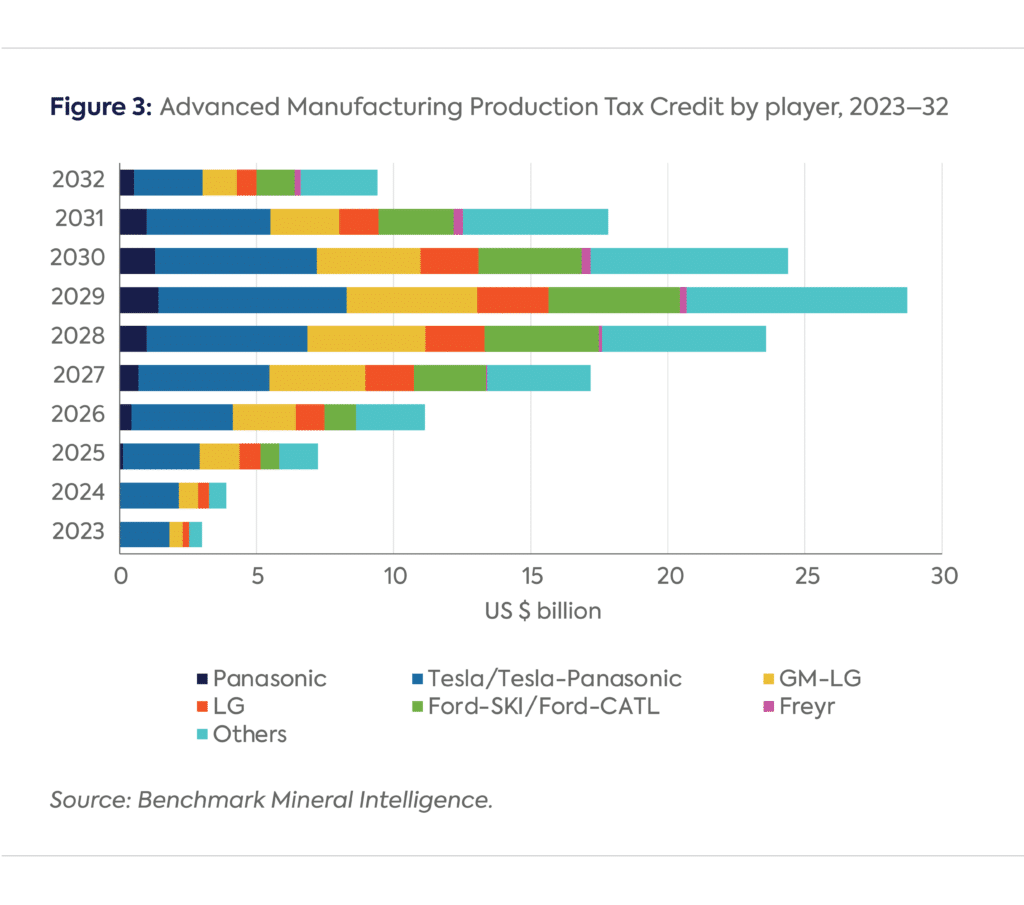

Another feature of the IRA has been the ongoing acceleration of original equipment manufacturer (OEM) joint ventures (JV) with cellmakers, particularly non-Chinese Asian firms such as LG Energy Solution, Panasonic, and SK Innovation—a model pioneered in the US market by Tesla and its JV partner, Panasonic. Because the AMPTC applies to the actual production of cells rather than planned capacity, players that had an early-mover advantage will benefit most. Figure 3 shows the likely distribution of tax credits by player, with Tesla-Panasonic set to be major benefactors of the IRA, and GM-LG Energy Solution and Ford-SK Innovation catching up later in the decade. At a company level, and assuming the AMPTC remains in place through 2032, Tesla could receive up to $45 billion in tax credits. One important consequence of this will be increased geopolitical alignment between the US and its non-Chinese Asian downstream partners, particularly South Korean cell majors such as LG Energy Solution and SK Innovation.

