This website uses cookies as well as similar tools and technologies to understand visitors’ experiences. By continuing to use this website, you consent to Columbia University’s usage of cookies and similar technologies, in accordance with the Columbia University Website Cookie Notice.

The Center on Global Energy Policy (CGEP) at Columbia University SIPA today announced new personnel additions who bring extensive experience from government and the private sector to the...

Announcement• July 3, 2025

Energy Explained

Get the latest as our experts share their insights on global energy policy.

The European Commission (EC) published a proposed regulation on June 17 to end Russian gas imports by the end of 2027; this followed the initial roadmap to do...

The global energy landscape is shifting right now. Geopolitical tensions in the Middle East, debates about peak oil demand, and waning support for climate action in some parts...

This year, the Third Annual Energy Opportunity Lab (EOL) Forum will take place July 7th and 8th in Washington, DC, offering a chance for the Washington policymaking community...

Event

About Us

We are the premier hub and policy institution for global energy thought leadership. Energy impacts every element of our lives, and our trusted fact-based research informs the decisions that affect all of us.

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision. Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. Rare cases of sponsored projects are clearly indicated.

For a full list of financial supporters of the Center on Global Energy Policy at Columbia University SIPA, please visit our website at Our Partners. See below a list of members that are currently in CGEP’s Visionary Circle. This list is updated periodically.

As the summer approaches, the European Union (EU) is confronting an unusual situation amid the worst energy crisis in its history: too much gas to handle—at least in the near term. A short-term glut can become a shortfall in the winter if Europe slows the pace of storage injections or runs out of storage space. Ukraine, with the world’s third-largest gas storage capacity, could help solve this unexpected challenge.

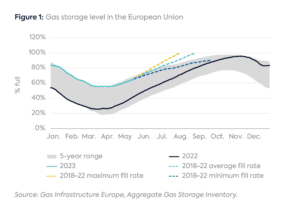

Thanks to a combination of warmer-than-normal weather, price-driven demand destruction, and well-timed policy action,[1] the gas balance in Europe looks surprisingly favorable. Gas storage levels in the European Union ended the heating season at 56 percent of capacity on April 1, 2023, an all-time high and more than twice the level a year earlier. By May 20, 2023, EU gas storage was 66 percent full (compared to a five-year average of 47 percent on the same date). If average fill rates of the 2018–2022 period persist, storage levels are projected to reach full capacity by the end of August. At the maximum fill rate observed during the previous five-year period, tank tops would be reached by early August, three months earlier than net stock draws normally begin for the winter. But even if fill rates decline to the slowest observed rate of the 2018–2022 period, gas stocks in the EU would reach the mandated 90 percent storage level by late September, more than a month before the November 1 deadline (Figure 1).[2]

An Unplanned Glut in Europe

As strange as it sounds given prices of around $40 per million British thermal units (MMBtu) only 6 months ago,[3] a temporary gas market glut is a distinct possibility in Q3. The market could adjust to Europe’s diminishing gas storage capacity in at least five ways.

The pace of storage injections in Europe could slow. This year’s storage fill season started more slowly than the five-year average rate. However, storage would only have to fill at less than 70 percent of the average rate to reach last year’s levels by November 1.

Some price-sensitive demand could return within the EU, especially in the power and industrial sectors. So far, no evidence supports this revival, at least in the high-frequency sector-level data reported by system operators in European countries representing the majority of demand.[4]

If Asian liquefied natural gas (LNG) demand rebounds while Europe becomes oversupplied, European prices could drop below Asian benchmarks and LNG cargo diversions from Europe to Asia could emerge. So far, this shift has not taken place.[5]

If both European and Asian demand for LNG weakens further, the market could experience a brief repeat of 2020, with US LNG cargo cancellations and rock-bottom prices in both Europe and Asia.[6] Cancellations are relatively unlikely now, given the low Henry Hub price and the resilience of US gas production, but they remain a possibility.[7]

Absent outright cargo cancellations, LNG suppliers to Europe could keep LNG in floating storage until stock draws begin to free up space in underground storage. A similar dynamic helped resolve temporary infrastructure bottlenecks in Q4 2022, and the volume of LNG on the water for more than 20 days began to climb in May 2023.[8] However, the storage capacity LNG vessels can provide is relatively small (about 0.1 billion cubic meters [bcm] of gas per average-sized vessel)[9] and temporary, as 0.1–0.15 percent of LNG stored in a tanker evaporates every day.[10]

Each of these outcomes would be detrimental to the energy security of Europe because the EU needs more gas during the winter than it can withdraw from storage.[11] Any amount of incremental gas that the EU cannot absorb between the summer and the start of the heating season would be missing from the balance even in a mild winter. This year, the continent will likely need even more gas to compensate for a further 60 percent drop in Russian pipeline gas flows,[12] continuing production declines (including the planned closure of the Groningen field in the Netherlands in October 2023),[13] and any normalization in winter temperatures.[14]

