Trump is frustrated gasoline prices don’t mirror oil’s decline. Experts say it’s not that simple

U.S. gasoline prices decreased an average of 49 cents a gallon in the last month as expectations rose for an end to the war with Iran.

Get the latest as our experts share their insights on global energy policy.

This Energy Explained post represents the research and views of the author(s). It does not necessarily represent the views of the Center on Global Energy Policy. The piece...

Hear in-depth conversations with the world’s top energy and climate leaders from government, business, academia, and civil society.

The energy transition is in the midst of its own transition. Spiking electricity demand and geopolitical events are driving up energy prices, while debates over the best sources...

Fact Sheet by Noah Kaufman • April 02, 2019

This piece represents the research and views of the author. It does not necessarily represent the views of the Center on Global Energy Policy. The piece may be subject to further revision.

Contributions to SIPA for the benefit of CGEP are general use gifts, which gives the Center discretion in how it allocates these funds. More information is available at Our Partners page. Rare cases of sponsored projects are clearly indicated.

A carbon price is a fee on each unit of carbon dioxide (CO2) or other greenhouse gas emissions released into the atmosphere.

There are two primary methods of pricing carbon-carbon taxes and cap-and-trade programs. Carbon taxes would directly establish a price on carbon in dollars per ton of emissions.

A price on carbon can also be implemented via cap-and-trade programs, which limit the total quantity of emissions per year. This limit is enforced using tradable emissions permits that any emissions source must own to cover its emissions. The market for buying and selling these allowances creates the carbon price in a cap-and-trade program.

A price on carbon makes those responsible for the damages caused by greenhouse gas emissions pay for those damages. The primary objective of a carbon price is to change behavior. A carbon price makes carbon-intensive goods and services more expensive, which provides a financial incentive to use less of these products or shift to lower-carbon alternatives.

Various representatives and senators in the U.S. Congress have proposed legislation authorizing a federal carbon tax in recent years:

In addition, a proposal for a carbon tax from the Climate Leadership Council, authored by James Baker and George Shultz, has gained considerable support (“Baker Proposal”).

The key differences between the carbon tax proposals are described below.

Crafting a carbon tax requires policy designers to make numerous important decisions. Several of the most important design decisions are explored below.

A carbon tax requires policymakers to explicitly define the fee on each ton of CO2 emissions, typically on an annual basis. Higher tax rates mean larger emissions reductions, revenues, and price increases.

Policymakers can use various approaches to set carbon tax rates:

Tax rates may also be influenced by political factors, such as the impacts on energy prices. Some prefer carbon tax rates that start low so that the impacts of the policy phase in gradually.

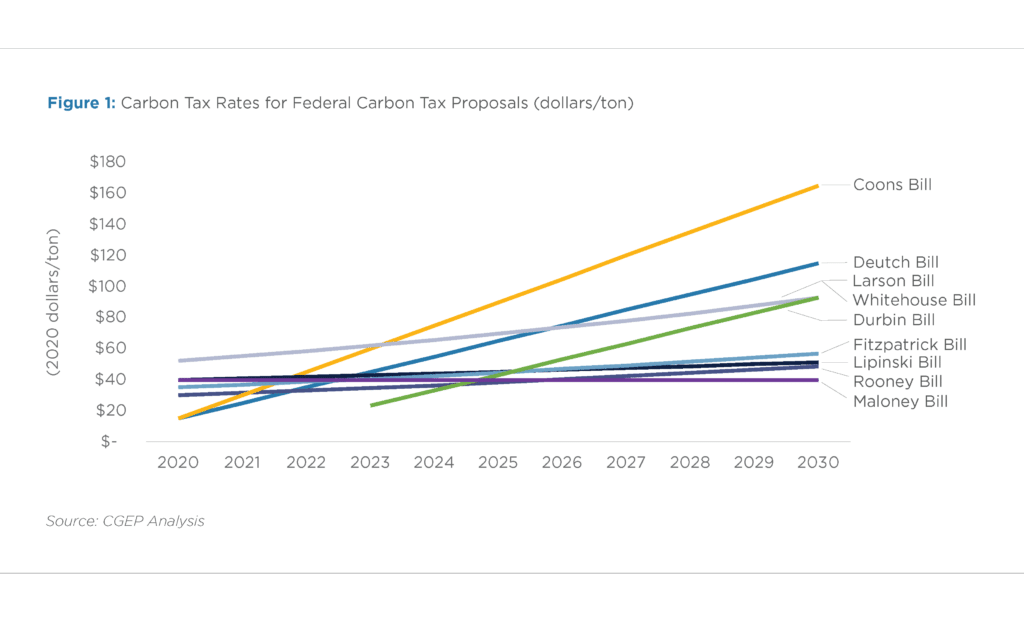

To reduce the uncertainty associated with the emissions outcomes under a carbon tax, some proposals make future tax rates contingent on emissions outcomes: the Fitzpatrick, Rooney, Coons, and Deutch bills all include such a mechanism.