In addition to the supply-side incentives outlined above, the IRA introduces demand-side policy levers that incentivize EV uptake and influence OEM procurement behavior in line with the US goal of de-risking reliance on China. Four requirements need to be met to capture the full $7,500 subsidy, including final vehicle assembly in North America and local content requirements for battery components and critical minerals. The bill also includes an exclusion criterion that battery components and critical minerals cannot come from FEOCs, which will most likely include China if existing guidance on FEOCs in other contexts (e.g., the CHIPS Act) or the list of countries of particular concern to the Department of State is followed.[xii]

The IRA does not operate in a vacuum, however. Already, new offtake deals have been structured and partnerships (including those with China) have been discussed. In some cases, industry has already front-run government, with the Ford-CATL partnership (the latter being the world’s largest battery manufacturer) being the key example. The fate of this partnership could act as a bellwether of how the US government will treat China in a post-IRA landscape. As the Treasury Department continues to formulate conditions for Chinese involvement, in the short term the US will need to be pragmatic about China’s role if its goals are to support OEM electrification targets.

OEM Procurement Practices and Supply Chains Are Adapting, but Time and Further Government Support Will Be Needed

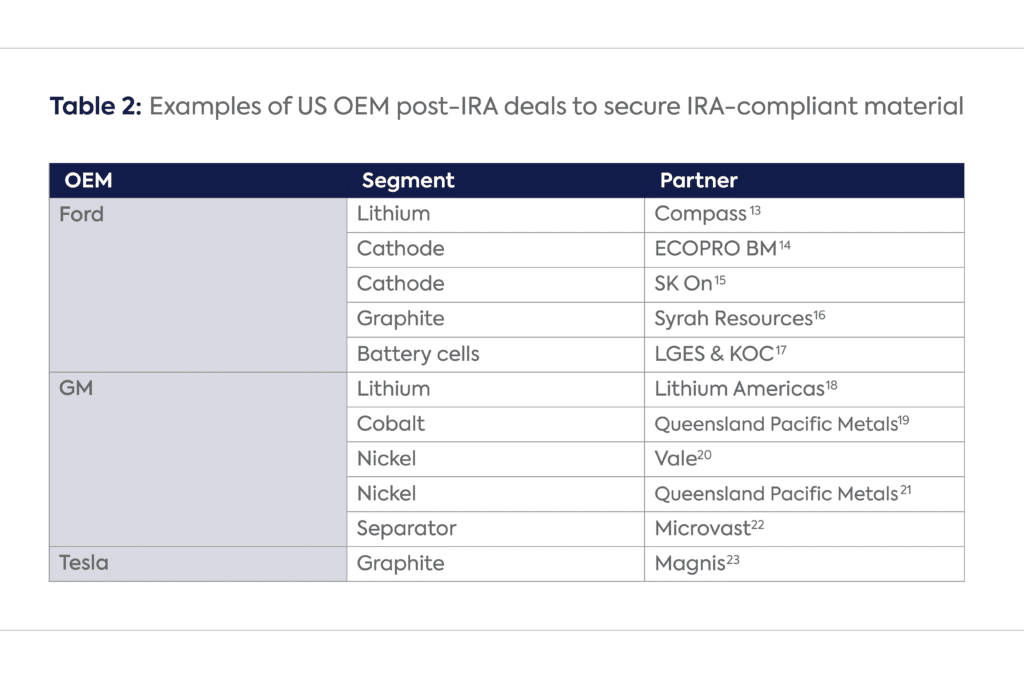

OEMs have already started responding to the IRA, screening IRA-compliant tonnages and seeking to structure offtakes (i.e., purchases) that align with the requirements of the tax credits. The largest OEMs, such as Tesla, Ford, and GM, have structured such offtakes with Free Trade Agreement–compliant players (see Table 2)—one prominent example being the one between GM and Lithium Americas Corp., which saw the former invest $650 million in the latter. Lithium players are also responding, as demonstrated by the Allkem-Livent merger, which will help improve the project economics for IRA-compliant supply (specifically Allkem’s James Bay project in Canada and Sal de Vida project in Argentina).

