Big banks predict catastrophic warming, with profit potential

Morgan Stanley, JPMorgan and an international banking group have quietly concluded that climate change will likely exceed the Paris Agreement's 2 degree

Current Access Level “I” – ID Only: CUID holders, alumni, and approved guests only

Get the latest as our experts share their insights on global energy policy.

Steps by the second Trump administration show it is taking a tougher stance against the regime of Nicolas Maduro. Trump recently issued an executive order that could levy a 25...

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

The European Union’s energy landscape is transforming rapidly, as the bloc works to reduce emissions, lower energy prices, and decrease dependence on Russian fuel—three goals proving to be...

Find out more about our upcoming and past events.

The Columbia Global Energy Summit 2024 is an annual event dedicated to thought-provoking discussions around the critical energy and climate challenges facing the global community.

Insights from the Center on Global Energy Policy

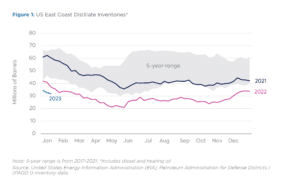

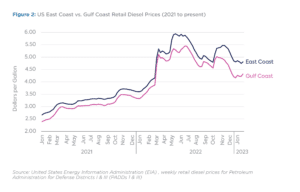

With European Union sanctions[1] on Russian petroleum products exports scheduled to come into effect on February 5, disruption in diesel markets continues to represent an economic risk globally[2] and, particularly, for the United States East Coast. The region has seen low Preview Changes (opens in a new tab)distillate (diesel and heating oil) inventories (Figure 1) and a blow-out in the premium of US East Coast prices versus the Gulf Coast (Figure 2) over the past year, and there are structural reasons why these could reoccur. This is particularly hard right now for low-income consumers, who spend disproportionately a higher percentage of their income on heating their homes in winter months. This post focuses on potential policy options to improve supply resilience during the energy transition, arguing that building strategic inventories could help now but the long-term solution may be to lower heating oil demand.

The first structural issue is on the demand side. The East Coast accounts for 82 percent of the heating[3] oil consumed in the US, while other regions have switched to different heating sources. This dependence on an oil product for heating is also a challenge for energy decarbonization in the region.

On the supply side, Russia’s invasion of Ukraine tightened global diesel markets and highlighted the consequences of the East Coast’s diesel import dependence. Around 84 percent of the region’s distillate supply comes from outside the region, with significant dependence on one major pipeline[4] from the US Gulf Coast, and from foreign imports. The imports, which reached 21 percent in 2021, are subject to a variety of geopolitical risks.[5] The East Coast’s refining capacity[6] fell by half over the last decade as plants closed due to lack of competitiveness in refined product yields and difficulty in obtaining low-cost feedstock. The Jones Act[7] requires shipments of merchandise, including fuels, between US ports to utilize US ships with American crews. High costs and low availability of Jones Act tankers make it challenging for the East Coast to receive seaborne crude or refined product from the Gulf Coast refining center to offset any loss of foreign imports.

Global diesel markets were already tight before Russia’s invasion of Ukraine, and the war worsened supply risks. Russia has been the world’s second largest exporter of petroleum products after the US and the major supplier[8] of diesel to Europe. Developed economies have lost about 2 million barrels per day of refining capacity[9] since the start of COVID-19, while demand for the fuel has surged due to pandemic recovery and fuel-switching into diesel from natural gas (outside of the US). This is because prices of natural gas have risen even higher, exacerbated by disruptions in gas supplies from Russia to Europe. Other factors affecting diesel supply included strikes in refineries in Europe[10] and limitations on Chinese[11] refinery exports last year. Diesel markets could further deteriorate given the EU’s upcoming oil ban on Russian petroleum products. Adding uncertainty is the impact of a price cap[12] on Russia’s product exports to other markets, also expected to come into effect on the same day.

Geopolitical considerations are also an increasingly important factor in global refining markets. Today about 60 percent of global refinery capacity is already located in emerging markets.[13] The additional 3 million barrels per day (b/d) of refinery capacity expected to come online in the next couple of years will primarily come from national oil companies of emerging markets.[14] This makes it all the more important for policymakers to factor in energy security considerations in their decision matrix.

Policy questions revolve around how to make the US East Coast more resilient to distillate supply disruptions[15], stock outages, price spikes[16] and cyberattacks.[17]

In the short term, a potentially effective solution would be waiving the Jones Act to allow the US East Coast to receive additional domestic supplies from the Gulf Coast in foreign tankers. This will increase diesel availability and reduce costs. However, the EU ban on Russian product imports could increase foreign tanker[18] costs as well with Russian diesel exports and European imports having to travel longer distances on tankers. Another short-term solution would be to make greater use of the federal Low-Income Home Energy Assistance program (LIHEAP)[19] in the region this winter to assist low-income consumers with home heating bills while making homes more energy efficient.

In the medium term, requiring a strategic diesel reserve and/or mandatory minimum levels of diesel inventories might be a policy solution fit for energy security concerns in the age of the energy transition. In the face of uncertainties such as the pace of oil demand decline and sufficiency of product supplies, a greater level of distillate stocks could help temper regional distillate price spikes.

The strategic Northeast Home Heating Oil Reserve (NEHHOR)[20] has set a precedent for such a policy. The NEHHOR, which was first created in 2000 and subsequently converted to a 1-million-barrel reserve of ultra-low-sulfur diesel for New England, could now be significantly increased. Alternatively, such policy could apply to commercially held stocks or to a combination of government and commercial stocks. Commercially held stocks offer the advantage of faster deployment to markets vs. a government-owned reserve as well as the benefits of commercial management.