Figure 1 shows the carbon tax rates from recent federal carbon tax proposals assuming emissions targets are met. The Baker proposal has not been finalized but will start at $43 per metric ton and increase between 3 and 5 percent above inflation each year.

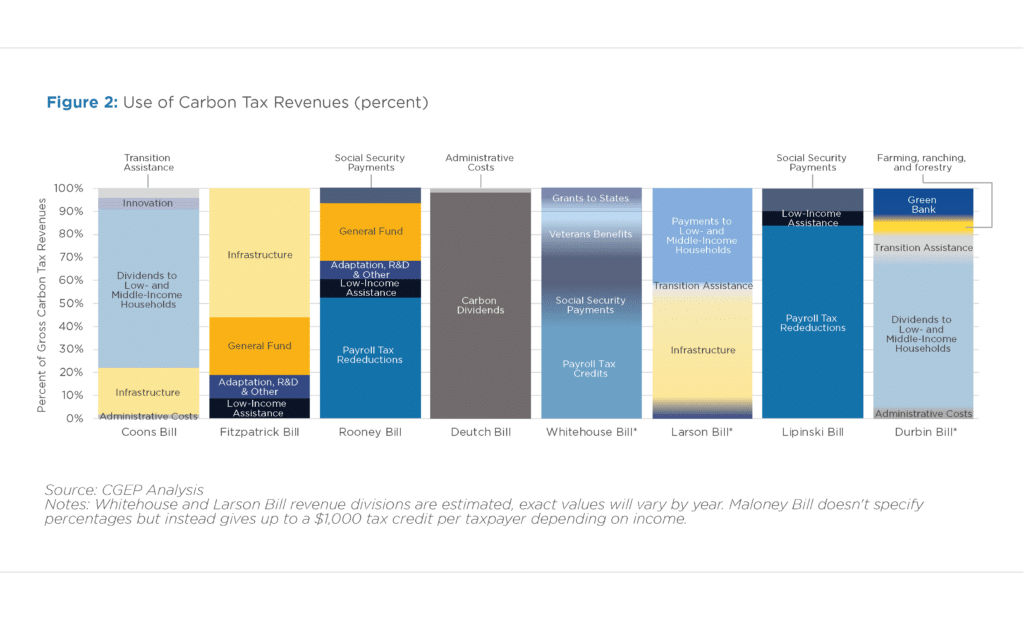

A carbon tax could provide hundreds of billions of dollars in new government revenue each year. Like other government resources, no consensus exists on how carbon tax revenue should be spent.

The following are commonly proposed uses for carbon tax revenue:

More than one approach to revenue allocation can be chosen in the design of a carbon tax program. Ultimately, the limiting factor is the revenue derived from the tax.

Revenue could also be used to fund the government more broadly. The budget process is designed to consider explicit trade-offs across priorities, while directing funds for particular uses from particular revenue sources narrows the scope of consideration and may result in spending on less efficient government programs. Figure 2 describes the revenue uses from recent federal carbon tax proposals:

A carbon tax could provide hundreds of billions of dollars in new government revenue each year. Like other government resources, no consensus exists on how carbon tax revenue should be spent.

The following are commonly proposed uses for carbon tax revenue:

More than one approach to revenue allocation can be chosen in the design of a carbon tax program. Ultimately, the limiting factor is the revenue derived from the tax.

Revenue could also be used to fund the government more broadly. The budget process is designed to consider explicit trade-offs across priorities, while directing funds for particular uses from particular revenue sources narrows the scope of consideration and may result in spending on less efficient government programs. Figure 2 describes the revenue uses from recent federal carbon tax proposals:

The “scope” of the carbon tax is the range of emissions that are subject to the tax. A broader scope will lead to a more efficient and environmentally effective tax because it increases the number of GHG abatement opportunities covered by the policy. A broader scope also allows for more revenue generation at a given tax rate, or a lower tax rate to achieve the same revenue target. However, broadening the scope also expands the number of groups facing a new tax liability and could potentially increase political opposition to a tax. In addition, the administrative burden associated with monitoring and verifying emissions reductions from certain sources may be sufficiently high that it does not make sense to make them subject to a carbon tax.

A carbon tax is considered “economy-wide” if it covers all or nearly all CO2 emissions from the energy system, instead of a specific economic sector like electricity. All recent federal proposals have been for economy-wide carbon taxes, but they include small differences in coverage, which will translate to small differences is revenue and emissions outcomes. For example, the Deutch bill exempts agricultural and military fuel use. The Fitzpatrick and Rooney Bills cover biodiesel based on lifecycle emissions not already taxed. Most bills also cover fluorinated gases at a reduced rate, which are strong greenhouse gases. All bills leave out land use, land-use change, and forestry due largely to the difficulty to monitor emissions and verify emissions reductions that have occurred in these sectors.