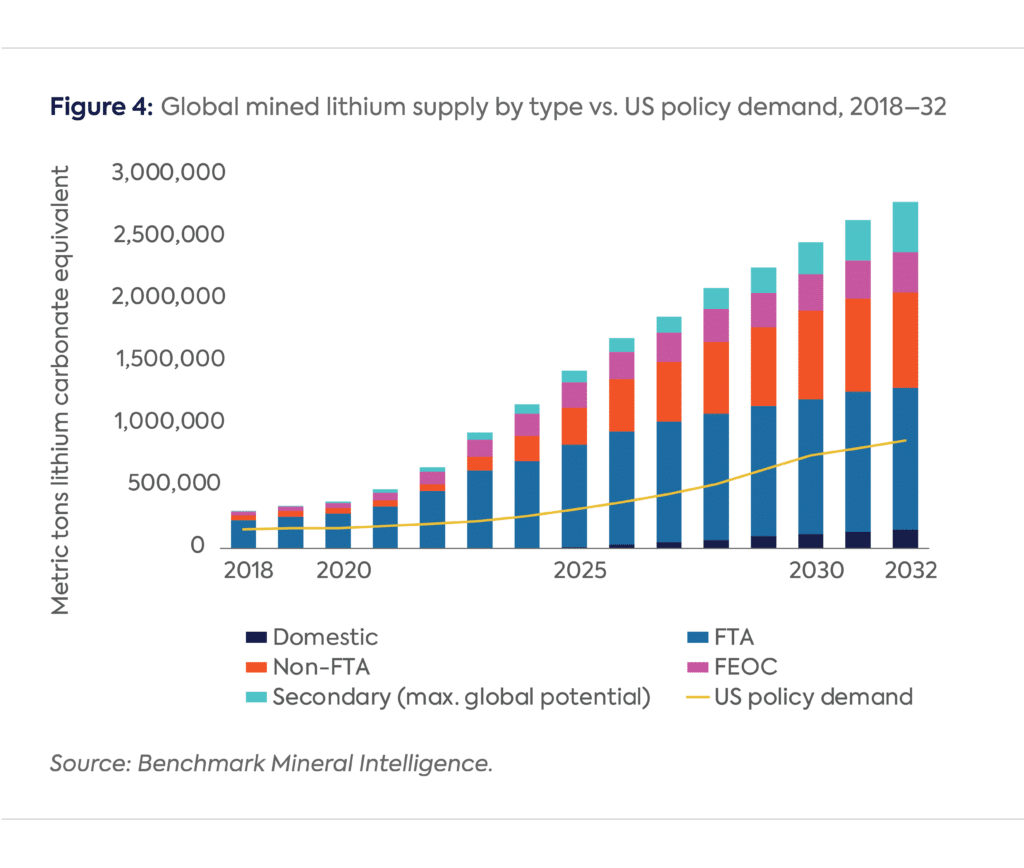

Yet OEMs will still need to accept reliance on China’s position in the global battery value chain for a large share of mineral processing, anode production, and LFP cathode production. For example, at a superficial level, an analysis of FTA-compliant lithium (see Figure 4) shows that—on a mined basis—OEMs can secure enough lithium to meet the 30D requirements. However, this comes with several major caveats that show why China will continue to play an important role, even for lithium supply:

For other critical minerals, complying with the IRA’s content requirements is equally challenging. For nickel, Indonesia is set to provide most production growth through 2025, but the country is not an FTA-listed country. The war in Ukraine has removed another major source of Class 1 nickel supply, Russia. The growing focus of OEMs on the emission intensity of various nickel processing routes (e.g., sulfide smelting and high-pressure acid leaching) adds another layer of complexity to future OEM decision-making on nickel sourcing: environmental, social, and governance (ESG) metrics around battery materials sourcing. While there is limited evidence that carbon intensity has been a key driver in OEM decision-making, factors such as carbon pricing regimes, trade tariffs, and other ESG requirements on the horizon add further uncertainty to sourcing strategies. Indonesia’s ore export ban shows the trend of governments seeking to capture more value from their resources, giving Indonesia significant leverage as a key “geopolitical swing state” in the balance of power between the US and China.