Ukraine: The Storage Giant Next Door

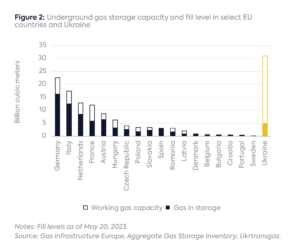

Faced with a storage shortage within its own borders, the EU—which itself possesses a little over 100 bcm of underground storage capacity[15]—has one enormous “flexibility asset” at its doorstep: 31 bcm of underground storage capacity in Ukraine, of which only about 17 percent (5 bcm) was filled in late May (Figure 2).[16] Ukraine’s vast gas storage capacity (surpassed only by the United States and Russia) is owing to its former role as a major transit country for Russian gas to Europe and its much larger gas consumption profile in earlier decades.[17] About 25 bcm of its capacity is located in the western part of the country and a further 2 bcm is in central Ukraine, far from the frontlines and under firm Ukrainian control. About 4 bcm is closer to the eastern entry points for Russian gas (partially on occupied territory).[18]

In 2020, Ukraine harmonized its regulatory framework with that of the EU and substantially reduced the cost of warehousing gas in Ukrainian storage for EU-based traders by cutting transport tariffs and exempting temporarily stored gas from customs duties.[19] Thanks to these reforms, European customers were able to use Ukrainian storage sites during the 2020 gas market oversupply, when EU storage sites filled up ahead of the winter. At the peak of the 2020 gas glut, about 10 bcm of gas was stored in Ukraine by foreign traders.[20]

In April 2023, Ukrtransgaz (Ukraine’s state-owned gas storage operator) was certified as a European storage operator, meaning it can hold strategic gas reserves for EU member states.[21] However, the ongoing war in Ukraine has made it riskier to store the EU’s temporary gas surplus—let alone its strategic stocks—in the country.

Damage to physical gas infrastructure, loss of control over specific facilities, and government bans on natural gas (re)exports in supply emergencies (such as those imposed at the start of the war in March 2022)[22] are just a few risk factors facing European traders considering using Ukraine’s warehouse regime. Securing insurance against such force majeure-type events could be particularly challenging. Storing third-party gas in Ukraine would require additional public guarantees for commercial companies to utilize the state-owned capacity. International financial institutions, such as the European Bank for Reconstruction and Development, and bilateral donor involvement from the EU and the US could play a role in providing guarantees to cover political and war-related risks. Ukraine has already asked the European Union to provide war risk insurance for its storage facilities to encourage their use by foreign traders. Meanwhile, the CEO of Naftogaz (the parent company of Ukrtransgaz) recently offered 10 bcm of storage capacity to the EU[23] and suggested that Ukraine could become an “energy bank” for Europe.[24]

A Mutually Beneficial Storage Play

De-risking the use of Ukrainian storage could improve energy security both in the EU and within Ukraine itself. Ensuring that the current gas surplus in Europe carries into the winter could help Ukraine’s western neighbors continue supplying gas to Ukraine, which has received virtually all of its gas imports via EU countries (in the form of physical or virtual reverse flows) since 2015.[25] More than 60 percent of the gas foreign companies stored in Ukraine in 2020 was sold into the Ukrainian market and most of the remainder was carried forward to the following year, leaving only a tiny fraction re-exported to the EU within the year. If the next European winter is mild, a similar situation could occur. Current rules allow the duty-free warehousing of gas in Ukrainian storage for up to three years, so European companies could work toward building a multiyear buffer in Ukraine if the gas is not needed on the continent (or in Ukraine) this winter or next year.

Ukraine’s underused and readily available storage capacity offers a unique opportunity for Europe to carry forward its current—but temporary—gas surplus into the winter and beyond. But reducing the risks of storing gas in a country at war to acceptable levels would require additional well-timed policy action from Ukraine’s Western partners in the months ahead.

Foundations and Individual Donors Anonymous Anonymous the bedari collective Jay Bernstein Breakthrough Energy LLC Children’s Investment Fund Foundation (CIFF) Arjun Murti Ray Rothrock Kimberly and Scott Sheffield

[2] The highest fill rate recorded within the European Union was just under 98 percent in October 2019, according to Gas Infrastructure Europe’s AGSI database. EU storage levels never exceeded 96 percent in 2020, another year characterized by excess supply and stretched underground storage capacity in Europe. These historical storage peaks suggest that the effective technical capacity of underground storage sites across the EU is slightly less than 100 percent.

[11] The only question is how much imports the EU needs during the winter months, and to what extent the price has to go up to attract incremental supplies. With an ample storage cushion, the price of gas during the peak winter months has to go up by less than without one.

The European Commission (EC) published a proposed regulation on June 17 to end Russian gas imports by the end of 2027; this followed the initial roadmap to do...

Saudi Arabia’s recent moves into the liquefied natural gas (LNG) market may be a sign the giant oil exporter is looking to expand into a rapidly growing and politically influential market it had long ignored.

Over the past few decades, liquified natural gas (LNG) trade has evolved from the initial point-to-point business model of the 1960s to become more flexible.

Calls to "Drill, baby drill" are back with Donald Trump's return to the White House, and for US natural gas production, the catchphrase might also be a necessity over the next three years if demand for the fuel grows as steeply as expected.