Unilaterally implementing a carbon tax raises various concerns for producers of products that are carbon-intensive and traded in international markets. First, the emissions goals of the policy could be jeopardized if U.S. producers relocate their operations or source their inputs from countries without equivalent regulations. Second, the economy could be harmed if U.S. companies are put at a disadvantage compared to foreign competitors whose products are not taxed at comparable rates.

Policymakers can use various methods to mitigate these considerations while continuing to include energy-intensive and trade-exposed industries in the scope of the policy.

One approach is to define a set of industries that are most at risk based on their energy intensity and exposure to international competition and implement a border carbon adjustment that requires importers of these products to pay a fee and provides rebates to exporters of the same products. In theory, this should create a level playing field in international markets, although in reality, numerous complications arise, such as how to determine the carbon content of products and whether and how to give credit to other countries with comparable climate policies. Despite these complications, all recent federal carbon tax proposals have included a border carbon adjustment, though the details differ across proposals.

Alternatively, producers of these energy-intensive and trade-exposed products can be compensated in a way that retains the incentive for these industries to reduce emissions. For example, producers can be given tax credits of an amount equal to the expected carbon tax payment for a representative company in each industry. Then, if these companies can reduce their emissions, they will receive the same subsidy but pay less in taxes.

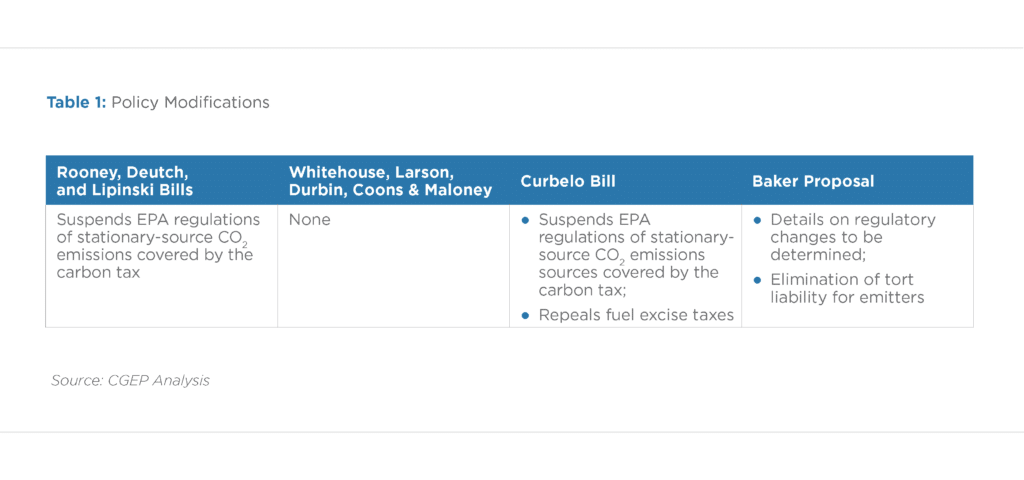

A carbon tax will not cover all sources of greenhouse gas emissions, and it does not address non-price related barriers to reducing emissions. Additional climate policies are needed. Yet policymakers are justified in reconsidering the need for and stringency of existing policies with similar or overlapping objectives if a carbon tax were to be adopted. Therefore, carbon tax proposals may include additions, subtractions, or changes to other policies.

To provide policymakers with information to help make these decisions, a CGEP report developed a framework for considering the interactions between a federal carbon tax and other policies that influence greenhouse gas emissions. The policies that are most redundant are regulations of the CO2 emissions of a facility that is covered by the carbon tax. Indeed, the elimination of policies in most recent carbon tax proposals have focused on these categories of policies. Table 1 summarizes the changes to existing policies in recent federal carbon tax proposals. Many bills contemplate using the carbon tax revenues for additional climate change mitigation and adaptation measures.

A carbon tax must specify the point in the supply chain where the tax is levied. Selecting the point of taxation requires considering the desired scope of the tax, existing emissions and/or fuel reporting infrastructure, administrative efficiency, and politics.

Carbon emissions can be taxed “upstream” at the point of fuel production, “downstream” at the point of fuel consumption, or at points in between. Carbon taxes can be imposed on imported fuels when they enter the country.

Ideally, the point of taxation should be where the greatest share of emissions is covered, the fewest number of entities are subject to the tax, and no fuel is inadvertently taxed twice. There are about 710 coal mines, 140 oil refineries and 551 natural gas processing plants in the United States, which may be efficient points of taxation.

Regardless of where the tax is imposed, firms will attempt to pass these costs on to consumers in the form of higher prices. Therefore, while the point of taxation matters to individual businesses and sectors, it is not a major determining factor of the overall energy market, emissions, or economic outcomes of a carbon tax.

A federal carbon tax would have impacts across the economy. Several major categories of impacts are explored below.

