This website uses cookies as well as similar tools and technologies to understand visitors’ experiences. By continuing to use this website, you consent to Columbia University’s usage of cookies and similar technologies, in accordance with the Columbia University Website Cookie Notice.

The Center on Global Energy Policy (CGEP) at Columbia University SIPA today released a new report examining Project-based Carbon Credit Markets (PCCMs) in G20 countries and Singapore. A...

Announcement• June 17, 2026

Energy Explained

Get the latest as our experts share their insights on global energy policy.

The 109-day-old Iran crisis is heading toward an off-ramp in the form of a not-yet-public Memorandum of Understanding to reopen the Strait of Hormuz. While energy markets are...

This event will take place in-person in Washington DC, at the Rayburn House Office Building, Room 2168 (Gold Room). Advance registration is required. Announcing New Columbia University Publications...

We are the premier hub and policy institution for global energy thought leadership. Energy impacts every element of our lives, and our trusted fact-based research informs the decisions that affect all of us.

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. Rare cases of sponsored projects are clearly indicated.

For a full list of financial supporters of the Center on Global Energy Policy at Columbia University SIPA, please visit our website at Our Partners. See below a list of members that are currently in CGEP’s Visionary Circle. This list is updated periodically.

European proposals[1] to replace Russian gas shipped via Ukraine[2] with gas from Azerbaijan when current transit agreements with Moscow expire at the end of 2024[3] may be easier said than done.[4] Lack of transparency around the deal has created unreasonable expectations and accusations.[5] While Ukraine, the EU, and Azerbaijan may all support the idea of buying Azeri gas and injecting it into Russian pipelines heading to Europe,[6] the three options to bring that plan to fruition face significant hurdles or require compromises on the goal. Most importantly, Azerbaijan will not have sufficient additional gas supplies in the short term to replace Russian gas volumes, Naftogas talks about “only 2 billion cubic meters [bcm] of the 14 bcm that the EU receives via the Ukraine pipeline” [7] although that could change in the longer term if buyer interest hits a level that spurs investment.

This blog post discusses the benefits of replacing Russian gas with Azeri fuel for Ukraine, the EU, and Azerbaijan, and explores the three options for bringing that fuel to Europe. The piece finds that in the short term the only realistic way to replace the existing volumes of Russian gas would be through swap deals between Azerbaijan and Russia, but this would have only limited benefits in terms of reducing EU dependence on Moscow.

Why Do Ukraine, the EU, and Azerbaijan Want This Deal?

Ukraine:

Ukraine earns transit fees from Russian gas flowing through its pipelines, initially expected to amount to $7.15 billion over 2020–24.[8] However, Gazprom only paid around $500 million during January-June 2023 (UAH 19.2 bn) due to lower transit volumes.[9] Maintaining these revenues is important for Ukraine’s economy; transit fees represent around 2 to 3 percent of the expected revenues for 2024.[10]

Shipping Azeri gas to Europe would reinforce Ukraine’s role as a key transit country for ensuring European energy security. It would allow Kyiv to protect its relationship with Slovakia and Austria, the two countries most dependent on supplies via Ukraine.[11]

“Virtual reverse” (when gas is physically transported in one direction but mutually accounted for in both directions through settlements) has allowed Ukraine to secure physical gas supplies,[12] even after halting direct purchases from Gazprom and switching to European traders. Despite the current reduced gas consumption due to the war, this system remains beneficial even though Ukraine claims to be self-sufficient in gas.[13]

In the past, maintaining external gas flows and using Russian gas to balance the network has been seen as technically essential for Ukraine to ensure adequate system pressure and effective distribution because its gas extraction and consumption centers are not optimally located.

The complete cessation of Russian gas transit via Ukrainian GTS would also pose a gas supply security risk as without its transit role the Ukrainian gas transmission system would very likely be subjected to further Russian missile attacks (Until now, the Ukrainian gas transmission system has been largely spared by Russian attacks, though gas facilities have been targeted, including facilities in Western Ukraine in April 2024.[14])

Azerbaijan:

By supplying gas to Europe via Ukraine, Azerbaijan can strengthen its position in the European energy market—one of its long-term strategic goals since it signed a memorandum of understanding with the EU in July 2022.[15] Hungarian Minister of Foreign Affairs and Trade Péter Szijjártó visited Azerbaijan in April[16] to strengthen energy ties between the two countries in the framework of the Southern Gas Corridor. Hungary’s state-owned MVM signed a contract to acquire 5 percent of the Azeri Shah Deniz gas field in June (equivalent to 1.5 billion cubic meters [bcm]/y of gas supplies).[17]

The deal would strengthen Azerbaijan’s political ties with the EU and Ukraine, thereby enhancing its regional influence and generating revenue.

