This website uses cookies as well as similar tools and technologies to understand visitors’ experiences. By continuing to use this website, you consent to Columbia University’s usage of cookies and similar technologies, in accordance with the Columbia University Website Cookie Notice.

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

In energy policy circles, the word “resilience” often refers to future-proof systems or infrastructure designed for the transition away from fossil fuels. But resilience means something different to...

Please join the Women in Energy initiative at the Center on Global Energy Policy at Columbia SIPA for a student roundtable lunch and discussion with Kadri Simson, who most recently...

Event

• Center on Global Energy Policy

1255 Amsterdam Ave

New York, NY 10027

About Us

We are the premier hub and policy institution for global energy thought leadership. Energy impacts every element of our lives, and our trusted fact-based research informs the decisions that affect all of us.

On February 4, the Trump administration imposed an additional 10 percent tariff on all Chinese imports into the United States. China’s Ministry of Commerce responded by announcing new tariffs on US imports, including a 15 percent tariff on US liquefied natural gas (LNG), which will take effect on February 10. In doing so, Beijing is reprising a move from the 2018–19 US–China trade war when it placed a 10 percent tariff (later increased to 25 percent) on US LNG.

US LNG sellers and Chinese buyers both have room to navigate this new political landscape, even if China’s US LNG imports fall to zero as they did from March 2019 to April 2020. But they both have more at stake now due to the large number of new long-term LNG contracts signed in 2021–23, which are set to increase significantly Chinese companies’ offtake of US LNG over the next four years. Contracted US LNG supplies amount to 35 bcm, six times what China imported in 2024.