A carbon tax differs from other regulatory strategies by not only encouraging emissions reductions across the economy but also requiring the remaining emissions sources to pay the tax, thus creating significant federal revenues. The revenues raised by the tax are contingent on the tax rates, scope, and other design options, as well as the degree to which market actors decide to pay the carbon tax instead of changing their behavior.

Recent carbon tax proposals would bring in hundreds of billions of dollars in revenue per year by the mid-2020s. As emissions decline, the total amount of taxable GHGs will also decline, impacting revenues. However, overall revenues will rise if, as contemplated in the Deutch and Whitehouse proposals, carbon tax rates increase sufficiently quickly to more than offset the decrease in emissions. A preliminary analysis of the Deutch Bill shows that carbon tax revenues would rise from $70 billion in 2020, to $400 billion in 2030. For context, the U.S. corporate income tax raised about $300 billion in 2017 (prior to the 2017 tax cuts), and the federal excise tax on gasoline and diesel fuel brought in about $40 billion. Under the Deutch Bill, nearly all revenue is used for annual dividend payments, which would increase to about $1400 for adults and $600 to children by 2030.

Net revenues are likely to be lower because payments of the carbon tax leave individuals and businesses with less income, and thus lower tax payments on that income. This is referred to by the Joint Committee on Taxation and the Congressional Budget Office as the “Income and Payroll Tax Offset.” A recent analysis of carbon tax proposals indicates this offset could reduce government revenue by about 23 percent of the annual carbon tax revenue.

Finally, there will be other effects on government revenue that are difficult to quantify and may be large. The expenditures of the revenue and the price increases will have “multiplier” effects that ripple across the economy, and the carbon tax will lead to differences in the production and consumption of goods across the economy, which will influence overall tax revenues.

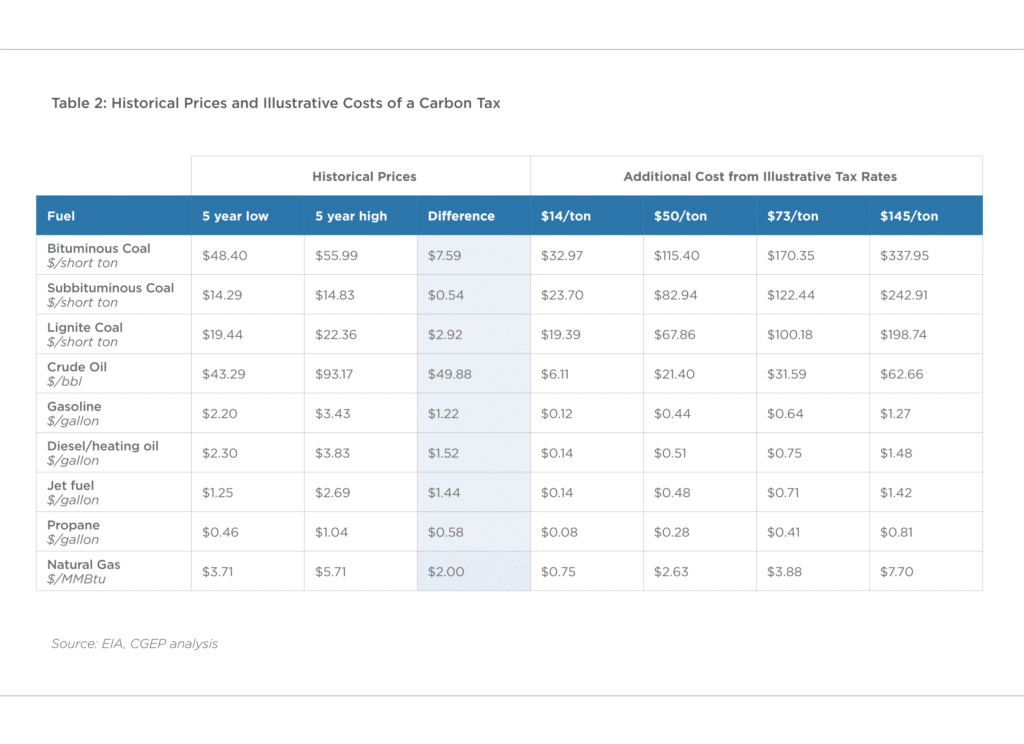

A carbon tax increases energy costs in proportion to the carbon content of the source of energy. On account of the different carbon-intensity of fuels, price impacts are most significant for energy produced with coal, then petroleum, then natural gas. Higher carbon tax rates cause larger changes in energy prices. Table 2 shows the impacts of various carbon tax rates on fuels and compares them to the 5-year high and low of those fuels, as of 2019, to give an indication of the likely impact on prices.