The deal would also increase the importance of Azerbaijan vis-a-vis Russia.

The EU:

The EU aims to diversify its energy sources as part of ceasing its import of all Russian gas by 2027. While the EU has reduced Russian pipeline gas imports already,[18] some Central European countries still depend on Russian gas transiting via Ukraine (12 bcm in 2023).[19] Replacing Russian gas in January 2025 after the EU’s transit contracts with Russia expire could be very difficult, especially for Slovakia. Slovakian Prime Minister Robert Fico went to Azerbaijan in May[20] stating he would do “everything politically necessary” to receive Azeri gas. Meanwhile, Hungary, which is on friendlier terms with Russia, holds the EU presidency for the second semester of 2024.

The deal aligns with the EU’s broader strategy of supporting Ukraine amid its ongoing conflict with Russia.

Russia’s position on these negotiations is nuanced. For the Russian government and Gazprom, the deal is less favorable compared with extending the current transit agreement (currently not feasible), but could help to preserve a shrinking market share in Europe by enabling gas flows to the EU via Ukrainian GTS after 2025. Re-labeling some gas flows as Azerbaijani is better than stopping supplies via this route entirely. While not promoting this idea, Russia has not opposed it either, showing a pragmatic stance given the circumstances.

How Will Gas from Azerbaijan Get into the Ukrainian Pipeline System?

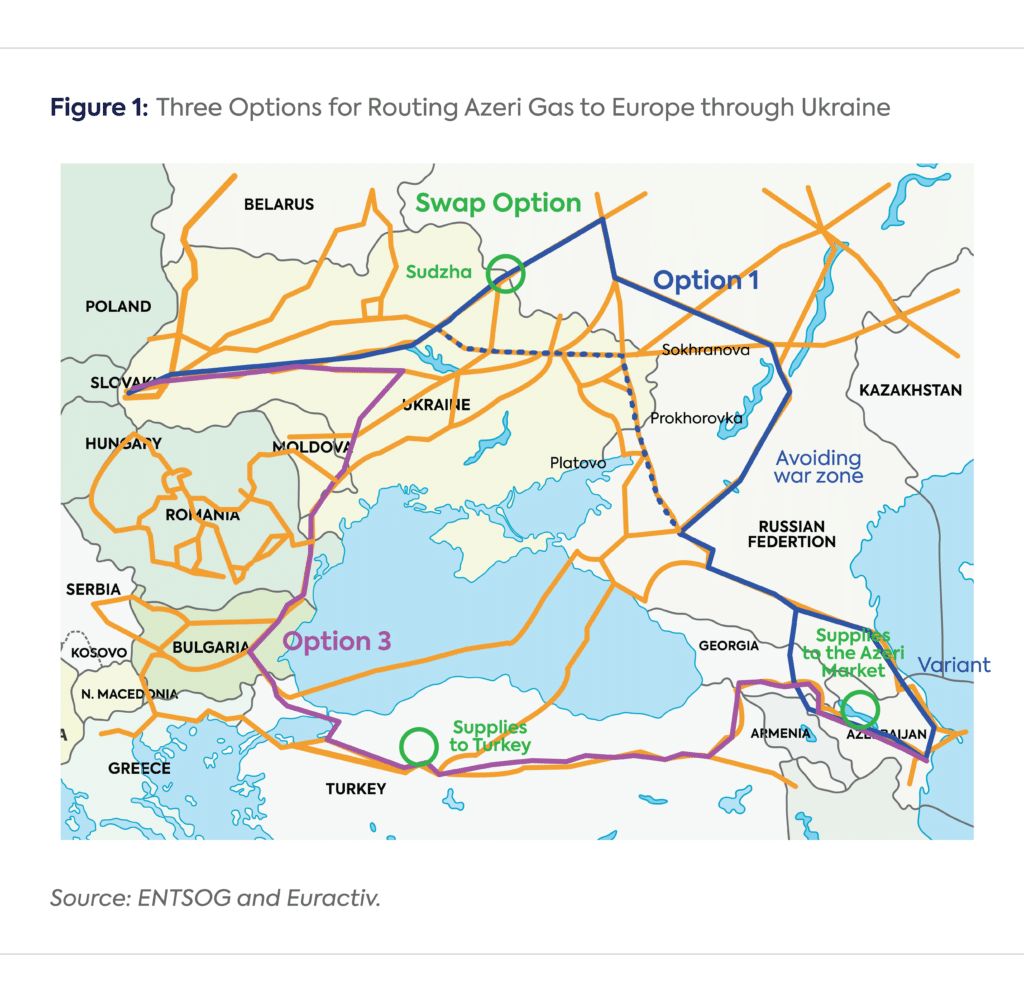

There are three options for routing Azeri gas to Europe through Ukraine.