Small But Growing US–China LNG Trade

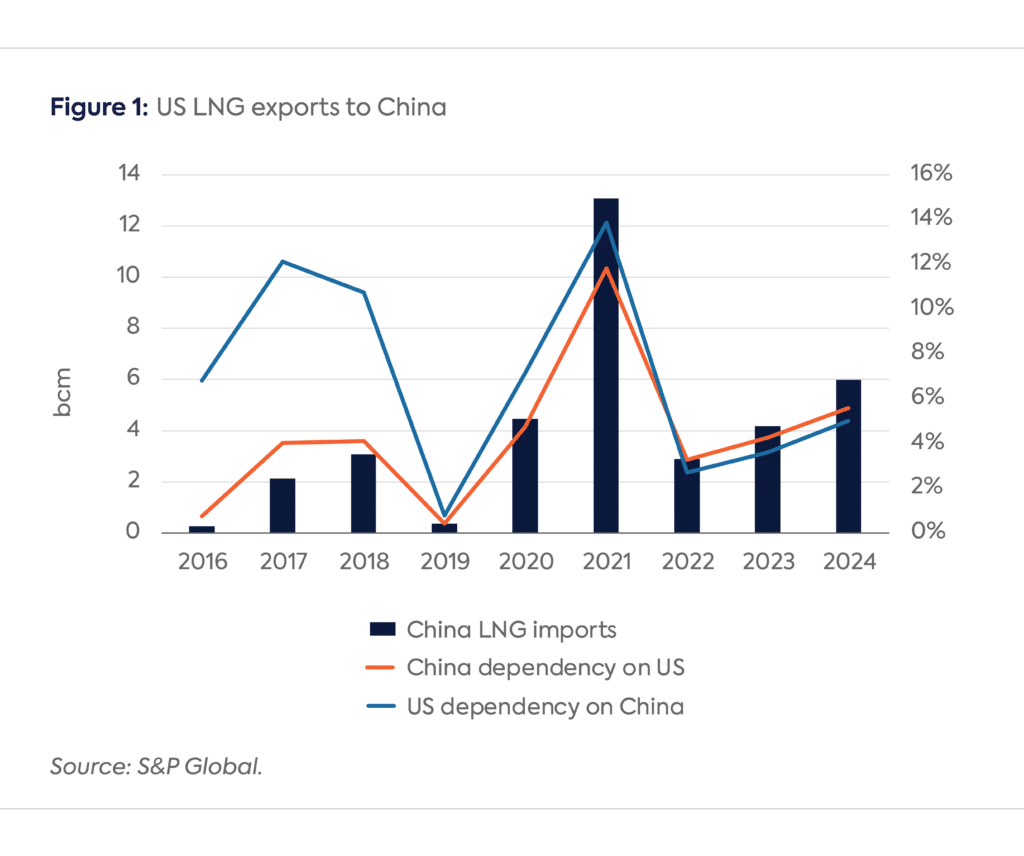

China is currently the largest LNG importer in the world, and the US is the largest LNG exporter. In 2024, only 6 percent of China’s LNG supply (6 billion cubic meters [bcm]) came from the US, while exports to China accounted for 5 percent of US LNG exports (Figure 1). The two countries are not significantly dependent on each other in this arena.

While China was already a large LNG importer in the late 2010s, when the first LNG trade disruption happened, its dependency on US LNG was limited to around 4 percent and 3 bcm (half of 2024 volumes) due to established contractual relationships with Australia, Indonesia, Malaysia, and Papua New Guinea. Interestingly, no Chinese company was a foundation customer of any of the first six US LNG export projects due to their unfamiliarity with Henry Hub indexation and uncertainty surrounding the two countries’ future relationship. The first contract between China (CNPC) and the US (Cheniere) was signed only in 2018, with a portion of the supply beginning in 2018 and the balance in 2023.

In 2021, China was the fastest-growing LNG importer and the US the fastest-growing LNG exporter, resulting in surging imports of US LNG by China. This trend reversed completely in 2022, when US LNG supplies (including volumes resold by Chinese buyers) were redirected to Europe, resulting in lower US LNG volumes going to China.