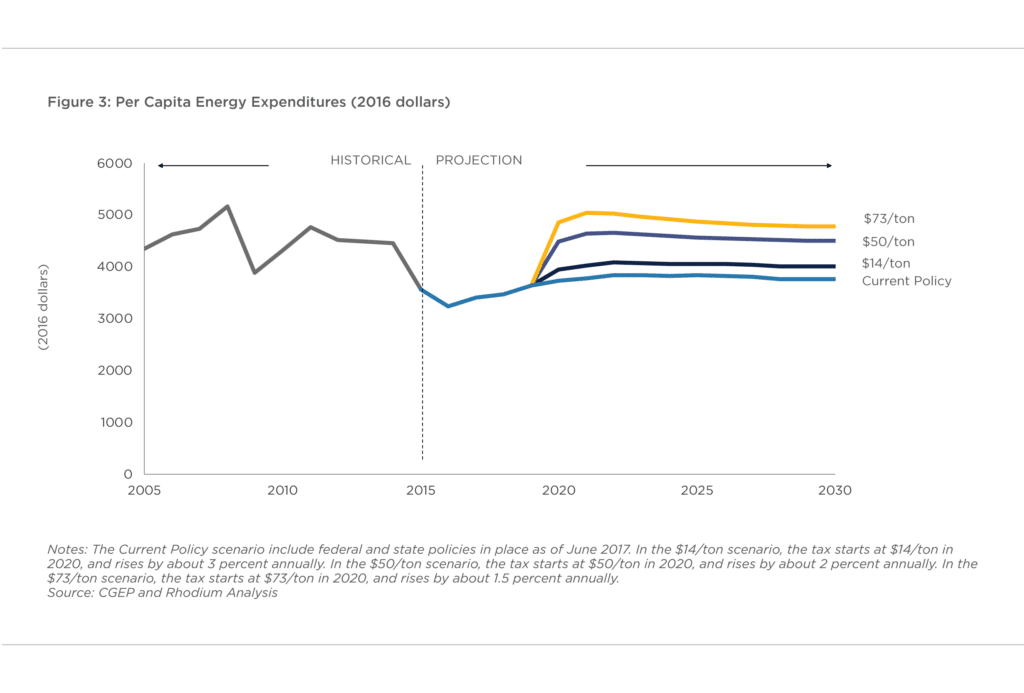

Higher energy prices translate into price increases for consumers. Figure 3 shows changes in per capita energy expenditures under the three illustrative carbon tax scenarios. Total annual per capita energy expenditures increase by as much as 6 percent, 21 percent, and 34 percent in the $14/ton, $50/ton, and $73/ton scenarios. In all scenarios, they remain below the per capita expenditure levels at the height of the global commodity boom in 2008.

Notes: The Current Policy scenario include federal and state policies in place as of June 2017. In the $14/ton scenario, the tax starts at $14/ton in 2020, and rises by about 3 percent annually. In the $50/ton scenario, the tax starts at $50/ton in 2020, and rises by about 2 percent annually. In the $73/ton scenario, the tax starts at $73/ton in 2020, and rises by about 1.5 percent annually. Source: CGEP and Rhodium Analysis

A carbon tax provides a financial incentive to reduce emissions. Emitters of greenhouse gases will shift to lower-carbon alternatives if doing so costs less than the tax. Moreover, the carbon price will accelerate low-carbon technological progress due to increased deployments of low-carbon technologies today (i.e. “learning-by-doing”) and larger investments in innovation because of the promise of greater market share in the future.