To Maximize EV Deployment and Support as well as US OEM Global Competitiveness on EVs, the US Needs to Be Pragmatic about China’s Near-Term Role

The US has not yet released guidance on how the FEOC requirement will be implemented. That guidance will be key, because the producers of cells and cathode active materials in South Korea, Japan, and other countries continue to rely on China’s supply chain.

The Department of Commerce’s current proposal to define FEOC in the context of the CHIPS Act, released in March 2023, would consider any entity in which a Chinese person or company holds at least a 25 percent voting interest an FEOC. While final rules are still forthcoming, it is worth noting the following:

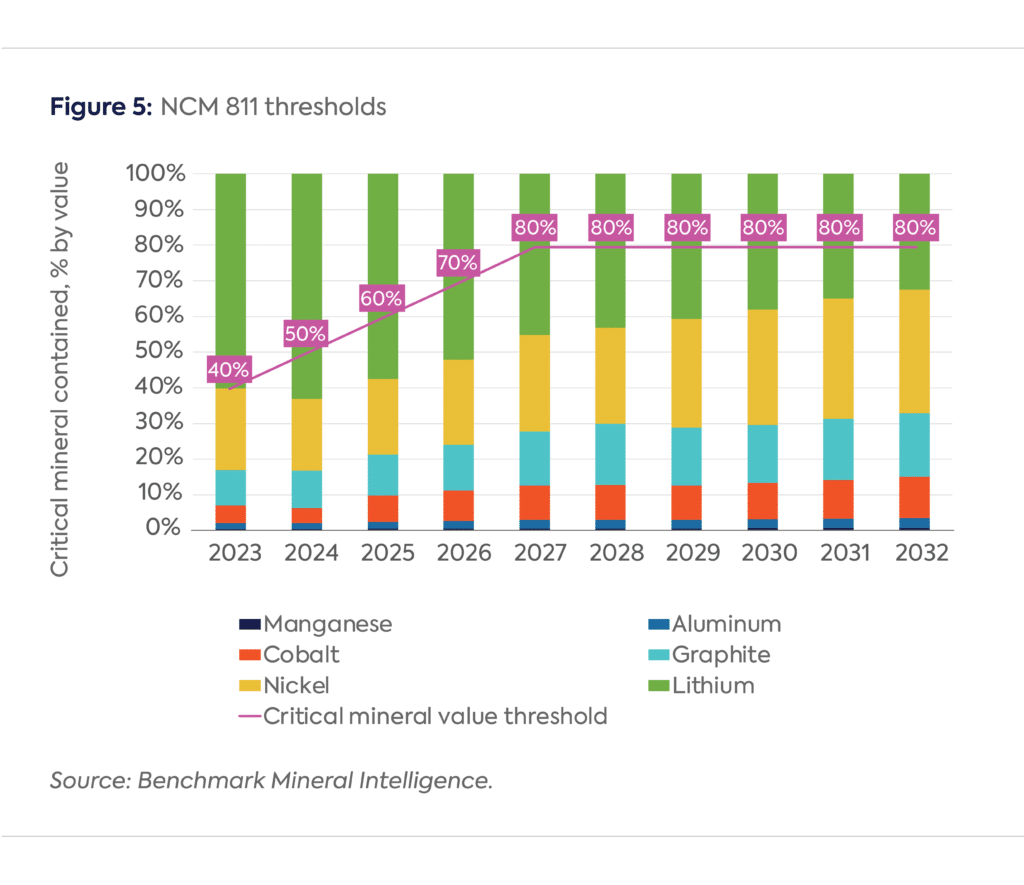

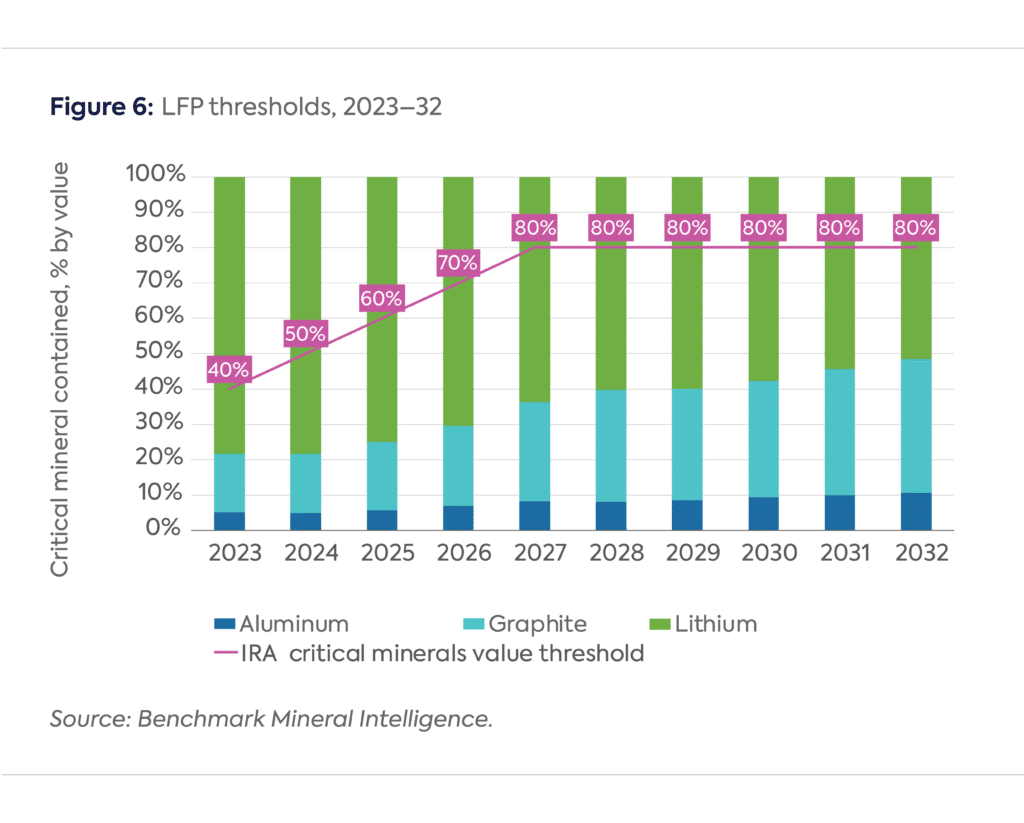

As Figures 5 and 6 show, the short-term strategy for OEMs will be to focus on lithium sourcing; longer term, however, other pinch points will come into focus, principally nickel, cobalt, and graphite sourcing. This reinforces the point that technology shifts are unlikely to make IRA sourcing any easier, even if NCM 811 sourcing will provide more opportunities than LFP cells, given that phosphate is not treated as a critical mineral.

The US IRA mimics what China did over a decade ago by using demand- and supply-side subsidies and government support to build a supply chain. Its biggest impact so far has been on the US battery cost curve and announced cell supply to 2030. The bill has already made headway in achieving one of its goals: onshoring cell supply, particularly by rewarding early movers such as Tesla. It has also created competition between governments to incentivize supply chain localization, even among US FTA partners that are seeking to capture more value from their respective industries. In its attempt to shift the demand curve, the IRA has enhanced competition for “IRA-compliant” minerals and battery components. This means that, absent an expansion of FTA countries, the IRA can only truly succeed in supporting mass-scale deployment capable of keeping the US on track with its climate targets by adopting a pragmatic attitude toward China. The US has the opportunity to crystallize new rules of the game, but if it tries to decouple completely from China, it may well face a mismatch between its supply and demand policies—an imbalance unlikely to be welcome by a value chain already operating on razor-thin margins.