The government could potentially incentivize the building of commercial diesel inventories with a temporary waiver to the Jones Act. The combination of increased NEHHOR and mandated commercial reserves would simultaneously allow an expedited drawdown of reserves from commercially-held inventories while improving the relevance of NEHHOR as a backup system. The EU, in fact, obliges member states to hold at least one-third of emergency reserves as products.[21] In addition, some countries allow the minimum product stocks to be held by commercial producers and importers of the product.

One measure of size of reserves would be to follow the International Energy Agency (IEA) rule that requires member countries to hold oil stocks equivalent to 90 days of their net oil imports. Ninety days of net distillate imports of 120 thousand barrels per day to Petroleum Administration for Defense Districts I (PADD I) would equal a reserve of about 11 million barrels. Adverse, unintended consequences should also be considered. For example, the existence of a government reserve could discourage commercial inventory building in the region. The key for making this policy work is not to build inventory during the current market tightness as that would exacerbate price pressures.

Longer term, the solution for the East Coast’s diesel vulnerability is to reduce distillate fuel oil demand in the region. One option is to switch to natural gas for heating, which will require permitting natural gas pipelines from the Marcellus to the Northeast markets. Given decarbonization commitments, this build-up of natural gas infrastructure would need to follow the highest restrictions on methane emissions throughout the natural gas value chain. Another option would be to accelerate the electrification of heating and trucking in the Northeast. And another approach, currently being implemented in some states, is blending heating oil with renewable diesel, which would reduce carbon emissions while potentially displacing up to 20 percent of diesel consumed. New York[22] state is moving in this direction. Such policy solutions should be on the table not only as a matter of energy security, but with an eye towards decarbonization.

A correction was made on July 19, 2023

This article was updated to correct that the International Energy Agency (IEA) requires member countries to hold oil stocks equivalent to 90 days of their net oil imports. The original article stated that the requirement was 90 days of net imports or 61 days of average consumption, whichever is greater.

[1]https://www.consilium.europa.eu/en/policies/sanctions/restrictive-measures-against-russia-over-ukraine/sanctions-against-russia-explained

[2] https://www.iea.org/reports/world-energy-outlook-2022

[3] https://www.eia.gov/energyexplained/heating-oil/use-of-heating-oil.php

[4] https://www.colpipe.com/about-us/our-company/system-map

[5] https://www.nytimes.com/2021/05/10/business/colonial-pipeline-ransomware.html

[6] https://www.eia.gov/petroleum/refinerycapacity/table13.pdf

[7] https://www.maritime.dot.gov/ports/domestic-shipping/domestic-shipping#act

[8] https://www.iea.org/articles/frequently-asked-questions-on-energy-security

[9] https://iea.blob.core.windows.net/assets/ed7af175-8e40-4e14-bde6-510cab88edfc/Oil2021midterm_tables.pdf

[10] https://www.reuters.com/markets/europe/why-are-french-refinery-workers-striking-2022-10-11/

[11] https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/oil/012422-china-cuts-oil-products-export-as-focus-shifts-to-efficiency-lower-emissions

[12] https://www.bloomberg.com/news/articles/2023-01-10/g-7-eyes-two-prices-caps-for-russian-refined-petroleum-products#xj4y7vzkg

[13] https://www.energypolicy.columbia.edu/research/qa/qa-how-eu-ban-russian-oil-might-impact-global-petroleum-product-markets2

[14]https://www.eia.gov/todayinenergy/detail.php?id=53279#:~:text=In%20the%20International%20Energy%20Agency’s,minus%20capacity%20that%20has%20closed

[15] https://www.bloomberg.com/news/articles/2023-01-05/colonial-shuts-key-fuel-pipeline-to-new-york-harbor-after-spill#xj4y7vzkg

[16] https://www.cnbc.com/2022/10/30/diesel-market-in-perfect-storm-as-prices-surge-and-supplies-dwindle.html

[17] https://www.nytimes.com/2021/05/08/us/politics/cyberattack-colonial-pipeline.html

[18] https://www.eia.gov/todayinenergy/detail.php?id=55039

[19] https://www.acf.hhs.gov/ocs/low-income-home-energy-assistance-program-liheap

[20] https://www.energy.gov/ceser/nehhor-releases

[21] https://www.iea.org/areas-of-work/ensuring-energy-security/oil-security

[22] https://www.biobased-diesel.com/post/new-york-state-enacts-bioheat-law-requiring-20-biodiesel-in-home-heating-oil-by-2030

President Donald Trump has made energy a clear focus for his second term in the White House. Having campaigned on an “America First” platform that highlighted domestic fossil-fuel growth, the reversal of climate policies and clean energy incentives advanced by the Biden administration, and substantial tariffs on key US trading partners, he declared an “energy emergency” on his first day in office.

The world has committed to transitioning away from fossil fuels to avoid the most severe threats of climate change.[1] Communities across the United States rely on fossil fuel...

November’s election for president of the United States will have crucial implications for the nation’s and world’s energy and climate policies.

The European Union (EU-27) is a globally significant trading bloc focused on reducing greenhouse gas emissions, including by seeking to impose its own environmental standards extra-territorially on its...

Nuclear power is being weighed in energy transition plans around the world, as countries seek to replace fossil fuels with low-carbon alternatives while also meeting growing energy demand and maintaining reliability and affordability.

Millions of US households struggle to meet their energy needs due to low wages, rising living costs, and other historical and structural drivers of poverty.

As Russian President Vladimir Putin prepares to visit China, the proposed Power of Siberia 2 natural gas pipeline is likely high on his agenda.