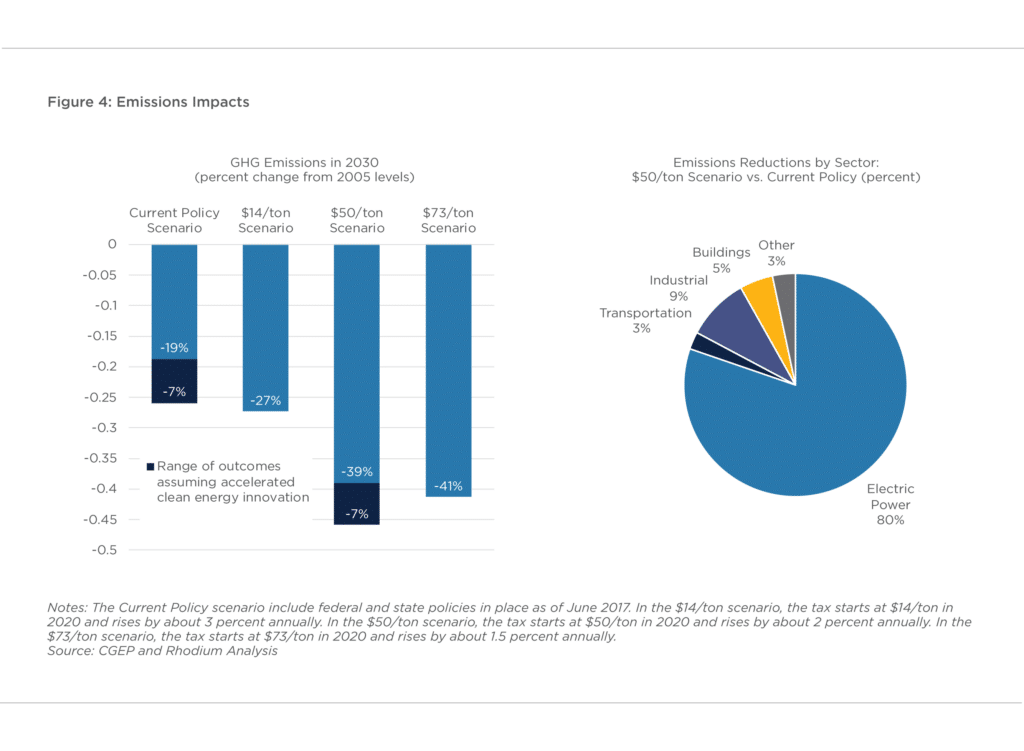

The tax rate is the main design element that determines the magnitude of emissions reductions caused by the carbon tax, although the policy scope and revenues targeted at mitigation would influence emissions as well. Figure 4 below shows emissions reductions by 2030 from three illustrative carbon taxes along with a current policy scenario. Under the $50/ton scenario, US emissions fall to 39–46 percent below 2005 levels, depending on assumptions related to technological progress.

The majority of the emissions reductions caused by the carbon tax are in the power sector, where competitive markets, a relatively small number of corporate actors, and an array of clean energy technologies facilitate deep and immediate emissions reductions.

Notes: The Current Policy scenario include federal and state policies in place as of June 2017. In the $14/ton scenario, the tax starts at $14/ton in 2020 and rises by about 3 percent annually. In the $50/ton scenario, the tax starts at $50/ton in 2020 and rises by about 2 percent annually. In the $73/ton scenario, the tax starts at $73/ton in 2020 and rises by about 1.5 percent annually. Source: CGEP and Rhodium Analysis

Actual emissions could be higher or lower than the projections shown above, and these results should be interpreted with the following considerations in mind:

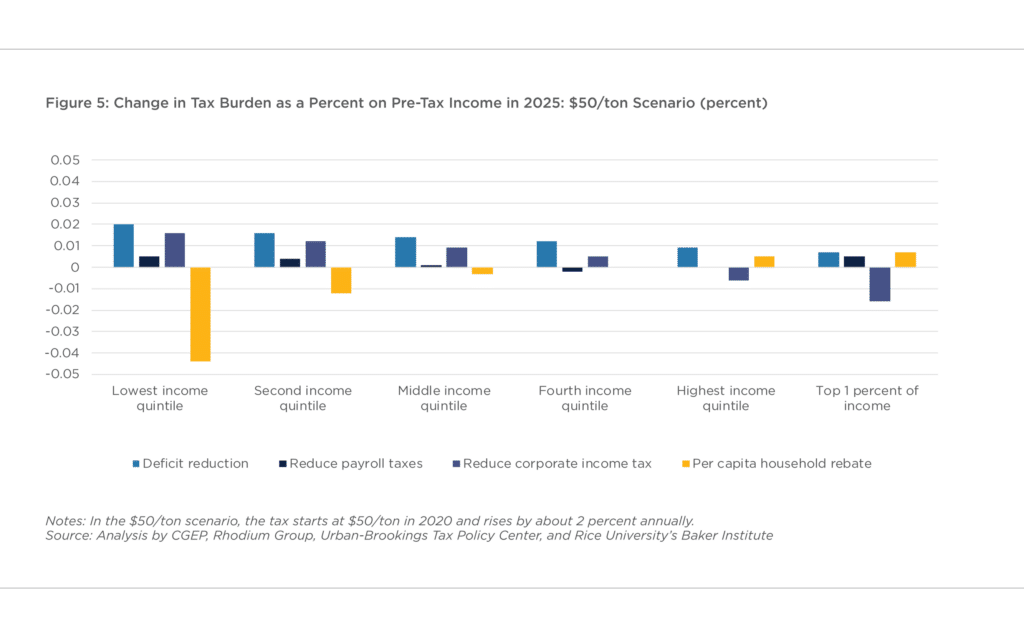

Lower-income households could struggle to afford the potential increases in energy prices caused by a carbon tax or other climate policies. Policymakers can ensure that low-income and middle-class households will not be harmed by the carbon tax by using the revenue in ways that benefit these households.

One approach, contemplated by the Deutch Bill and Baker Proposal, is to use most or all of the revenue for equal per capita household rebates/dividends. Figure 5 below shows that in contrast to other revenue uses, when all revenues are used for equal rebates, the policy is progressive, with lower-income households receiving far more in rebates than they pay in additional taxes. The tax burden for low-income households (bottom 20 percent) decreases by 4–5 percent of pre-tax income in a $50/ton carbon tax scenario.