Option 1: Shipping it from Azerbaijan through Russia and then Ukraine. The main obstacle here is that transiting through the current conflict zone might prove impossible (see the red dotted line on the map in Figure 1).[21] Russia is also unlikely to facilitate gas transit from an alternative supplier through its territory without deriving significant benefits,[22] especially if this lowers its pipeline exports,[23] and could require transit payments from Azerbaijan in the framework of the Eurasian Economic Union. It is uncertain whether this would be enough for Russia and whether EU consumers or Azeri producers would pay for the transit and accept the associated risk.

Option 2: Creating swap arrangements between Russian and Azeri gas. Russian gas (titled “Azeri gas”) would be delivered at the Russian–Ukrainian border while Russian-titled gas would be sent elsewhere. Realistically, the only new markets that Azerbaijan could propose to Russia are its domestic market and Turkey (by replacing Azeri exports through the Southern Gas Corridor). The domestic market option could be problematic: it is unlikely that Russia would agree to sell its gas at the very low prices prevailing in Azerbaijan’s domestic market or that Azerbaijan would pay European price levels for 10-15 bcm/y—meaning a compensation mechanism would need to be devised. Alternatively, Russian gas could be sent to Turkey instead of Azeri gas.[24] This scheme would resemble the RosUkrEnergo gas supply contract of 2004–09 in which Gazprom sold a gas mix of unknown origin to RosUkrEnergo that it officially labeled Turkmen gas.[25]

Option 3: Shipping Azeri gas through alternate pipelines. Azerbaijan could send gas westward via the 24 bcm/y South Caucasus Pipeline (SCP)[26]and the 17.5 bcm/y TANAP[27] in Turkey and then northward through Bulgaria-Romania interconnections to Ukraine. The problem with this option is that according to Azeri president Ilham Aliev the Southern Gas Corridor is already at capacity. Meanwhile, the expansion of the SCP to 34 bcm/y and TANAP to 31 bcm/y is not yet confirmed and would require long-term commitments from European customers who thus far have not shown a willingness to make them.[28] Additionally, even if the contracts were signed, several years and several billion Euros would still be needed for the expansion to be realized. Simply put, this will not happen by January 2025.

All three of these options would preserve Ukrainian transit, though the third is slightly more convoluted since Azeri gas would have to travel from the EU to Ukraine and then back to the EU just to preserve the transit—at a cost for European buyers (though potentially averting the need to build new gas infrastructure in Southern Europe). Their viability depends on whether capacity is really available on each route (depending on existing flows and contracts).

The first two options involve Russia, and would likely require an interconnection agreement for the Sudzha border crossing. The lack of such an agreement is currently preventing EU buyers from contracting Russian gas directly at Sudzha. Meanwhile, Russia would retain the ability to cut gas supplies at any moment, as it has done previously.

The first and third options would effectively lower Russian gas supplies to Europe, but would also require additional Azeri gas. Most importantly, replacing around 10–15 bcm of Russian gas by January 2025 currently looks impossible. The second option would allow the Europeans and Ukrainians to save face by displacing Russian sales to another market, but would neither reduce Russian sales nor diminish Moscow’s influence on gas transit.

Where Will Azerbaijan Find Additional Gas Volumes?