[i] White House, “Fact Sheet: One Year In, President Biden’s Inflation Reduction Act Is Driving Historic Climate Action and Investing in America to Create Good Paying Jobs and Reduce Costs,” August 16, 2023,

[ii] Benchmark Source, “One Year On, Biden’s IRA Has Changed the Battery Landscape,” Benchmark Mineral Intelligence, August 15, 2023, https://source.benchmarkminerals.com/article/one-year-on-the-ira-has-changed-the-battery-landscape-in-the-us.

[iii] The wage requirement of the IRA is that all laborers and mechanics are paid wages at rates not less than the prevailing rates determined by the Department of Labor. The apprenticeship requirement is threefold—labor hours, ratio, and participation. Under the labor hours requirement, the taxpayer must ensure that, depending on when construction began, 12.5 or 15 percent of the total labor hours required by the construction, alteration, or repair of the facility are performed by qualified apprentices from a registered apprenticeship program. Under the ratio requirement, the taxpayer must ensure that the applicable ratio of apprentices to journeyworkers established by the registered apprenticeship program are met on the facility each day. Under the participation requirement, any taxpayer (or contractor or subcontractor) that employs 4 or more laborers or mechanics in the construction, alteration, or repair of the facility must also hire at least one qualified apprentice.

[iv] Internal Revenue Service, “IRS Provides Additional Guidance for Advanced Energy Projects,” May 31, 2023, https://www.irs.gov/newsroom/irs-provides-additional-guidance-for-advanced-energy-projects.

[v] Benchmark Mineral Intelligence, “Battery Cell Cost Model Q2 2023.”

[vi] Benchmark Mineral Intelligence, “Gigafactory Cost Model,” 2023; and Bernstein, “Global Energy Storage: The Olympian Gigafactory Challenge,” May 2022.

[vii] Benchmark Mineral Intelligence, “Gigafactory Assessment,” August 2023.

[viii] Benchmark Source, “One Year On, Biden’s IRA Has Changed the Battery Landscape.”

[ix] See Manchin’s response to Treasury: “Manchin Statement on Treasure EV Tax Credit Guidance,” Senate Committee on Energy and Natural Resources, March 31, 2023, https://www.energy.senate.gov/2023/3/manchin-statement-on-treasury-ev-tax-credit-guidance.

[x] Amanda Chu, Oliver Roeder, and Alex Irwin-Hunt, “Inside the $220bn American Cleantech Project Boom,” Financial Times,August 16, 2023, https://www.ft.com/content/3b19c51d-462b-43fa-9e0e-3445640aabb5.

[xi] Guy Chazen, Sam Fleming, and Kana Inagaki, “A Global Subsidy War? Keeping Up with the Americans,” Financial Times, July 13, 2023, https://www.ft.com/content/4bc03d4b-6984-4b24-935d-6181253ee1e0.

[xii] US Department of State, “Countries of Particular Concern,” accessed September 15, 2023, https://www.state.gov/countries-of-particular-concern-special-watch-list-countries-entities-of-particular-concern/#:~:text=The%20most%20recent%20Countries%20of,Arabia%2C%20Tajikistan%2C%20and%20Turkmenistan.

[13] Business Wire, “Compass Minerals Signs Binding Multiyear Agreement to Supply Ford Motor Company with Battery-Grade Lithium Carbonate,” May 22, 2023, https://www.businesswire.com/news/home/20230519005431/en/Compass-Minerals-Signs-Binding-Multiyear-Agreement-to-Supply-Ford-Motor-Company-with-Battery-Grade-Lithium-Carbonate.

[14] Ford, “EcoProBM, SK on, Ford Investing in Québec; Building Cathode Plant to Solidify EV Supply Chain in North America,” press release, August 17, 2023, https://media.ford.com/content/fordmedia/fna/us/en/news/2023/08/17/ecoprobm–sk-on–ford-investing-in-quebec–building-cathode-plan.html.

[15] Ibid.