Notes: In the $50/ton scenario, the tax starts at $50/ton in 2020 and rises by about 2 percent annually. Source: Analysis by CGEP, Rhodium Group, Urban-Brookings Tax Policy Center and Rice University’s Baker Institute

Another approach is to use at least some of the carbon tax revenue in ways that specifically benefit low- and middle-income households. All of the proposed bills in Congress that do not use all revenues for equal dividends direct a portion of the revenues to low-income households, although the details differ across proposals. For example, under the MARKET CHOICE Act, a 2018 carbon tax bill proposed by Congressman Carlos Curbelo, 10 percent of the net government revenue is used for dividends to households in the bottom 20 percent of the income distribution, which would be sufficient to fully offset the price increases for the vast majority of these low-income households.

A large-scale shift from high-carbon to low-carbon energy sources will have wide-ranging effects on the U.S. economy. A price on carbon is a necessary part of a low-cost climate change strategy because it encourages emissions reductions wherever and however they can be achieved at the lowest cost.

For years economists have been studying the potential economic impacts of carbon pricing policies. Models show that effects of a carbon tax on near-term macroeconomic outcomes like gross domestic product (GDP) are small and typically negative compared to a current policy scenario. These studies are highly imperfect—they nearly always exclude the economic benefits of avoided regulations and reduced air pollution, as well as any changes in technological progress stimulated by the tax.

Economic studies of carbon prices may be most useful in highlighting the trade-offs among policy design choices. How the carbon tax revenue is used is a differentiating factor in macroeconomic outcomes. Economic studies show that national economic outcomes are best when carbon tax revenues are used in ways that correct pre-existing inefficiencies in the U.S. economy. For example, using revenue to reduce payroll taxes or income taxes would not only return the revenues to taxpayers but also provide financial incentives for increased work. The Whitehouse, Rooney and Lipinski Bills use the majority of carbon tax revenue to reduce payroll taxes. In contrast, the carbon dividends approach of the Deutch Bill and Baker proposal returns the carbon tax payments to eligible recipients without correcting any existing distortions in the economy.

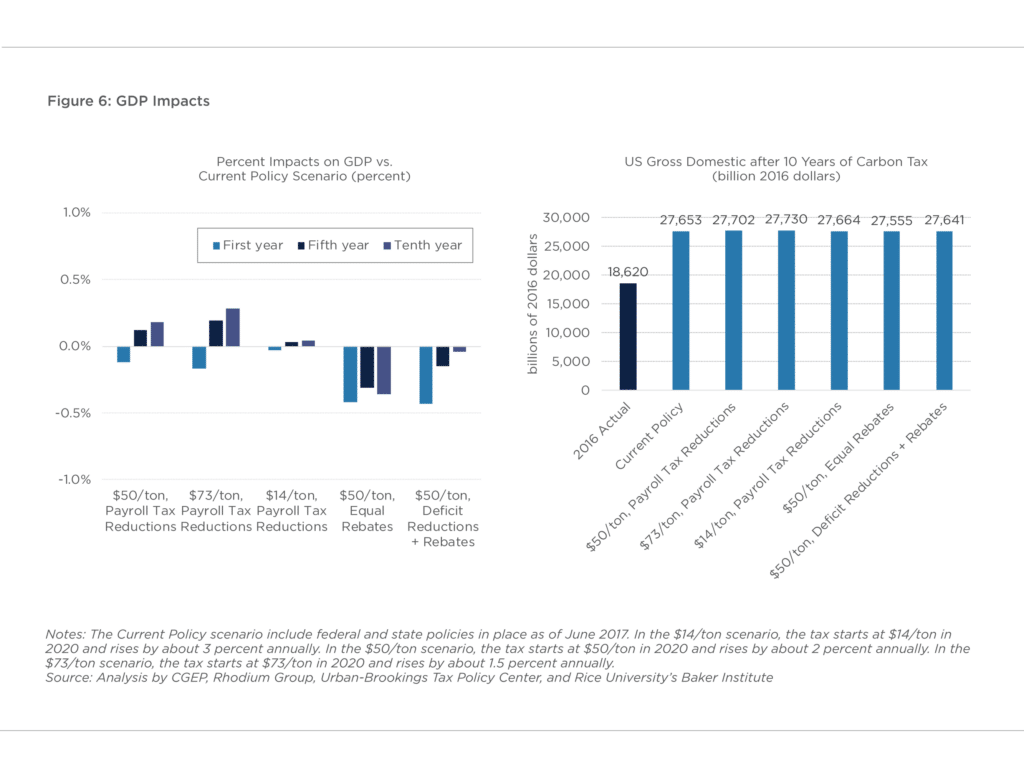

Figure 6 shows the effects of a carbon tax on U.S. gross domestic product (GDP) of three illustrative carbon tax scenarios compared to a current policy scenario. GDP impacts are less than 0.5 percent per year and they could be positive or negative, depending on the revenue use.