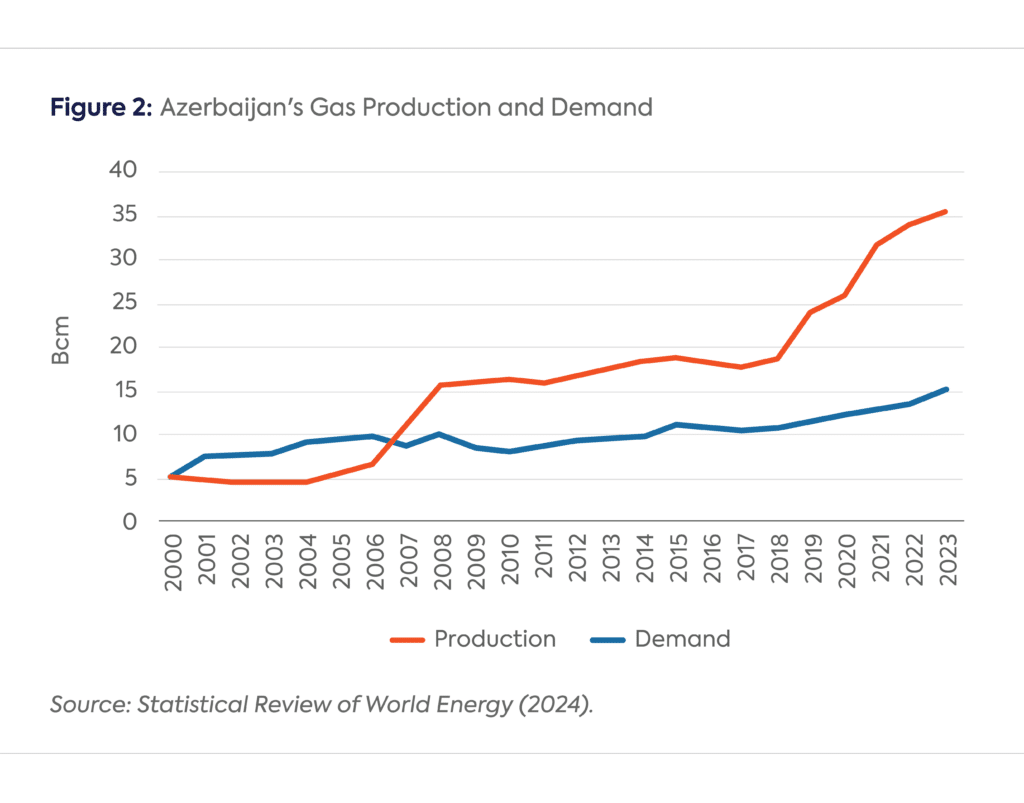

Azerbaijan wants to boost its gas exports to Europe[29] via the Southern Gas Corridor but has not secured sufficient long-term deals yet to invest in further production.[30] In fact, Azerbaijan cannot currently offer any significant additional volumes of gas to replace the existing Russian transit via Ukraine. The Azeri supply–demand balance is so tight that Azerbaijan had to import gas from Russia during the winter of 2022-23 and from Turkmenistan.[31]

Exporting an additional 10–15 bcm would require significant upstream expansion (from fields such as Umid, Absheron, and ACG Deep) and possibly infrastructure expansion depending on which option was adopted. Umid’s gas production is expected to reach 2.4 bcm in 2024, with a potential to increase to 4.4 bcm.[32]No final investment decision has been taken on Absheron Phase 2 yet (+4 bcm/year).[33] First gas from ACG deep could start in 2025 from the first production well, but no concrete development plan has surfaced yet.[34] Any increase in hydrocarbon production is complicated by the fact that Azerbaijan is due to host the UN’s annual Congress of the Parties (COP29) climate summit in November this year.[35]

Expanding production would require long-term purchasing commitments from EU countries,[36] possibly Slovakia when its 5.5 bcm contract with Gazprom expires in 2028, on top of Hungary’s 1.5 bcm. But these could potentially clash with the EU’s proposed target of 90 percent greenhouse gas emissions reduction by 2040. An alternative option of sourcing gas from Turkmenistan and shipping it through Azerbaijan would face even bigger challenges given that Turkmenistan is among the largest methane emitters in the world. Azerbaijan must also meet its domestic needs, which have increased from 10.8 bcm in 2018 to 15.1 bcm in 2023.

Conclusion

Realistically, the only way to replace existing volumes of Russian gas in the short term is through swap deals between Azerbaijan and Russia. This would involve Russian gas continuing to flow to the EU via Ukraine under the label of Azeri gas. Such an arrangement would provide an additional bargaining point for Ukraine in potential negotiations with Russia. It could also be a way for Kyiv and the EU to show progress in reducing their reliance on Russian gas transit and Russian gas, respectively. Additionally, the arrangement would significantly increase the interdependency between Russia and Azerbaijan, which has strengthened since 2022 to the advantage of both sides, and which was strongly criticized by the EU when Azerbaijan started purchases of Russian gas in 2022–23. The deal underlying these purchases was not prolonged in part due to EU pressure, but it could be reborn in a new guise. Beyond the next 3 to 5 years, there is a slim possibility that Azerbaijan could play a bigger role in Eastern Europe, but this would require commitments by EU buyers who as yet have not shown any willingness to make them.

Foundations and Individual Donors Anonymous Anonymous the bedari collective Jay Bernstein Breakthrough Energy LLC Children’s Investment Fund Foundation (CIFF) Arjun Murti Ray Rothrock Kimberly and Scott Sheffield

[21] Ukraine stopped receiving gas through the southern entry point (Prokhorovka and Platovo) in 2015. In May 2022, GTSOU declared force majeure at the Sokhranovka entry point.

El Consejo Mexicano de Asuntos Internacionales (COMEXI) y la Unidad de Estudio y Reflexión sobre Energía y Sustentabilidad, presentan el análisis: “Posición en materia de energía y sustentabilidad en la revisión del T-MEC" El documento analiza cómo México puede aprovechar este proceso para fortalecer la integración energética de América del