[16] “Australia’s Syrah Resources Signs Graphite Supply Deals with US Firms,” Reuters, August 2, 2023, https://www.reuters.com/article/syrah-rsrcs-graphite-usa/australias-syrah-resources-signs-graphite-supply-deals-with-us-firms-idUSKBN2ZE025.

[17] Ford, “Ford, LG Energy Solution, and Koç Holding to Establish a Joint Venture to Produce Battery Cells as Ford Prepares to Bring More EVs to Customers in Europe,” press release, February 21, 2023, https://media.ford.com/content/fordmedia/feu/en/news/2023/02/21/ford–lg-energy-solution–and-koc-holding-to-establish-a-joint-v.html.

[18] General Motors, “GM and Lithium Americas to Develop U.S.-Sourced Lithium Production through $650 Million Equity Investment and Supply Agreement,” press release, January 31, 2023, https://www.prnewswire.com/news-releases/gm-and-lithium-americas-to-develop-us-sourced-lithium-production-through-650-million-equity-investment-and-supply-agreement-301734300.html.

[19] General Motors, “GM Enters Collaboration Agreement with Queensland Pacific Metals for Nickel from Australia,” press release, October 11, 2022, https://investor.gm.com/news-releases/news-release-details/gm-enters-collaboration-agreement-queensland-pacific-metals/.

[20] General Motors, “Vale and GM Sign Long-Term Nickel Supply Agreement in Canada Critical to North American EV Supply Chain,” press release, November 2022, https://news.gm.com/newsroom.detail.html/Pages/news/us/en/2022/nov/1117-vale.html.

[21] General Motors, “GM Enters Collaboration Agreement with Queensland Pacific Metals for Nickel from Australia,” press release, October 11, 2022, https://investor.gm.com/news-releases/news-release-details/gm-enters-collaboration-agreement-queensland-pacific-metals.

[22] General Motors, “General Motors and Microvast to Develop Specialized EV Battery Separator,” press release, November 2022, https://news.gm.com/newsroom.detail.html/Pages/news/us/en/2022/nov/1102-microvast.html.

[23] “Australia’s Magnis in Deal with Tesla to Supply Graphite for Electric Vehicle Batteries,” Reuters, February 20, 2023, https://www.reuters.com/business/autos-transportation/australias-magnis-deal-with-tesla-supply-graphite-electric-vehicle-batteries-2023-02-20/.

[xxiv] Tolling refers to an agreement with a third party to process raw material or semi-finished product for a fee.

[xxv] Benchmark Source, “Opinion: Grow or Be Bought: Livent-Allkem Merger Sets Scene for Industry Consolidation,” Benchmark Mineral Intelligence, May 12, 2023, https://source.benchmarkminerals.com/article/opinion-grow-or-be-bought-livent-allkem-merger-sets-scene-for-industry-consolidation.

[xxvi] Jenna N. Trost and Jennifer B. Dunn, “Assessing the Feasibility of the Inflation Reduction Act’s EV Critical Mineral Targets,” Nature Sustainability 6 (2023): 639–643, https://doi.org/10.1038/s41893-023-01079-8

[xxvii] Heekyong Yang and Zoey Zhang, “Chinese Firms Ramp Up Investment in South Korea to Get US EV Tax Credits,” Reuters, July 31, 2023, https://www.reuters.com/technology/chinese-firms-ramp-up-investment-skorea-get-us-ev-tax-credits-2023-07-31/.

[xxviii] “China’s Xi Has Mixed Feelings about CATL’s Battery Market Dominance,” Reuters, March 7, 2023,

[xxix] Benchmark Source, “Five Things You Need to Know about Manganese and Batteries,” Benchmark Mineral Intelligence, August 17, 2023, https://source.benchmarkminerals.com/article/five-things-you-need-to-know-about-manganese-and-batteries.

This open access book sheds new light on the challenges and opportunities of downstream diversification in countries rich in critical minerals

Securing critical minerals is a top priority of governments around the world.

Elemento decisivo será coordenação estratégica

Full report

Commentary by Ahmed Mehdi & Tom Moerenhout • September 20, 2023