Notes: The Current Policy scenario include federal and state policies in place as of June 2017. In the $14/ton scenario, the tax starts at $14/ton in 2020 and rises by about 3 percent annually. In the $50/ton scenario, the tax starts at $50/ton in 2020 and rises by about 2 percent annually. In the $73/ton scenario, the tax starts at $73/ton in 2020 and rises by about 1.5 percent annually. Source: Analysis by CGEP, Rhodium Group, Urban-Brookings Tax Policy Center and Rice University’s Baker Institute

Nationwide results mask subnational variation, primarily caused by regional differences in energy production and consumption. Rural communities will likely face larger energy cost increases as a share of income than urban residents because low population density typically is associated with higher per capita energy demand for transport, heating, and cooling.

While the western and northeastern regions of the country would fare relatively well under a carbon tax, the economic effects would be worse in the more carbon- and energy-intensive southern and middle parts of the country, where, according to one recent study, the carbon tax causes gross regional product to fall by as much as 0.6 percent compared to the baseline scenario in 2030. Carbon tax revenues can be used to mitigate such regional disparities.

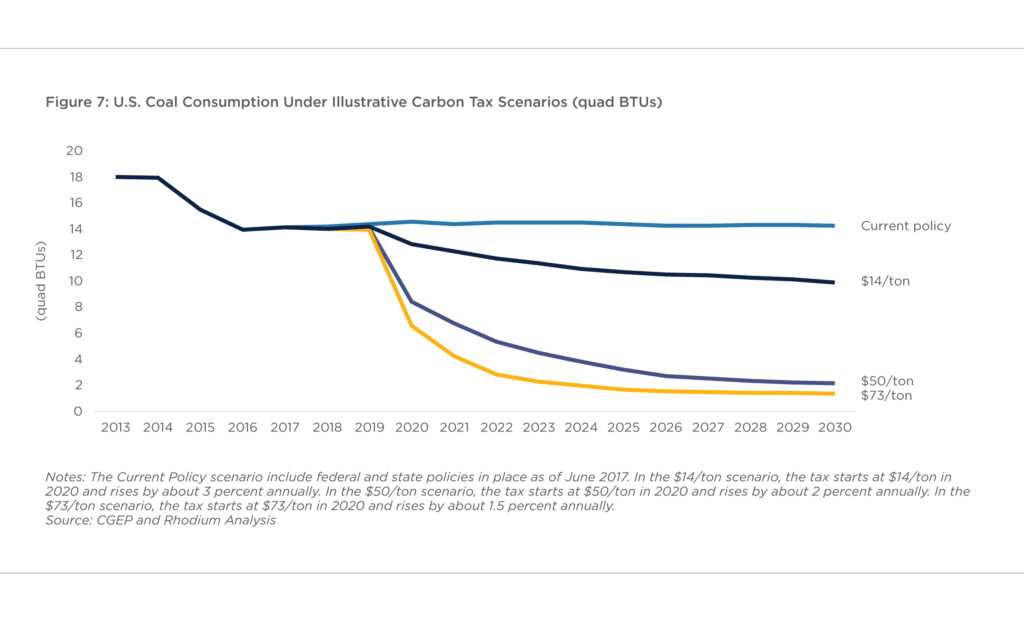

Communities with rich renewable resources are more likely to capture the clean energy investment a carbon tax would incentivize. In contrast, the largest adverse impacts will be on regions dependent on the coal industry. Figure 7 below shows the decline of coal production in the 2020s under three illustrative carbon tax scenarios. The U.S. coal industry is highly geographically concentrated, meaning a relatively small number of local economies across the country are highly reliant on the coal industry. A recent CGEP/Brookings study highlighted the fiscal risks of climate policy to coal-reliant local governments.

Notes: The Current Policy scenario include federal and state policies in place as of June 2017. In the $14/ton scenario, the tax starts at $14/ton in 2020 and rises by about 3 percent annually. In the $50/ton scenario, the tax starts at $50/ton in 2020 and rises by about 2 percent annually. In the $73/ton scenario, the tax starts at $73/ton in 2020 and rises by about 1.5 percent annually. Source: CGEP and Rhodium Analysis

Carbon tax proposals have allocated revenue to compensate coal workers and communities and invest in the economies of these regions—indeed, a small sliver of carbon tax revenue could provide billions of dollars per year in assistance to these regions.

Project-based carbon credit markets (PCCMs) facilitate the generation, trading, and retirement of carbon credits from projects that remove, reduce, or avoid greenhouse gas emissions.

The World Bank is revisiting one of its most entrenched positions, publicly questioning its long-standing emphasis on market-led approaches in economic policy.

Full report

Fact Sheet by Noah Kaufman • April 02, 2019