China’s Dependency on US LNG over the Next Four Years

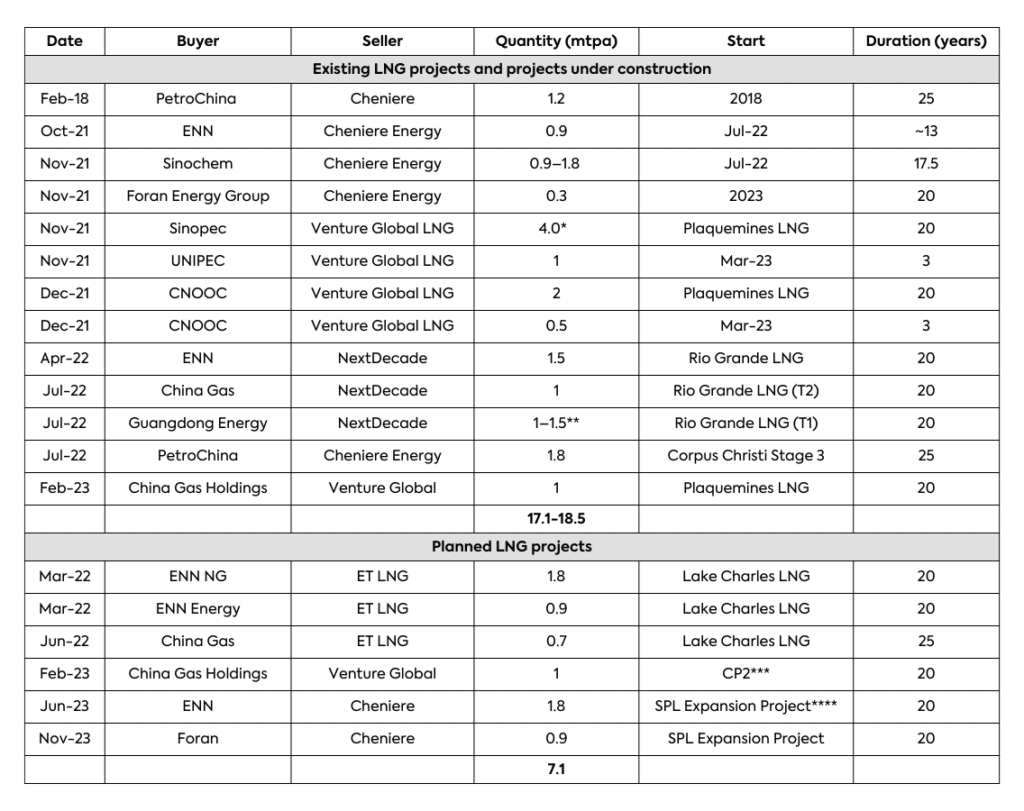

China signed many long-term LNG contracts with US projects between 2021 and 2023. As some of these projects come online in 2025 (Plaquemines and Corpus Christi, though commercial operations at the former will not start before the end of 2026), China’s import levels of US LNG are expected to rise (Table 1). Others have not yet taken a final investment decision (FID) (Lake Charles and Calcasieu Pass 2). Assuming all of these projects move forward, US LNG would represent up to a quarter of all of China’s contracted LNG.

Table 1. Contracts between US LNG projects and Chinese companies

Source: Companies’ announcements. *The contract with Sinopec consists of two contracts of 2.8 and 1.2 mtpa, respectively, but they are often aggregated and reported with a total of 4 mtpa. ** Right to buy an additional 0.5 mtpa. ***CP2: Calcasieu Pass 2. ****SPL: Sabine Pass Liquefaction.

China’s Response

Beijing’s response to President Trump’s new blanket China tariff, which includes imposing a 10 percent tariff on some US imports and a 15 percent tariff on others, is probably aimed at reminding the Trump administration that it has the capacity to harm the US (something it signalled repeatedly after the election) while avoiding an escalation of trade tensions. The value of China’s imports of US LNG in 2024 ($2.4 billion) is just a tiny fraction of the total value of China’s US imports during that year ($163.6 billion). This measured response likely leaves room for negotiations, which almost certainly appeals to Beijing given both Chinese officials’ mantra that no one wins a trade war and China’s struggling economy. Indeed, one reason why Beijing decided the tariffs will not take effect until February 10 could be to buy time to negotiate a reprieve, perhaps during a phone call between Trump and China’s leader Xi Jinping that the White House says still needs to be scheduled.

Additionally, the fact that China’s tariff on US LNG is less than the 2019 level may reflect the still-very-tight global gas markets and the potential expense of replacing contracted US LNG with spot LNG. There is little spare capacity in both Russian and Central Asian pipeline gas to replace 6 bcm of US LNG. But given low US gas prices, US LNG imports are still cheaper than spot LNG, even with a 15 percent tariff. If China were to reduce its total LNG imports in 2025, the move would trigger a welcome downward pressure on Asian and European spot prices.

The Choices Facing China’s LNG Buyers

The destination flexibility of US LNG makes it easier for Chinese firms with US LNG contracts to minimize the impact of Beijing’s new LNG tariff by simply reselling the US LNG to other markets. Chinese LNG buyers have increasingly acted as portfolio players, notably in 2022 when spot prices were high and LNG was resold to Europe. In addition, some Chinese LNG importers might be happy to keep US LNG in their portfolios due to its flexibility. Should the crisis extend into 2026 and especially 2027, Chinese LNG players will have access to more LNG supplies given the wave of projects coming online. Simultaneously, China’s new tariff on US LNG and the prospect of increasing US–China trade tensions are likely to make Chinese companies cautious about signing new long-term contracts with US LNG export projects. Among other effects, this may hamper some US LNG projects planning to take FID after President Trump lifted the pause on US LNG export permits.

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

This Energy Explained post represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

Earlier this month, China convened its “two sessions”—the annual concurrent meetings of the National People’s Congress (NPC), China’s legislature, and the Chinese People’s Political Consultative Congress, a political...